What Is the After-tax Cost of Debt?

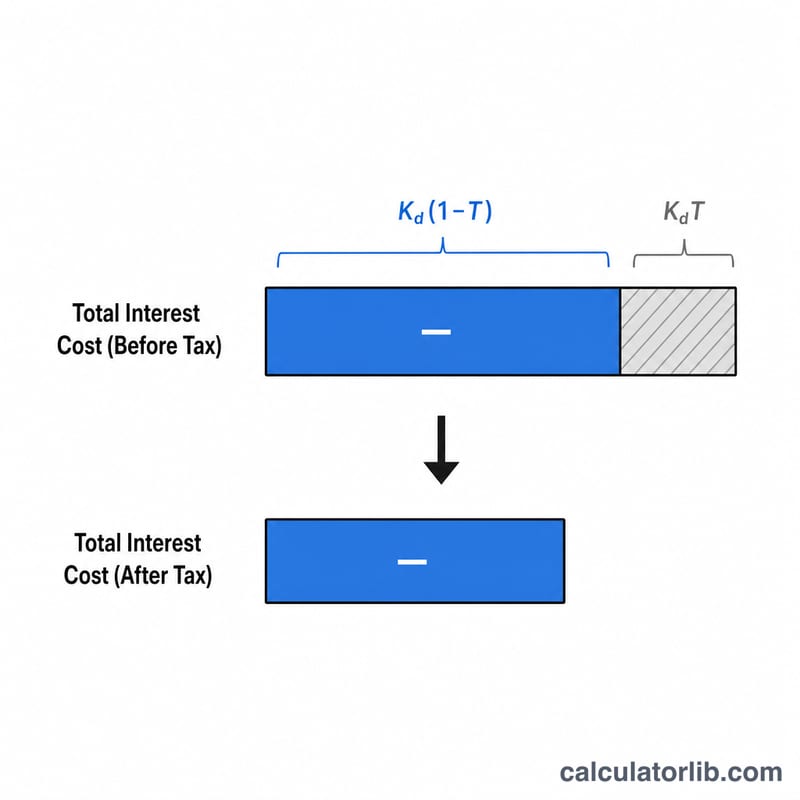

The after-tax cost of debt is the effective interest rate a company pays on its borrowings once the tax benefit of interest is taken into account. Because interest expense is typically tax-deductible, every dollar of interest reduces taxable income, lowering the true cost of debt below the stated (pre-tax) rate. This figure is a key input into the Weighted Average Cost of Capital (WACC).

How to Use This Calculator

Enter two values: the pre-tax cost of debt (your effective borrowing interest rate, as a percentage) and the company's tax rate (as a percentage). The calculator returns the after-tax cost of debt along with the tax shield — the portion of the rate that is effectively recovered through tax savings.

The Formula Explained

The relationship is simple:

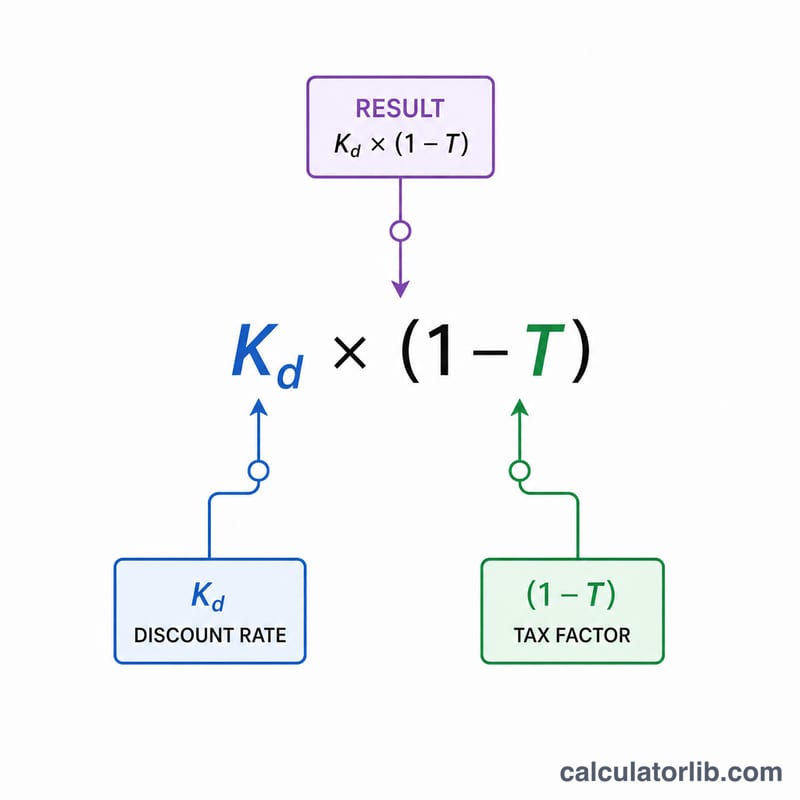

$$\text{After-tax Cost of Debt} = K_d \times (1 - T)$$The term \((1 - T)\) shrinks the pre-tax rate in proportion to how much of the interest is shielded from tax. A higher tax rate produces a lower after-tax cost because more of the interest expense is offset by reduced taxes.

Worked Example

Suppose a firm borrows at a pre-tax rate of 6% and faces a 25% tax rate. The after-tax cost is

$$6\% \times (1 - 0.25) = 6\% \times 0.75 = \mathbf{4.5\%}$$The tax shield is the difference, \(6\% - 4.5\% = 1.5\%\). So although the loan nominally costs 6%, it really costs the company only 4.5% after tax savings.

Interpreting Your Result

The after-tax cost of debt is the effective interest rate a company pays on its borrowings after accounting for the tax deductibility of interest expense. Because most tax systems allow interest to be deducted before calculating taxable income, every dollar of interest paid reduces the tax bill — this saving is called the tax shield and it lowers the true economic cost of borrowing below the headline (pre-tax) rate.

As a worked example, a firm borrowing at a pre-tax rate of 8% with a 25% marginal tax rate has an after-tax cost of debt of \(8\% \times (1 - 0.25) = \) 6%. The 2% gap between the 8% pre-tax rate and the 6% after-tax rate is the value of the tax shield.

How it feeds into WACC

The after-tax cost of debt is the debt component of the Weighted Average Cost of Capital (WACC). WACC blends the cost of each capital source by its weight in the capital structure:

$$\text{WACC} = \frac{E}{V}\,K_e + \frac{D}{V}\,K_d(1 - T)$$

where \(E\) is the market value of equity, \(D\) the market value of debt, \(V = E + D\), \(K_e\) the cost of equity, \(K_d\) the pre-tax cost of debt, and \(T\) the tax rate. Note that only the debt term is tax-adjusted, because dividends and equity returns are not tax-deductible.

Comparison to the cost of equity

The after-tax cost of debt is almost always lower than the cost of equity. Debt holders have a contractual, senior claim on cash flows and assets, so they bear less risk and demand a lower return; equity holders are residual claimants and require a higher return for that risk. The tax shield widens this gap further, which is one reason moderate leverage can reduce a firm's overall WACC.

Higher vs. lower values

A lower after-tax cost of debt signals cheaper borrowing — driven by a low pre-tax rate (strong credit quality, low benchmark rates) and/or a high tax rate that magnifies the shield. A higher after-tax cost of debt implies more expensive financing, often reflecting higher credit risk, rising interest rates, or a low or zero tax rate (e.g. a company with current losses that cannot immediately use the deduction).

Important caveat: limits on interest deductibility

The simple formula assumes every dollar of interest produces a full tax shield at the marginal rate. In practice, deductibility may be capped. Many jurisdictions limit net interest deductions to a percentage of EBITDA or EBIT (for example, the U.S. Section 163(j) limit of 30% of adjusted taxable income). When interest exceeds the cap, the excess is not currently deductible, so the realized tax shield is smaller and the true after-tax cost of debt is higher than the formula suggests. Loss-making firms, those with disallowed interest, or those subject to alternative minimum taxes should treat the calculated value as a best-case lower bound.

Key Terms Defined

- Pre-tax cost of debt (Kd)

- The effective interest rate a company pays on its borrowings before any tax effects. It is typically measured as the weighted-average yield on outstanding debt, often approximated by the yield to maturity on the firm's bonds or the interest rate on its loans.

- After-tax cost of debt

- The pre-tax cost of debt adjusted downward for the tax deductibility of interest, calculated as \(K_d \times (1 - T)\). It represents the true economic cost of debt financing and is the figure used in WACC.

- Tax shield

- The reduction in income taxes that results from deducting an expense — here, interest. The interest tax shield equals the interest expense multiplied by the tax rate, and it is the difference between the pre-tax and after-tax cost of debt.

- Marginal tax rate

- The tax rate applied to the next dollar of taxable income. Because interest reduces income at the top of the income stack, the marginal rate is the theoretically correct rate for valuing the interest tax shield.

- Effective tax rate

- Total tax expense divided by pre-tax income — the average rate a company actually pays across all its income. It often differs from the marginal rate due to credits, exemptions, and differences between book and tax accounting; it is sometimes used as a practical proxy when the marginal rate is hard to pin down.

- Yield to maturity (YTM)

- The total annualized return an investor earns if a bond is held to maturity, accounting for the coupon payments and any difference between purchase price and face value. YTM on a firm's outstanding bonds is a common, market-based estimate of its pre-tax cost of debt.

- Weighted Average Cost of Capital (WACC)

- The blended minimum rate of return a company must earn on its assets to satisfy all capital providers, weighting the after-tax cost of debt and the cost of equity by their respective shares of total capital. It is widely used as the discount rate in valuation and capital-budgeting decisions.

FAQ

Why is the after-tax cost lower than the stated rate? Interest is tax-deductible, so part of the cost is recovered as reduced taxes.

What rate should I enter for cost of debt? Use the company's effective weighted interest rate across all loans and bonds, often the yield to maturity on outstanding debt.

What tax rate applies? Use the firm's marginal effective tax rate. Note that tax rules and deductibility limits vary by jurisdiction.