What is the Number of Payments (NPER) Calculator?

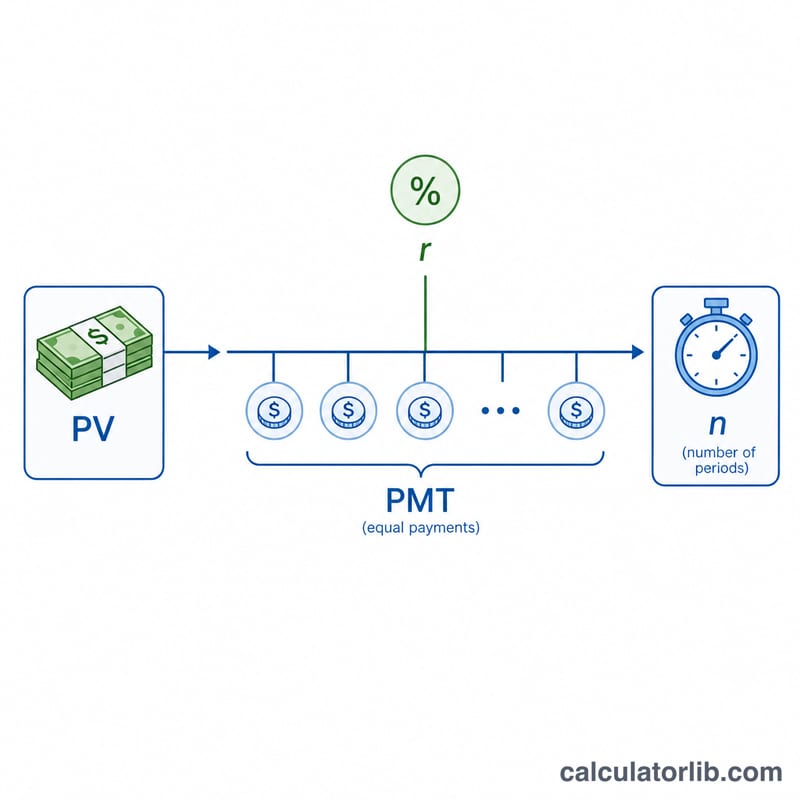

This calculator tells you how many equal periodic payments are required to fully repay a loan. Given the loan amount (present value), the fixed payment you make each period, and the interest rate, it solves for n — the total number of payments. It mirrors the spreadsheet NPER function and is useful for loans, mortgages, car finance, and any amortizing debt.

How to use it

Enter the loan or present value, the payment you make each period, the annual interest rate as a percentage, and how often you pay (monthly, weekly, etc.). The calculator converts the annual rate to a periodic rate and returns the number of payments, the equivalent time in years, the total amount paid, and the total interest.

The formula explained

The number of payments is:

$$n = \frac{-\ln\!\left(1 - \dfrac{PV \cdot r}{PMT}\right)}{\ln(1 + r)}$$

Here PV is the present value (loan balance), PMT is the payment per period, and r is the periodic interest rate (annual rate divided by payments per year). The natural logarithm (ln) appears because each payment compounds against a growing balance. Note: if the payment is smaller than the first period's interest, the loan never amortizes and no finite solution exists.

Worked example

Borrow $10,000 at 6% annual interest, paying $200 per month. The monthly rate is \(0.06 / 12 = 0.005\). Then $$n = \frac{-\ln\!\left(1 - \dfrac{10000 \cdot 0.005}{200}\right)}{\ln(1.005)} = \frac{-\ln(0.75)}{\ln(1.005)} \approx \frac{0.287682}{0.0049875} \approx 57.68 \text{ payments},$$ or about 4.81 years. Total paid ≈ $11,537, of which ≈ $1,537 is interest.

FAQ

Why is my answer a fraction? The formula returns a continuous value; in practice you round up and make a smaller final payment.

What if the rate is 0%? With no interest, n is simply \(PV \div PMT\).

Why does it show 0 or no result? If your payment doesn't cover the interest charged each period, the balance never decreases and the loan cannot be repaid — increase the payment.