What is the Compound Interest Rate Calculator?

This calculator solves for the interest rate hidden inside any growth scenario. If you know how much you started with (the present value), how much you ended up with (the future value), and how long the money was invested, you can work backward to find the constant compound rate that links them. This rate is often called the Compound Annual Growth Rate (CAGR).

How to use it

Enter the Present Value (PV) — your starting amount — and the Future Value (FV) — the ending amount. Add the number of years the investment was held and how many times interest compounds per year (1 for annual, 12 for monthly, 365 for daily). The tool returns the effective annual rate, the rate per compounding period, and the total growth.

The formula explained

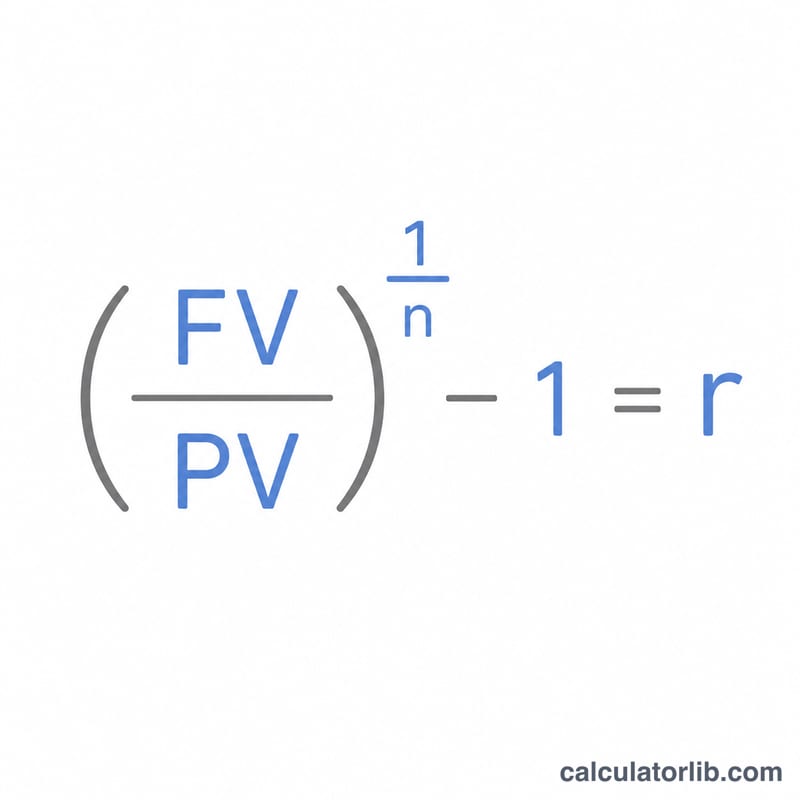

The core equation is $$r = \left[ \left( \frac{\text{FV}}{\text{PV}} \right)^{\frac{1}{n}} - 1 \right]$$ where n is the total number of compounding periods (years × compounds per year). Raising the ratio of future to present value to the power of \(1/n\) "undoes" the compounding, and subtracting 1 converts the growth factor into a rate. Multiply by 100 to express it as a percentage.

Worked example

Suppose you invested $1,000 and it grew to $2,000 over 10 years with annual compounding. Then \(\text{FV}/\text{PV} = 2\), \(n = 10\), so $$r = 2^{0.1} - 1 = 1.07177 - 1 = 0.07177$$ or about 7.18% per year. Your money doubled, which matches the classic "rule of 72" estimate \(72 \div 10 \approx 7.2\%\).

FAQ

What is the difference between the annual rate and the rate per period? The annual rate assumes one compounding per year; the rate per period is the smaller rate applied each compounding interval. With annual compounding they are identical.

Can I use this for any time unit? Yes — as long as PV, FV, years, and compounds per year are consistent, the formula works for any investment, savings account, or asset.

What if PV is larger than FV? The calculator returns a negative rate, indicating the value declined (a loss) over the period.