What Is the Income Tax Philippines Calculator?

This calculator applies to the Philippines and uses the graduated income tax brackets under the BIR TRAIN Law (Tax Reform for Acceleration and Inclusion, the rates effective from 2023 onward). It estimates the annual income tax due on your taxable income — the amount remaining after allowable deductions and exemptions. The first ₱250,000 of annual taxable income is exempt from tax.

How to Use It

Enter your annual taxable income in Philippine pesos. This should already account for mandatory contributions (SSS, PhilHealth, Pag-IBIG) and other deductions, since income tax is computed on net taxable income. The calculator returns your annual tax due, net income after tax, your effective tax rate, and the marginal rate of your bracket.

The Formula Explained

The Philippines uses a progressive bracket system. Each bracket has a fixed base tax plus a marginal rate applied only to the income above the bracket's floor:

$$\text{Tax} = \text{Base} + \text{Rate} \times (\text{Income} - \text{Floor})$$

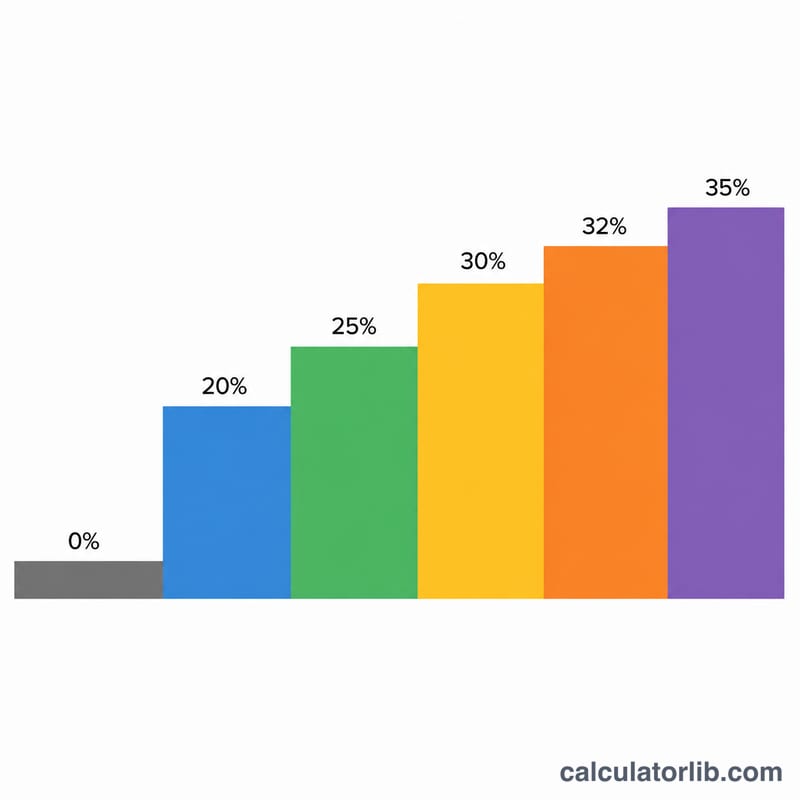

The 2023 brackets are: up to ₱250,000 → 0%; ₱250,001–400,000 → 15% of excess over ₱250,000; ₱400,001–800,000 → ₱22,500 + 20% of excess over ₱400,000; ₱800,001–2,000,000 → ₱102,500 + 25% of excess over ₱800,000; ₱2,000,001–8,000,000 → ₱402,500 + 30% of excess over ₱2,000,000; over ₱8,000,000 → ₱2,202,500 + 35% of excess over ₱8,000,000.

Worked Example

Suppose your annual taxable income is ₱500,000. This falls in the ₱400,001–800,000 bracket. $$\text{Tax} = ₱22{,}500 + 20\% \times (₱500{,}000 - ₱400{,}000) = ₱22{,}500 + ₱20{,}000 = \textbf{₱42{,}500}$$ Your effective rate is \(42{,}500 \div 500{,}000 = 8.5\%\), and your marginal rate is 20%.

FAQ

Is the first ₱250,000 really tax-free? Yes. Under the TRAIN law, annual taxable income of ₱250,000 or below incurs zero income tax.

Does this include SSS, PhilHealth, and Pag-IBIG? No — those are deductions you subtract before arriving at taxable income. Enter the income figure after those deductions.

Is this for employees or self-employed? These graduated rates apply to compensation earners and to self-employed/professionals who do not opt for the 8% flat rate. Always confirm with a tax professional or the BIR for your specific situation.