What this calculator does

This tool estimates UK Income Tax for the 2026/27 tax year for taxpayers in England, Wales and Northern Ireland. (Scotland uses different bands and rates.) It applies the standard personal allowance, the allowance taper for high earners, and the basic, higher and additional rate bands to your gross annual income. It does not include National Insurance, pension relief, student loans or other deductions.

How to use it

Enter your annual gross income and select the tax year, then read off your total income tax, take-home pay, and a band-by-band breakdown. The result also shows your personal allowance (which shrinks if you earn over £100,000) and your effective tax rate.

The formula explained

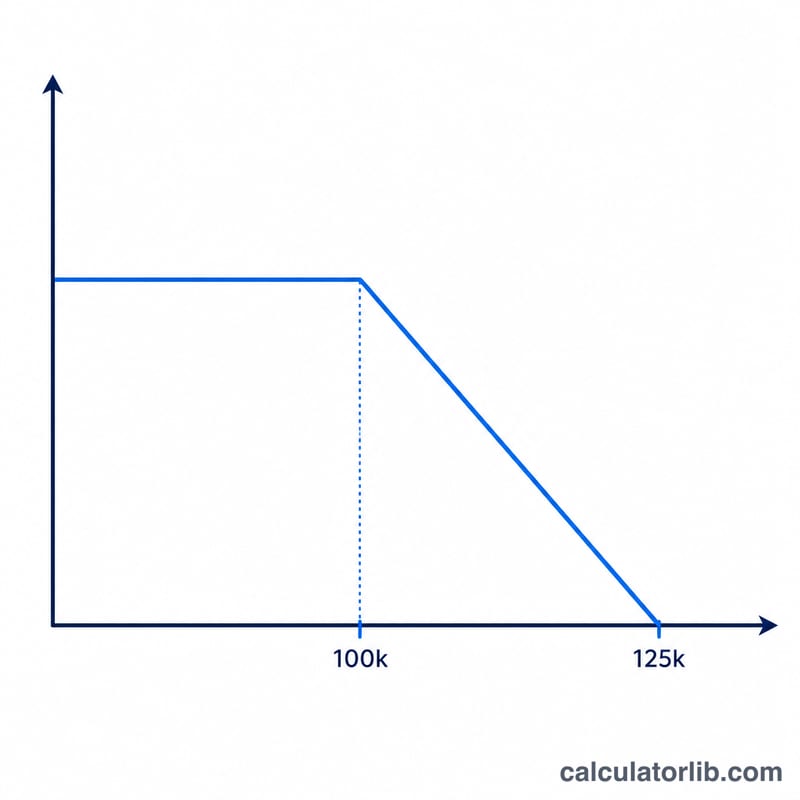

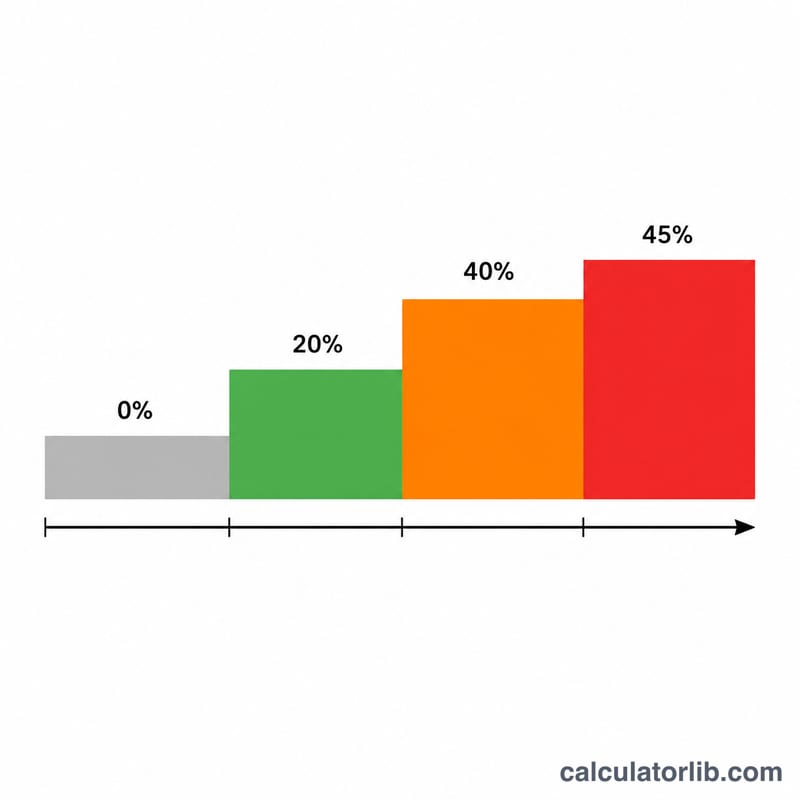

Everyone starts with a £12,570 personal allowance. Above £100,000 the allowance is reduced by £1 for every £2 earned, disappearing entirely at £125,140. Tax is then charged on your taxable income (income minus allowance): 20% on the first £37,700, 40% from £37,700 up to £125,140, and 45% on anything above £125,140.

$$\begin{gathered} \text{Tax} = 0.20\,T_1 + 0.40\,T_2 + 0.45\,T_3 \\[1.5em] \text{where}\quad \left\{ \begin{aligned} A &= 12570 - \max\!\left(0,\ \tfrac{\text{Income} - 100000}{2}\right) \\ T &= \max(0,\ \text{Income} - A) \\ T_1 &= \min(T,\ 37700) \\ T_2 &= \max(0,\ \min(T,\ 125140) - 37700) \\ T_3 &= \max(0,\ T - 125140) \end{aligned} \right. \end{gathered}$$

Worked example

On £120,000 income: the allowance is tapered by \((120{,}000 - 100{,}000)/2 = \text{£}10{,}000\), leaving £2,570. Taxable income is \(120{,}000 - 2{,}570 = \text{£}117{,}430\). Basic rate: \(37{,}700 \times 20\% = \text{£}7{,}540\). Higher rate: \((117{,}430 - 37{,}700) \times 40\% = 79{,}730 \times 40\% = \text{£}31{,}892\). Additional rate: £0. Total tax = £39,432, leaving £80,568 take-home.

FAQ

Why does my allowance disappear? Once income exceeds £100,000, HMRC tapers the personal allowance, creating an effective 60% marginal rate between £100,000 and £125,140.

Does this include National Insurance? No — this is income tax only. NI is calculated separately.

Is Scotland covered? No. Scotland has its own income tax bands; this calculator covers England, Wales and Northern Ireland.