What Is Jensen's Alpha?

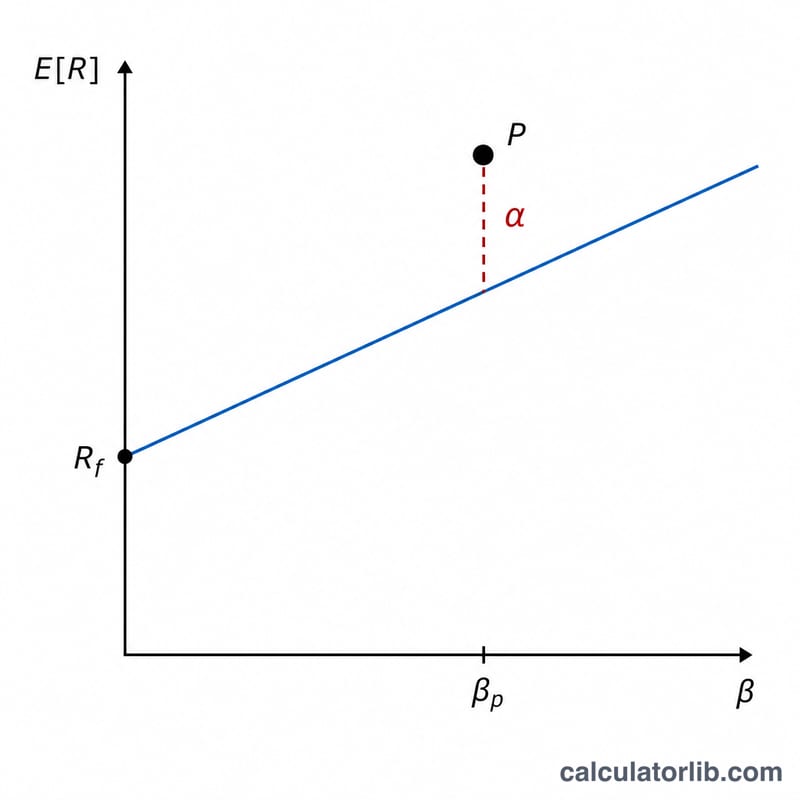

Jensen's Alpha is a risk-adjusted performance measure that tells you how much a portfolio or fund returned above or below what the Capital Asset Pricing Model (CAPM) predicted for its level of market risk. Developed by Michael Jensen in 1968, it isolates the value added (or lost) by a manager's skill after accounting for systematic risk, measured by beta. A positive alpha means the portfolio beat its risk-adjusted benchmark; a negative alpha means it lagged.

How to Use This Calculator

Enter four figures, all as percentages except beta: the portfolio's actual return, the risk-free rate (typically a short-term Treasury yield), the market's return (e.g. the S&P 500), and the portfolio's beta. The calculator computes the CAPM expected return and subtracts it from the actual return to give alpha.

The Formula Explained

$$\alpha = R_p - \left[ R_f + \beta \left( R_m - R_f \right) \right]$$ The bracketed term is the CAPM expected return: the risk-free rate plus beta times the market risk premium \((R_m - R_f)\). Subtracting it from the actual return \(R_p\) reveals the excess return not explained by exposure to market risk.

Worked Example

Suppose a portfolio returned 12%, the risk-free rate is 2%, the market returned 10%, and beta is 1.2. The expected return is $$2 + 1.2 \times (10 - 2) = 2 + 9.6 = 11.6\%.$$ Alpha = \(12 - 11.6 = \textbf{0.4\%}\). The manager added 0.4% of value beyond the risk taken.

FAQ

Is a higher alpha always better? Generally yes — a higher positive alpha indicates stronger risk-adjusted outperformance, but always confirm it is statistically significant and consistent over time.

What does negative alpha mean? The portfolio underperformed what its market risk warranted; the manager destroyed value relative to a passive CAPM benchmark.

Should returns be annualized? Yes. Keep all inputs on the same time basis (usually annual) so the comparison is consistent.