什麼是選擇權價差計算機?

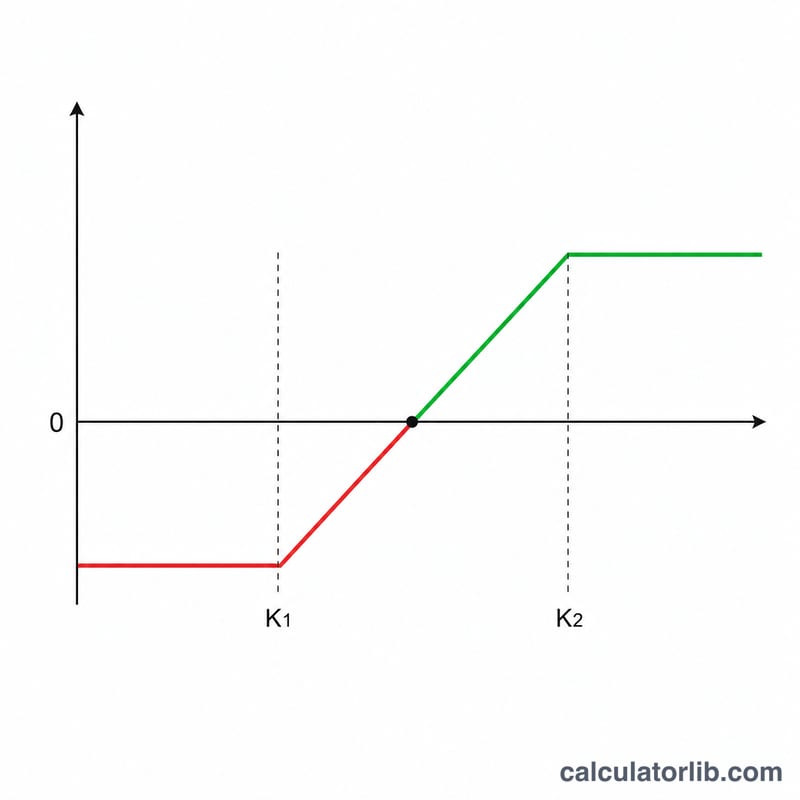

這項工具專門分析垂直借方價差(vertical debit spread),這是一種同時買進一口選擇權(買方部位)並賣出另一口相同類型、相同到期日但履約價不同的選擇權(賣方部位)的策略。由於買進那一腿付出的權利金高於賣出那一腿收取的權利金,建倉時會淨支出一筆權利金(借方)。計算機會立即算出你的淨權利金、最大獲利、最大虧損、損益兩平價格與風險報酬比,並同時提供每股與全部合約的數字。

使用方式

輸入買進選擇權所支付的權利金,以及賣出選擇權所收取的權利金,接著填入兩個履約價與合約口數。由於一口標準股票選擇權對應 100 股,計算機會將每股數字乘以 \(100 \times \text{合約口數}\),換算成你實際的美元損益。

公式說明

淨權利金 = 買方權利金 − 賣方權利金。這是你的成本基礎,同時也是你的最大虧損。最大獲利等於兩個履約價之間的差距減去淨權利金:\(\left|\,\text{賣方履約價} - \text{買方履約價}\,\right| - \text{淨權利金}\)。以多頭買權價差(bull call spread)來說,損益兩平點為買方履約價 + 淨權利金。

$$\begin{gathered} \text{Max Profit} = \left(\left|\,\text{Short Strike} - \text{Long Strike}\,\right| - D\right) \times 100 \times \text{Contracts} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} D &= \text{Long Premium} - \text{Short Premium} \\ \text{Breakeven} &= \text{Long Strike} + D \\ \text{Max Loss} &= D \times 100 \times \text{Contracts} \end{aligned} \right. \end{gathered}$$

實際範例

假設你以 5.00 美元買進一口履約價 100 美元的買權,同時以 2.00 美元賣出一口履約價 110 美元的買權,共一口合約。淨權利金 = \(5 - 2 = 3.00\) 每股美元。履約價差距 = 10。最大獲利 = \(10 - 3 = 7.00\) 每股美元,總計 700 美元。最大虧損 = 每股 3.00 美元,總計 300 美元。損益兩平點 = \(100 + 3 = 103\) 美元。風險報酬比 = \(7 \div 3 \approx 2.33\)。

常見問題

這也適用於信用價差(credit spread)嗎?本工具是為借方價差設計的。信用價差會產生負的淨權利金,只要把獲利與虧損的正負號對調即可。

為什麼要乘以 100?每一口美股選擇權合約代表 100 股標的,因此美元損益等於每股價值乘以 100 再乘以合約口數。

有把手續費算進去嗎?沒有。若想得到更精準的淨損益,請從結果中扣除券商按每口收取的交易費用。