What This Calculator Does

The Auto Loan Calculator estimates your monthly car payment based on the vehicle price, down payment, trade-in value, interest rate (APR), loan term, sales tax, and additional fees. It also shows the total amount financed, total interest you will pay over the life of the loan, and the grand total of all payments.

How to Use It

Enter the vehicle's negotiated price, any cash down payment, and the value of a vehicle you are trading in. Add your sales tax rate and any title, registration, or dealer fees. Then enter the APR your lender quoted and the loan term in months (48, 60, and 72 months are common). The calculator instantly returns your estimated monthly payment.

The Formula Explained

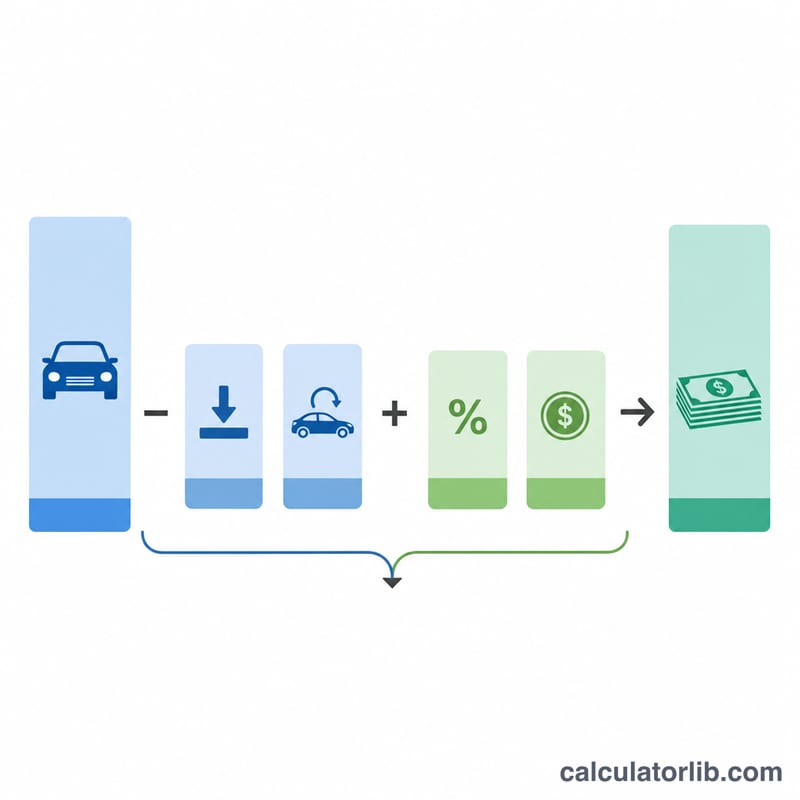

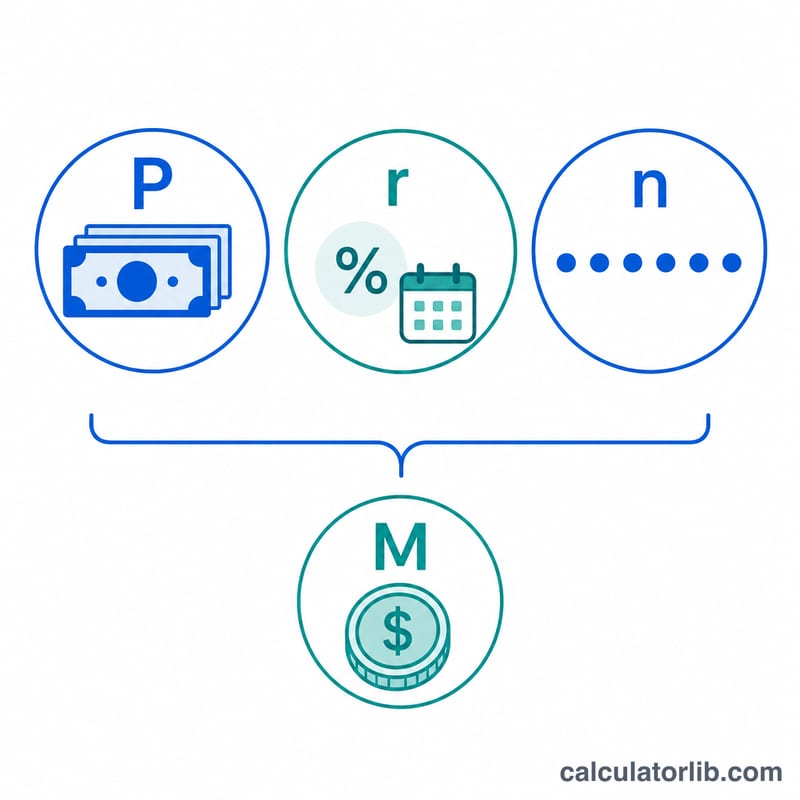

First the amount financed (principal) is computed: price minus down payment minus trade-in, plus sales tax (price × tax rate) and fees. The monthly payment uses the standard amortization formula $$M = P \cdot \frac{r(1+r)^n}{(1+r)^n - 1}$$, where \(r\) is the monthly interest rate (APR ÷ 12 ÷ 100) and \(n\) is the number of months. If the APR is 0%, the payment is simply the principal divided by the term.

Worked Example

Suppose you finance $33,000 at a 6.5% APR over 60 months. The monthly rate is \(0.065 \div 12 = 0.00541667\). Plugging into the formula gives a monthly payment of about $645.62. Over 60 months you pay roughly $38,737, of which about $5,737 is interest.

Key Terms Defined

- APR (Annual Percentage Rate)

- The yearly cost of borrowing expressed as a percentage. For a simple-interest auto loan it is the nominal annual rate used to compute the monthly rate. A true APR that includes finance charges and fees can be slightly higher than the quoted note rate.

- Amount Financed / Principal (P)

- The actual loan balance you borrow. It equals the vehicle price minus your down payment and trade-in value, plus any sales tax and fees that are rolled into the loan.

- Down Payment

- Cash you pay up front toward the purchase. It reduces the amount financed dollar for dollar, lowering both the monthly payment and total interest.

- Trade-In Value

- The credit a dealer gives you for your old vehicle. Like a down payment, it reduces the amount financed. In many states it also lowers the taxable amount.

- Sales Tax

- A percentage of the purchase price charged by your state or locality. It is often added to the financed amount rather than paid separately at signing.

- Dealer / Title / Registration Fees

- Additional charges such as documentation ("doc") fees, title transfer, registration, and license fees. These are frequently bundled into the loan and increase the principal.

- Loan Term (n)

- The repayment period in months — common terms are 48, 60, and 72 months. A longer term lowers the monthly payment but increases total interest paid.

- Monthly Rate (r)

- The periodic interest rate per month, calculated as the APR divided by 12 (in the formula, \(r = \text{APR}/1200\) so a percentage becomes a decimal). It is the rate applied to the outstanding balance each month.

Understanding Your Result

The calculator returns three related figures that describe the full cost of your loan.

The monthly payment (M) is the fixed amount you owe each month for the entire term. It covers both interest and a portion of the principal so that the balance reaches zero with the final payment.

The total amount financed (P) is the loan principal — the price after subtracting your down payment and trade-in, then adding any sales tax and fees that are rolled into the loan. Everything you borrow, including taxes and fees, accrues interest, so financing those costs raises both your payment and your total interest.

The total interest is the difference between everything you pay over the term (\(M \times n\)) and the amount financed. It is the price of borrowing and grows with a higher APR or a longer term.

Negative equity (being "upside down"). If your trade-in is worth less than the balance still owed on it, that shortfall is typically added to the new loan. For instance, a vehicle worth $8,000 with a $10,000 remaining balance carries $2,000 of negative equity, which increases the new amount financed — meaning you finance, and pay interest on, debt from the previous car.

Quoted APR vs. actual cost. The payment shown assumes the APR you enter is the effective rate and that you pay on schedule. The true cost of credit can differ once certain finance charges or fees are included, so the disclosed APR on your contract may be slightly higher than the note rate. Paying late, paying early, or refinancing will also change your actual interest.

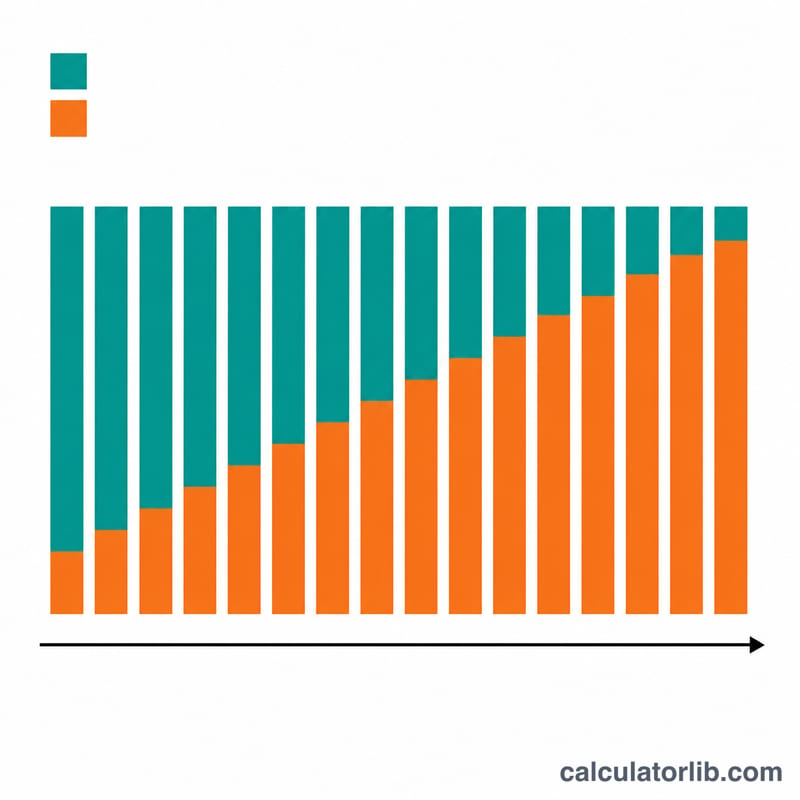

How amortization shifts over time. Although the monthly payment stays constant, its makeup does not. Early payments are mostly interest because the balance is large; as the balance falls, more of each payment goes to principal. This is why paying extra early in the loan saves the most interest, and why total interest is heavily front-loaded.

FAQ

Does this include sales tax? Yes — sales tax is calculated on the vehicle price and added to the amount financed (a common dealer practice). Adjust the rate to match your state.

Should I include my trade-in? Yes. The trade-in value reduces the amount you need to finance, just like a down payment.

Is the APR the same as the interest rate? Roughly. This tool treats the entered APR as the nominal annual rate compounded monthly, which closely matches how most auto lenders quote loans.