What is the Time Value of Money?

The time value of money (TVM) is the core idea in finance that a dollar today is worth more than a dollar in the future, because money can earn interest over time. This calculator computes the future value (FV) of an investment that starts with a present value (PV) and receives equal periodic payments (PMT), all growing at a fixed interest rate per period.

How to use it

Enter your starting amount as the Present Value, the recurring deposit per period as the Periodic Payment, the interest rate per period (as a percent), and the total number of periods. If you contribute monthly, use the monthly rate (annual rate ÷ 12) and the number of months. The calculator returns the future value, your total contributions, and the interest earned.

The formula explained

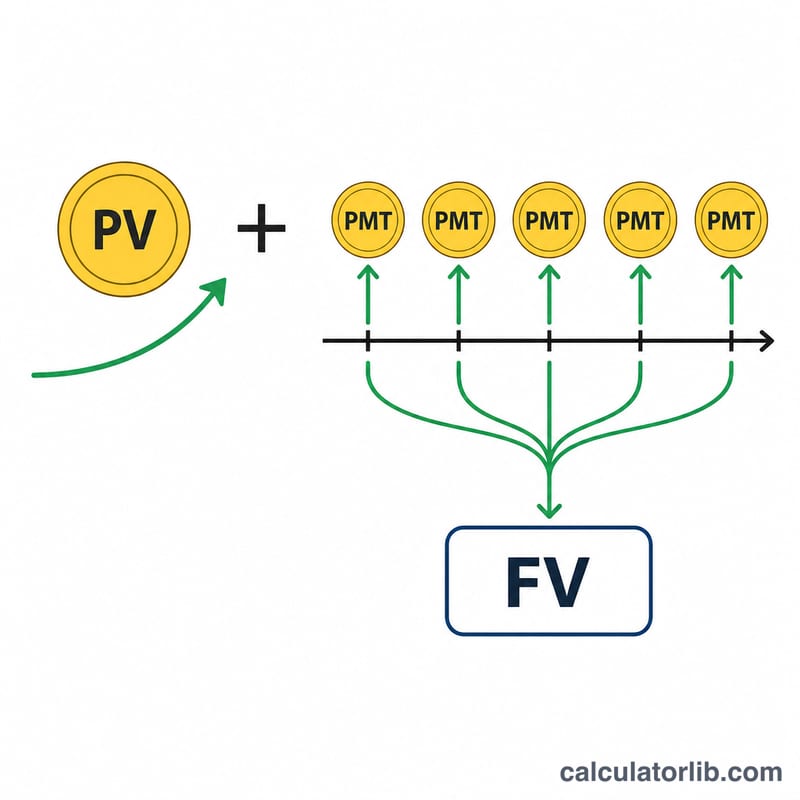

The equation has two parts. The first, \(\text{PV}\,(1+r)^n\), compounds your initial lump sum forward. The second, \(\text{PMT}\,\dfrac{(1+r)^n - 1}{r}\), is the future value of an ordinary annuity — a series of equal payments made at the end of each period. Adding them gives the total accumulated value:

$$\text{FV} = \text{PV}\,(1+r)^n + \text{PMT}\,\dfrac{(1+r)^n - 1}{r}$$When the rate is exactly 0%, the formula safely reduces to

$$\text{FV} = \text{PV} + \text{PMT}\cdot n$$

Worked example

Suppose PV = 1,000, PMT = 100, rate = 5% per period, and n = 10 periods. Then \((1.05)^{10} \approx 1.628895\).

$$\text{FV} = 1{,}000 \times 1.628895 + 100 \times \dfrac{1.628895 - 1}{0.05} \approx 1{,}628.89 + 1{,}257.79 = 2{,}886.68$$Total contributions are \(1{,}000 + 100\times 10 = 2{,}000\), so interest earned is about 886.68.

FAQ

Does this assume payments at the start or end of the period? It assumes end-of-period payments (an ordinary annuity), the most common convention.

Can I model only a lump sum? Yes — set the periodic payment to 0 and you get straight compound interest.

What rate should I enter? Use the rate per period, matching the period of your payments. For monthly compounding, divide the annual rate by 12.