什麼是貨幣的時間價值?

貨幣時間價值(Time Value of Money,TVM)是理財與財務領域最核心的觀念:今天的一塊錢,比未來的一塊錢更有價值,因為錢能隨著時間賺取利息、產生複利。這個計算機會幫你算出一筆投資的未來終值(FV)——從一筆現值(PV)出發,每期再固定投入相同金額(PMT),並以固定的每期利率持續累積成長。

使用方式

把你的起始金額填入現值(PV),每期固定投入的金額填入定期投入(PMT),再輸入每期利率(以百分比表示)與總期數。如果你是每月投入,就用月利率(年利率 ÷ 12)搭配總月份數。計算完成後,會顯示未來終值、你總共投入的本金,以及賺到的利息。

公式說明

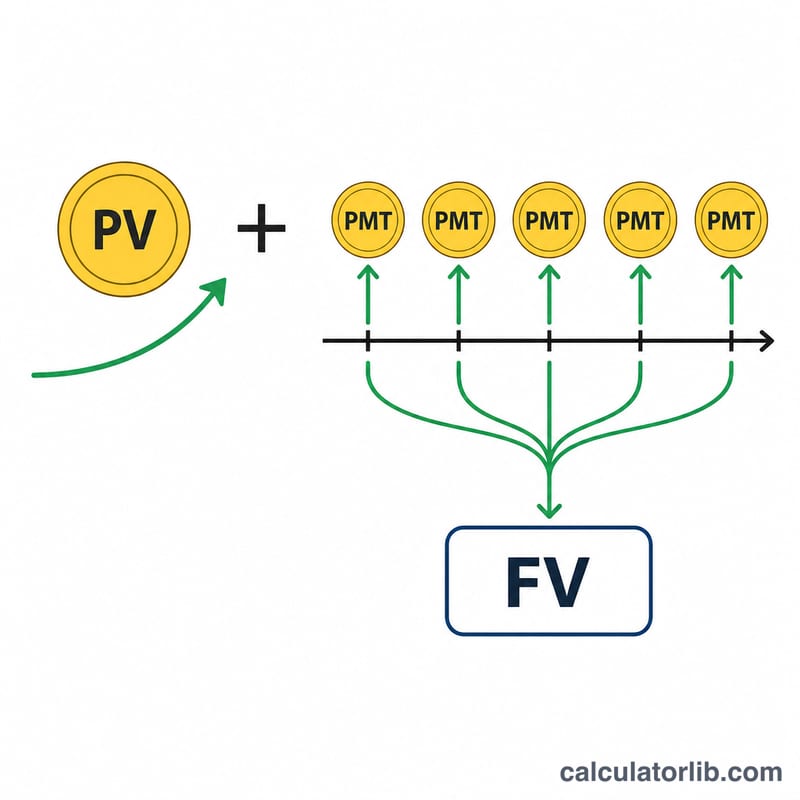

整個算式分成兩個部分。

$$\text{FV} = \text{PV}\,(1+r)^n + \text{PMT}\,\dfrac{(1+r)^n - 1}{r}$$第一部分 \(\text{PV}\cdot(1+r)^n\) 把你最初投入的整筆金額往未來複利成長;第二部分 \(\text{PMT}\cdot\dfrac{(1+r)^n - 1}{r}\) 則是普通年金(ordinary annuity)的終值,也就是每期期末投入一筆相同金額所累積的價值。把兩者相加,就是最終累積的總金額。當利率恰好為 0% 時,公式會自動簡化為安全的 \(\text{FV} = \text{PV} + \text{PMT}\cdot n\)。

實際範例

假設 PV = 1,000、PMT = 100、每期利率 = 5%、n = 10 期。那麼 \((1.05)^{10} \approx 1.628895\)。

$$\text{FV} = 1{,}000 \times 1.628895 + 100 \times \frac{1.628895 - 1}{0.05} \approx 1{,}628.89 + 1{,}257.79 = 2{,}886.68$$總投入本金為 \(1{,}000 + 100 \times 10 = 2{,}000\),因此賺到的利息約為 886.68。

常見問題

這是假設在期初還是期末投入?本計算機假設於每期期末投入(即普通年金),這也是最常見的計算慣例。

我可以只試算一筆整存的金額嗎?可以——把定期投入設為 0,得到的就是單純的複利計算結果。

我應該填哪一種利率?請填入「每期」的利率,並與你投入的週期一致。若採月複利,就把年利率除以 12。