What Is a Carry Trade?

A carry trade is a strategy where you borrow (go short) in a low-interest-rate currency and invest (go long) in a higher-interest-rate currency, pocketing the interest rate differential. The catch is that your return also depends on how the exchange rate between the two currencies moves over the holding period. This calculator combines both effects into a single estimated return.

How to Use It

Enter the notional size of your position, the interest rate of the long (high-yield) currency, the interest rate of the short (funding) currency, and the expected or realized percentage change in the exchange rate. The tool returns your total percentage carry return and the estimated profit or loss in currency terms.

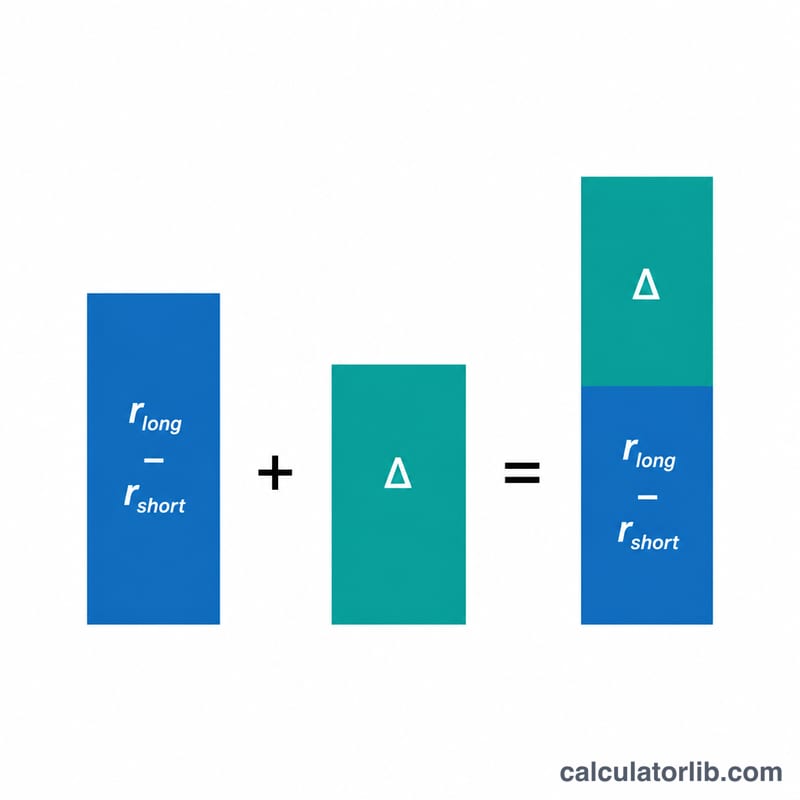

The Formula Explained

The core relationship is Carry Return = (Interest Rate Long − Interest Rate Short) + Exchange Rate Change. The first part is the interest rate differential, the steady "carry" you earn for holding the trade. The second part, the exchange rate change, can amplify or wipe out that carry. A favorable FX move adds to returns; an adverse one subtracts. Profit is simply the notional multiplied by the return divided by 100.

$$\text{Profit} = \text{Notional} \times \frac{\left(\text{Long Rate} - \text{Short Rate}\right) + \text{FX Change}}{100}$$

Worked Example

Suppose you go long a currency yielding 5% and fund it with one yielding 0.5%, on a notional of 10,000. Over the period the exchange rate moves −1% against you. The interest differential is \(5 - 0.5 = 4.5\%\). Adding the −1% FX change gives a total return of 3.5%. On 10,000 notional that is a profit of $$10000 \times \frac{(5 - 0.5) + (-1)}{100} = 350.$$

FAQ

Why can a carry trade lose money? Even with a positive interest differential, a large adverse currency move can exceed the carry and produce a net loss.

Is this annualized? The result is expressed over the period of the rates and FX change you enter. Use period-matched rates for accurate results.

Does this include leverage or transaction costs? No. The notional is treated as the full position size; add your own spread, swap, and financing costs for a more precise figure.