What Is Residual Income?

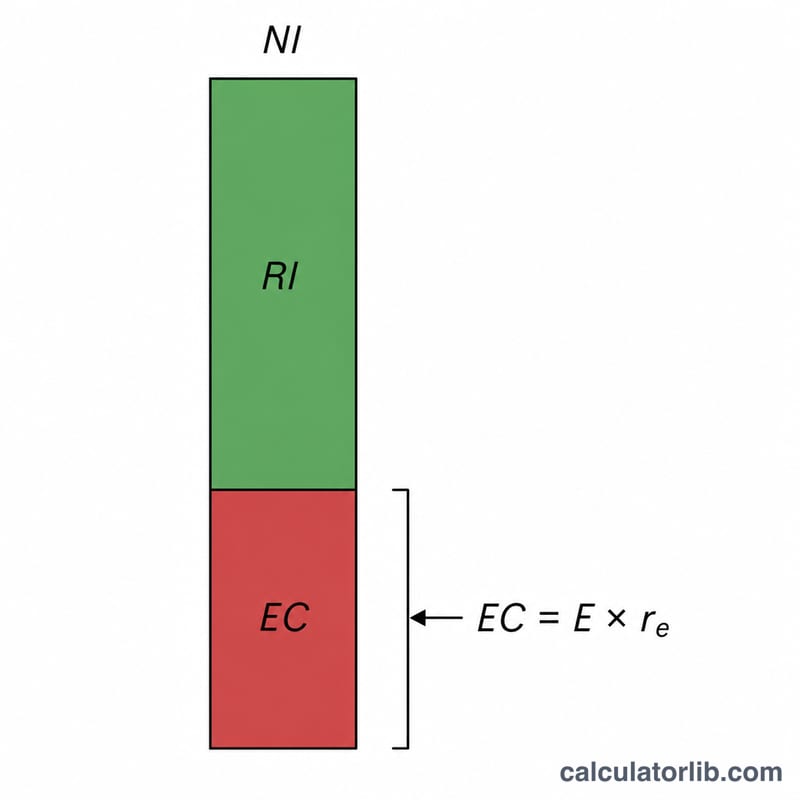

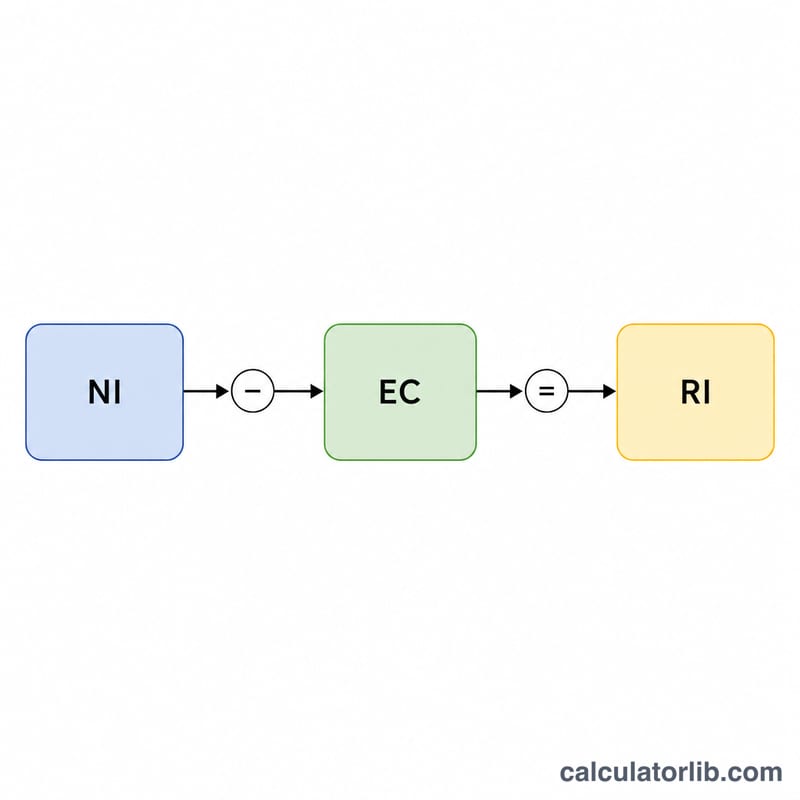

Residual income (RI), also called economic profit, measures the value a business or investment creates after accounting for the cost of the equity capital it uses. Unlike accounting net income, residual income subtracts a charge for shareholders' required return — so a positive figure means the company earned more than its investors' minimum expectation, while a negative figure means it destroyed value despite being profitable on paper.

How to Use This Calculator

Enter three values: Net Income (the company's after-tax profit), Equity (the book value of shareholders' equity or invested capital), and the Cost of Equity as a percentage (the rate of return investors require). The calculator multiplies equity by the cost-of-equity rate to get the equity charge, then subtracts it from net income to reveal the residual income.

The Formula Explained

The core equation is:

$$\text{Residual Income} = \text{Net Income} - \left(\text{Equity} \times \text{Cost of Equity}\right)$$

The term Equity × Cost of Equity is the "equity charge" — the dollar return shareholders demand for the capital tied up in the business. Net income above this hurdle is genuine economic profit.

Worked Example

Suppose a firm reports net income of $100,000, has $500,000 of equity, and shareholders require a 10% return. The equity charge is \(\$500{,}000 \times 10\% = \$50{,}000\). Residual income $$= \$100{,}000 - \$50{,}000 = \mathbf{\$50{,}000}$$ The company created $50,000 of value above what investors required.

FAQ

Is residual income the same as net income? No. Net income ignores the cost of equity; residual income deducts it, giving a truer picture of value creation.

Can residual income be negative? Yes. If net income is below the equity charge, RI is negative — the firm earned less than its cost of capital.

What cost of equity should I use? Many analysts estimate it with the Capital Asset Pricing Model (CAPM) or use the investor's required rate of return.