What this calculator does

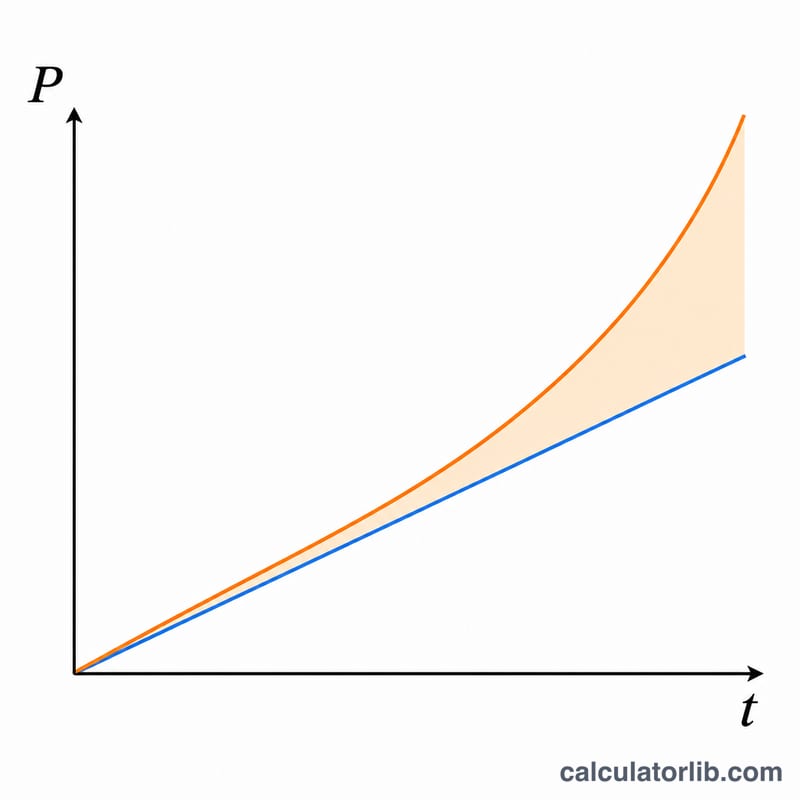

This tool compares two ways your money can grow over time: simple interest, where interest is paid only on your original principal, and compound interest, where each year's interest is added back so future interest is earned on a larger balance. Enter a principal, an annual interest rate and a number of years, and the calculator shows both final balances, the interest earned under each method, and the difference between them. The math is universal, so the "currency units" can be dollars, euros, yen or any currency you like.

How to use it

1. Enter the Principal — the amount you deposit or invest at the start. 2. Enter the Interest rate as an annual percentage (for example 3 for 3%). 3. Enter the number of Years the money is held. The result highlights the difference (compound minus simple) and lists each total and interest amount in the table below.

The formula explained

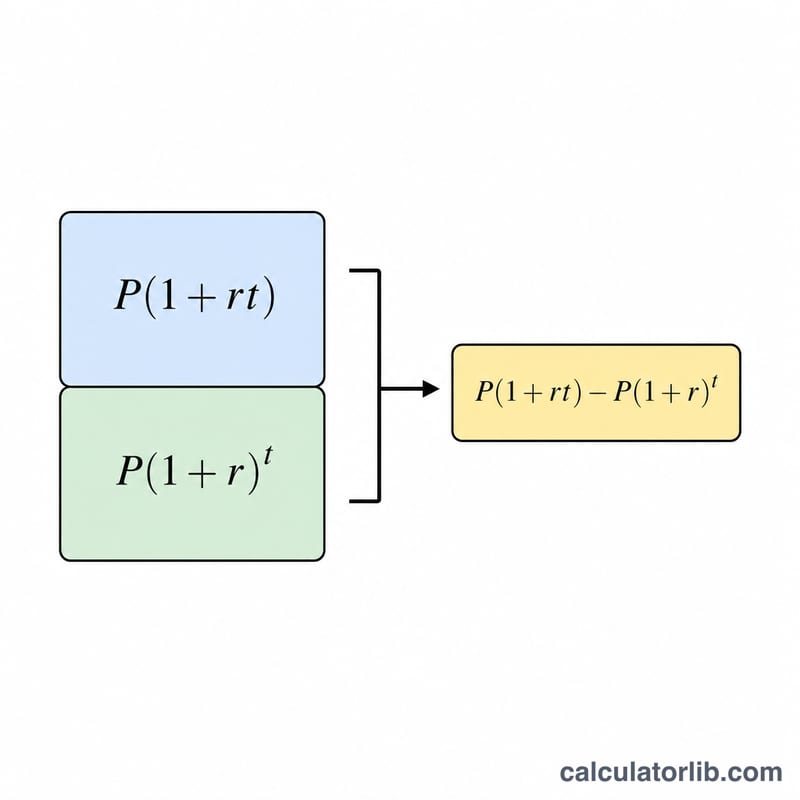

Let P be the principal, r the annual rate as a decimal (rate ÷ 100) and t the number of years. Simple interest total is \(S = P(1 + r\times t)\) and the interest earned is \(P\times r\times t\). Compound interest total is \(C = P(1 + r)^{t}\) and the interest earned is \(C - P\). The difference is therefore $$\Delta = P\left[(1 + r)^{t} - (1 + r\times t)\right]$$ This tool assumes interest compounds once per year.

Worked example

With a principal of 3,000,000, a 3% annual rate and 30 years: \(r = 0.03\). Simple total = $$3{,}000{,}000 \times (1 + 0.03 \times 30) = 3{,}000{,}000 \times 1.9 = 5{,}700{,}000$$ with 2,700,000 interest. Compound total = $$3{,}000{,}000 \times 1.03^{30} \approx 7{,}281{,}786$$ with about 4,281,786 interest. The difference is roughly 1,581,786 — that is how much more compounding earns over those 30 years.

FAQ

When does compound interest pull ahead? Only from year 2 onward. For \(t = 1\) (or when the rate is 0%, or \(t = 0\)) both methods give exactly the same result, so the difference is zero.

Does this support monthly compounding? No. This calculator uses annual (once-per-year) compounding only.

Why might my bank show a slightly different number? Financial institutions round or truncate fractional amounts according to their own rules, so the final figure can differ by a small amount. This calculator keeps full precision internally and rounds only for display.