What Is the Working Capital Turnover Ratio?

The working capital turnover ratio measures how efficiently a company uses its working capital — the difference between current assets and current liabilities — to generate sales. A higher ratio indicates the business is converting its capital into revenue effectively, while a very low ratio may signal idle or excess working capital tied up in inventory and receivables.

How to Use This Calculator

Enter your net sales for the period, your average current assets, and your average current liabilities. The calculator subtracts liabilities from assets to find average working capital, then divides net sales by that figure to produce the turnover ratio expressed as "times per period."

The Formula Explained

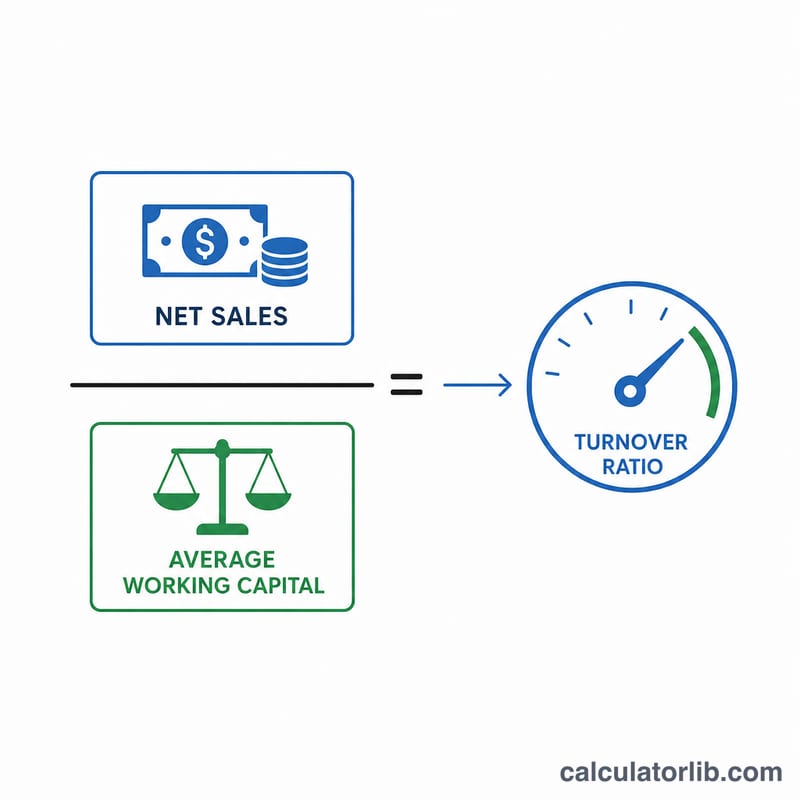

The core formula is $$\text{WC Turnover} = \frac{\text{Net Sales}}{\text{Average Working Capital}}$$, where \(\text{Average Working Capital} = \text{Current Assets} - \text{Current Liabilities}\). "Average" typically uses the mean of beginning and ending balances, but a single period figure works too. Net sales should exclude returns and allowances.

Worked Example

Suppose a company has net sales of $500,000, average current assets of $200,000, and average current liabilities of $100,000. Working capital is \(\$200{,}000 - \$100{,}000 = \$100{,}000\). The turnover ratio is $$\$500{,}000 \div \$100{,}000 = 5.0$$ This means the company generates $5 of sales for every $1 of working capital.

FAQ

What is a good working capital turnover ratio? It varies by industry, but generally a higher ratio is favorable. Compare against industry peers and prior periods rather than a fixed benchmark.

Can the ratio be negative? Yes. If current liabilities exceed current assets, working capital is negative, producing a negative ratio that signals potential liquidity problems.

What period should I use? Most analysts use annual figures, but quarterly data works for tighter monitoring as long as net sales and working capital cover the same period.