What Is the Additional Funds Needed (AFN) Calculator?

The Additional Funds Needed (AFN) method estimates how much external financing a company must raise to support a projected increase in sales. As sales grow, a firm typically needs more assets (inventory, receivables, equipment). Part of that growth funds itself through spontaneous liabilities (like accounts payable) and retained earnings, but any shortfall must come from new debt or equity. This calculator quantifies that shortfall.

How to Use It

Enter your current (base) sales, your projected sales for next period, your spontaneous assets and spontaneous liabilities (those that rise naturally with sales), your net profit margin as a percentage, and your retention ratio (the share of earnings kept rather than paid as dividends). The calculator returns the AFN along with each component so you can see what drives the number.

The Formula Explained

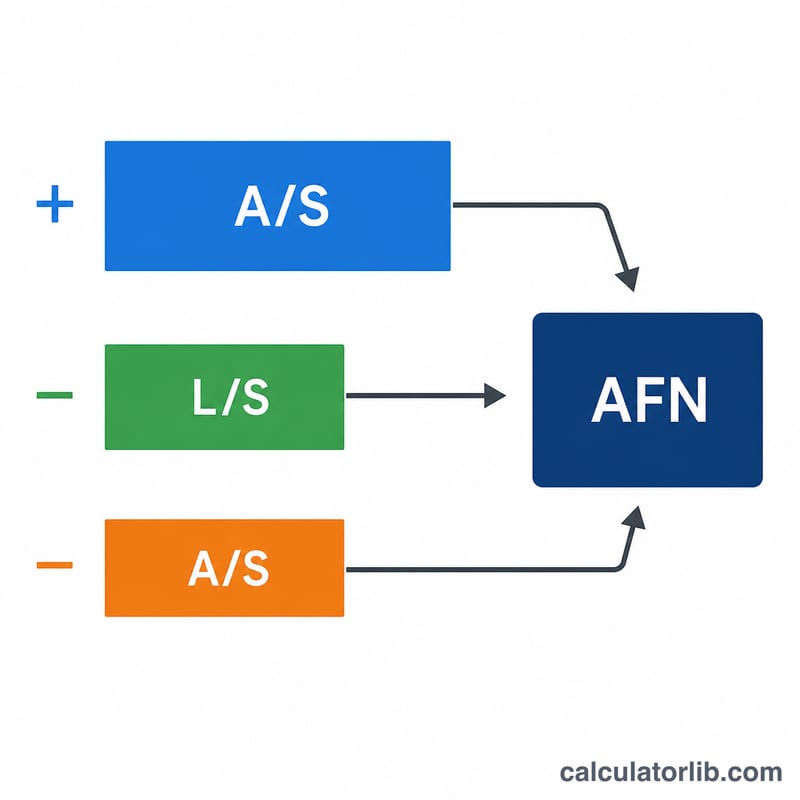

$$\text{AFN} = \frac{A}{S}\Delta S - \frac{L}{S}\Delta S - (PM \times S_1 \times RR)$$ where \(A/S\) is the asset-to-sales ratio, \(L/S\) is the spontaneous-liability-to-sales ratio, \(\Delta S\) is the change in sales, \(PM\) is the net profit margin, \(S_1\) is projected sales, and \(RR\) is the retention ratio. The first term is the required asset growth, the second is automatic financing from liabilities, and the third is internally generated funds retained in the business.

Worked Example

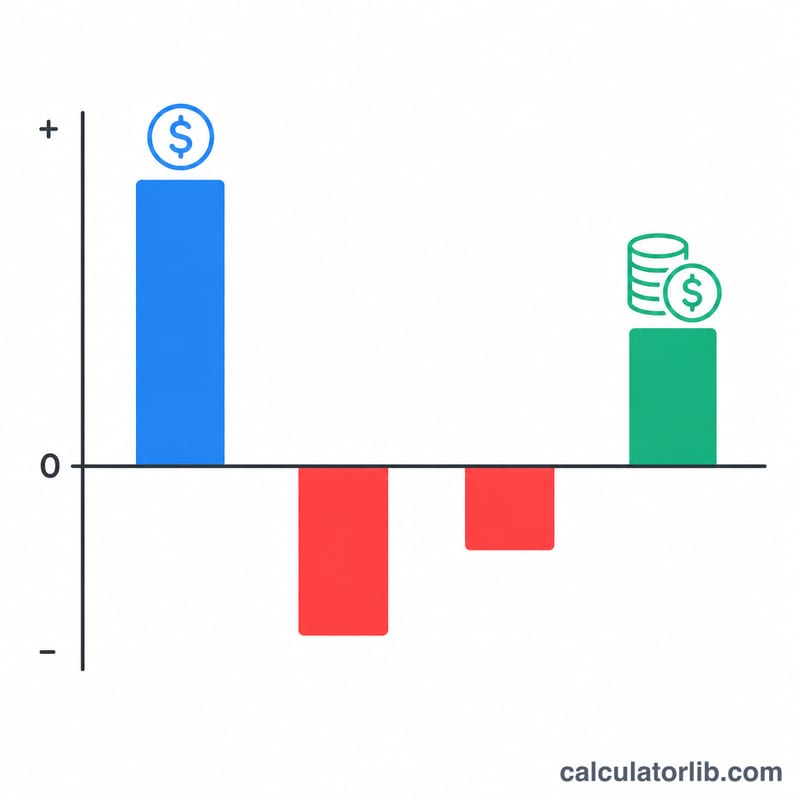

Current sales $200,000, projected $300,000 (\(\Delta S = \$100{,}000\)), assets $100,000, liabilities $10,000, profit margin 5%, retention 60%. Asset increase = $$\frac{100{,}000}{200{,}000}\times 100{,}000 = \$50{,}000.$$ Liability increase = $$\frac{10{,}000}{200{,}000}\times 100{,}000 = \$5{,}000.$$ Retained earnings = $$0.05\times 300{,}000\times 0.60 = \$9{,}000.$$ AFN = $$50{,}000 - 5{,}000 - 9{,}000 = \mathbf{\$36{,}000}.$$

Interpreting Your AFN Result

The sign of the AFN figure tells you whether projected growth can be funded from within the business or requires outside money.

- Positive AFN means the assets required to support higher sales exceed the funds generated spontaneously by liabilities and by retained earnings. This is an external financing gap that must be closed with new debt, new equity, or some combination — the model identifies the size of the gap but does not prescribe how to fill it.

- Zero AFN means spontaneous liabilities plus retained earnings exactly cover the new asset requirement. Growth is, in effect, self-financing at that combination of inputs.

- Negative AFN indicates a financing surplus: internally generated funds more than cover the asset needs of growth. The surplus could be used to pay down debt, increase dividends, build cash, or fund other investments.

Keep the model's assumptions in mind when reading the number. The basic AFN equation assumes that the asset and spontaneous-liability ratios stay constant as sales change (a linear relationship), and that fixed assets are operating at full capacity so they must grow in step with sales. If the company has excess capacity, the true asset requirement — and therefore the AFN — will be smaller than the formula suggests. The equation also assumes a stable profit margin and a stable dividend payout, so the retained-earnings term moves only with projected sales.

AFN is a planning estimate, not a precise financing plan. It sizes the funding gap so you can begin a more detailed analysis of capital structure, timing, and cost of capital. This is general educational information, not personalized financial advice.

Key Terms and Variables

- Spontaneous Assets (\(A\))

- Assets that increase more or less automatically as sales rise — typically cash, accounts receivable, inventory, and fixed assets operating at full capacity. These are the assets included in the \(A/S_0\) ratio.

- Spontaneous Liabilities (\(L\))

- Liabilities that grow automatically with sales without an explicit financing decision, chiefly accounts payable and accrued wages and taxes. They provide "free" funding that reduces the amount that must be raised externally.

- A/S Ratio (Asset Intensity)

- Spontaneous assets divided by current sales, \(A/S_0\). It measures how many dollars of assets are needed to support each dollar of sales. Multiplying by \(\Delta S\) gives the new assets required for growth.

- L/S Ratio

- Spontaneous liabilities divided by current sales, \(L/S_0\). Multiplying by \(\Delta S\) gives the spontaneous financing automatically supplied as sales grow.

- Change in Sales (\(\Delta S\))

- Projected sales minus current sales, \(S_1 - S_0\). This is the absolute increase in revenue that the firm must fund.

- Net Profit Margin (\(M\))

- Net income as a fraction of sales, entered as a percentage and converted with \(M = \text{PM}\%/100\). It determines how much profit each dollar of projected sales generates.

- Projected Sales (\(S_1\))

- The expected sales level for the forecast period. It drives both the change in sales and the amount of retained earnings generated, \(M \cdot S_1 \cdot b\).

- Retention (Plowback) Ratio (\(b\))

- The fraction of net income kept in the business rather than paid out as dividends, entered as a percentage and converted with \(b = \text{RR}\%/100\). It equals \(1\) minus the dividend payout ratio.

- Additional Funds Needed (AFN)

- The external financing required to support projected sales growth, after accounting for spontaneous liabilities and retained earnings. A positive value is a funding gap; a negative value is a surplus.

FAQ

What if AFN is negative? A negative AFN means internally generated funds and spontaneous liabilities more than cover the asset growth — the firm has a surplus.

What are spontaneous assets and liabilities? They are balance-sheet items that change in direct proportion to sales, such as inventory, receivables, and accounts payable. Long-term debt and equity are not spontaneous.

Is the retention ratio the same as the plowback ratio? Yes — it is 1 minus the dividend payout ratio, representing the fraction of profit reinvested.