What This Calculator Does

The Salary Needed for a Mortgage Calculator estimates the gross annual income you'd typically need to qualify for a given home loan. It is based on the common front-end debt-to-income (DTI) rule, which says your monthly housing payment should not exceed about 28% of your gross monthly income. This guideline is most widely used in the United States, but the underlying math works anywhere — just adjust the DTI ratio to match your lender's standards.

How to Use It

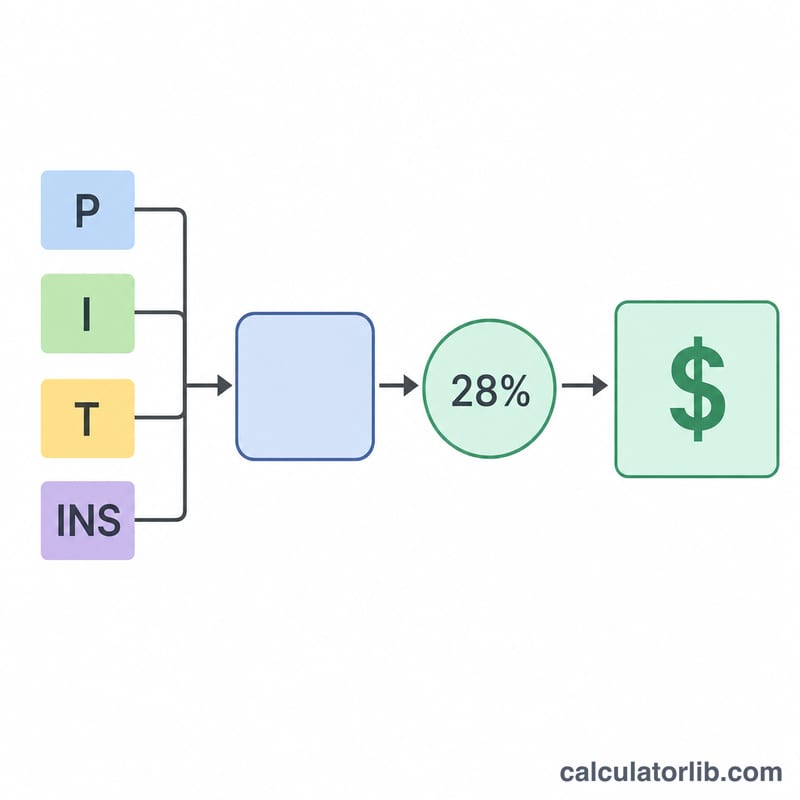

Enter the loan amount, the annual interest rate, and the loan term in years. Optionally add your annual property tax and home insurance so the result reflects your full PITI (principal, interest, taxes, insurance) payment. You can also change the front-end DTI ratio if your lender uses a different threshold. The calculator returns the salary needed, your required monthly income, and a breakdown of the monthly payment.

The Formula Explained

First the monthly principal and interest is computed with the standard amortization formula \(PI = L \cdot \dfrac{i(1+i)^{n}}{(1+i)^{n} - 1}\), where \(i\) is the monthly interest rate and \(n\) is the number of monthly payments. Monthly taxes and insurance are added to get the total monthly housing cost. That cost is annualized and divided by the DTI ratio: $$\text{Required Salary} = \frac{12 \times \text{Monthly Payment}}{0.28}$$

Worked Example

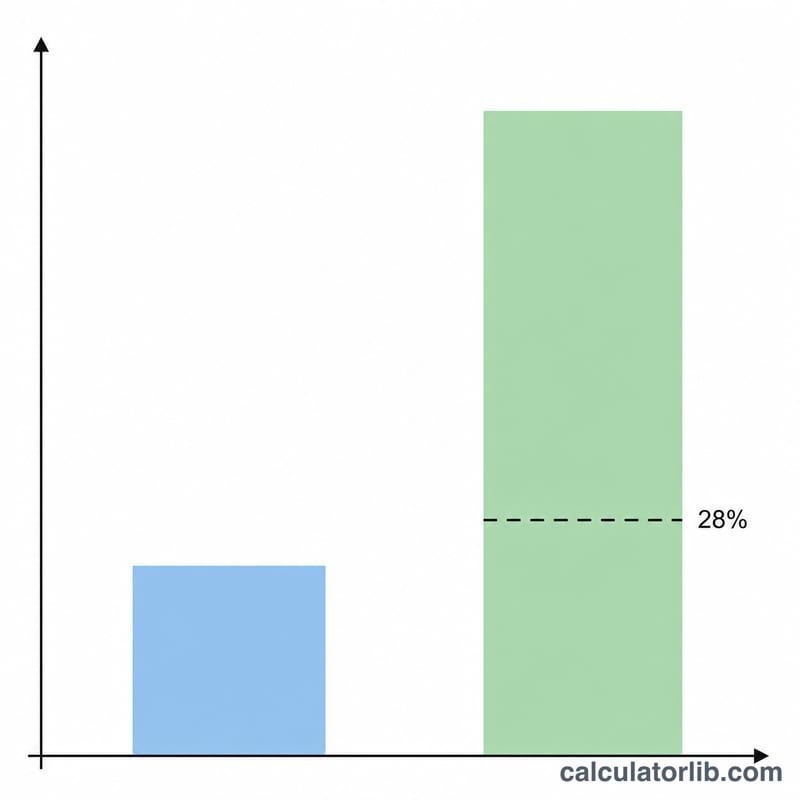

Suppose you want a $300,000 loan at 6.5% over 30 years with no taxes or insurance. The monthly principal and interest is about $1,896.20. Annualized that's $22,754.43. Dividing by 0.28 gives a required salary of roughly $81,266 per year, or about $6,772 per month.

$$\text{Required Salary} = \frac{12 \times 1{,}896.20}{0.28} = \frac{22{,}754.43}{0.28} \approx 81{,}266$$

FAQ

Why 28%? The 28% front-end ratio is a long-standing lending benchmark for the share of gross income that should go toward housing. Some lenders allow more.

Should I include taxes and insurance? Yes — including them gives a more realistic PITI payment and a higher, more accurate salary estimate.

Does this guarantee approval? No. Lenders also consider your other debts (back-end DTI), credit score, and down payment. Treat this as a planning estimate.