What Is Funds From Operations (FFO)?

Funds From Operations (FFO) is the standard performance metric for Real Estate Investment Trusts (REITs), defined by the National Association of Real Estate Investment Trusts (Nareit). Because real estate properties are depreciated on the income statement even though they often appreciate in value, ordinary net income understates a REIT's true cash-generating ability. FFO corrects for this by adding depreciation and amortization back to net income and stripping out one-time gains or losses from selling properties.

How to Use This Calculator

Enter the figures from the REIT's income statement: net income, real-estate depreciation, amortization, any losses on property sales (added back), and any gains on property sales (subtracted). The calculator returns FFO for the period along with a breakdown of each component.

The Formula Explained

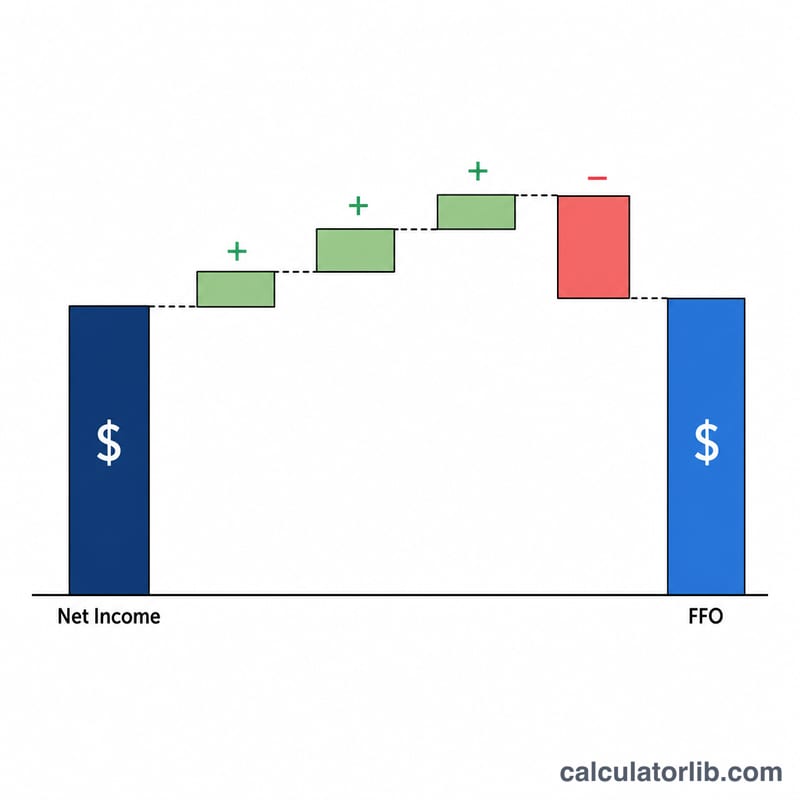

$$\text{FFO} = \text{Net Income} + \text{Depreciation} + \text{Amortization} + \text{Losses on Sales} - \text{Gains on Sales}$$ Depreciation and amortization are non-cash charges, so they are added back. Gains on selling property are non-recurring and are removed, while losses are added back, leaving a cleaner picture of recurring operating performance.

Worked Example

A REIT reports net income of $5,000,000, depreciation of $2,000,000, amortization of $500,000, no losses on sales, and a $1,000,000 gain on a property sale. $$\text{FFO} = 5{,}000{,}000 + 2{,}000{,}000 + 500{,}000 + 0 - 1{,}000{,}000 = \mathbf{\$6{,}500{,}000}$$

FAQ

Is higher FFO always better? Generally yes, as it indicates stronger operating cash flow, but compare it on a per-share basis and against the dividend payout.

How does FFO differ from AFFO? Adjusted FFO (AFFO) further subtracts recurring capital expenditures and straight-line rent adjustments to better approximate distributable cash.

Why not just use net income? GAAP net income includes large non-cash depreciation charges that distort a REIT's economic reality, which is why Nareit promotes FFO.