What is the Bike EMI Calculator?

The Bike EMI Calculator helps you estimate the Equated Monthly Installment (EMI) for a two-wheeler loan. An EMI is the fixed amount you pay every month until the loan is fully repaid, covering both principal and interest. By entering the loan amount, annual interest rate, and tenure, you instantly see your monthly outgo and the total cost of the loan.

How to Use It

Enter the loan amount (bike price minus your down payment), the lender's annual interest rate as a percentage, and the loan tenure in months. The calculator returns your monthly EMI, the total interest payable over the loan term, and the total amount (principal + interest) you will repay.

The Formula Explained

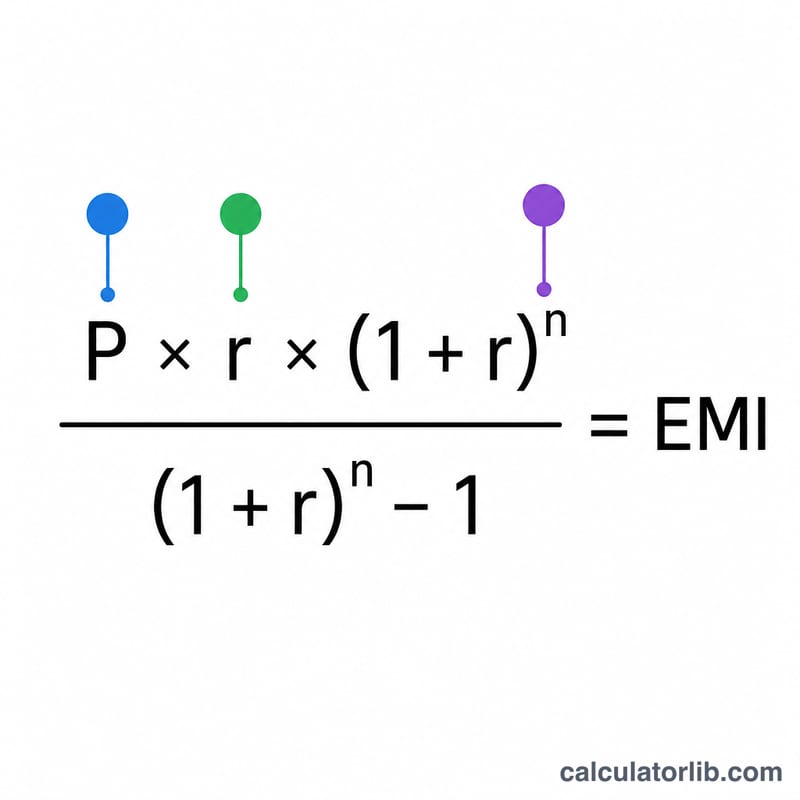

The EMI is calculated using the reducing-balance formula: $$\text{EMI} = P \cdot \frac{r\,(1+r)^{n}}{(1+r)^{n}-1}$$ where \(P\) is the principal, \(r\) is the monthly interest rate (annual rate divided by 12 and by 100), and \(n\) is the number of monthly installments. When the interest rate is zero, the EMI is simply the principal divided by the number of months.

Worked Example

For a loan of ₹80,000 at 10% annual interest over 24 months: the monthly rate \(r = 10 \div 12 \div 100 = 0.0083333\). Applying the formula gives an EMI of about ₹3,693.57. Over 24 months that totals roughly ₹88,645.67, meaning total interest of about ₹8,645.67.

Key Terms Explained

- EMI (Equated Monthly Installment)

- The fixed amount you pay every month until the loan is fully repaid. Each EMI covers both interest and a portion of the principal.

- Principal (P)

- The amount of money you actually borrow — the on-road price of the bike minus any down payment or trade-in value.

- Annual interest rate vs monthly rate

- Lenders quote an annual rate (for example, 10% per year). The EMI formula uses the monthly rate, found by dividing the annual rate by 12 (and by 100 to convert from a percentage), so \(r = \frac{\text{annual rate}}{1200}\).

- Tenure (n)

- The repayment period, expressed here in months. A 3-year loan has a tenure of 36 months.

- Reducing-balance method

- An interest-calculation method where interest is charged only on the outstanding principal, which falls with each EMI. The standard EMI formula assumes this method, so interest decreases over time while the principal portion grows.

- Total interest

- The sum of all interest paid over the full tenure — calculated as total payment minus the original principal.

- Down payment

- An upfront amount you pay from your own funds toward the bike's price. A larger down payment reduces the principal and therefore your EMI and total interest.

Understanding Your EMI Result

Your EMI is the equal amount you commit to pay each month for the entire tenure. Early in the loan, a larger share of each EMI goes toward interest; later, more goes toward repaying principal — even though the EMI itself stays constant.

The total interest figure is the extra cost of borrowing — what you pay above and beyond the amount you originally borrowed. The total payment is simply the principal plus that total interest, i.e. the full sum of all your EMIs.

A key trade-off to understand: choosing a longer tenure lowers your monthly EMI because the principal is spread over more installments, but it raises the total interest because you owe a balance for longer. A shorter tenure does the opposite — a higher monthly EMI but less interest overall. Use the scenario table above to weigh affordable monthly payments against total cost.

These figures reflect the loan principal, interest rate, and tenure only. They exclude processing or documentation fees, vehicle insurance, road tax, registration charges, and any GST or late-payment penalties. Your actual out-of-pocket cost and the amount disbursed by the lender may differ once those items are added, so treat the EMI result as the core repayment estimate rather than the complete cost of ownership.

FAQ

Does a higher down payment reduce my EMI? Yes. A larger down payment lowers the principal, which reduces both your EMI and total interest.

What does tenure mean? Tenure is the loan repayment period expressed in months in this tool.

Is processing fee included? No. The result covers principal and interest only; lender fees, insurance, and taxes are not included.