What Is the Debt Service Coverage Ratio?

The Debt Service Coverage Ratio (DSCR) measures how well an income-producing property or business can cover its debt obligations from its operating cash flow. Lenders use it heavily in commercial real estate and business lending to gauge repayment risk. A DSCR above 1.0 means there is more income than debt due; below 1.0 means cash flow is insufficient to fully cover the debt.

How to Use This Calculator

Enter your annual Net Operating Income (NOI) — gross revenue minus operating expenses, excluding debt payments and depreciation. Then enter your annual Total Debt Service — the sum of principal and interest payments on all loans for the year. The calculator instantly divides the two and labels the result Strong, Adequate, or Insufficient.

The Formula Explained

$$\text{DSCR} = \dfrac{\text{Net Operating Income}}{\text{Total Debt Service}}$$ If a property earns $120,000 NOI and owes $100,000 in annual debt service, the DSCR is \(120{,}000 \div 100{,}000 = 1.20\). That means the property generates 20% more income than needed to pay its debt.

Worked Example

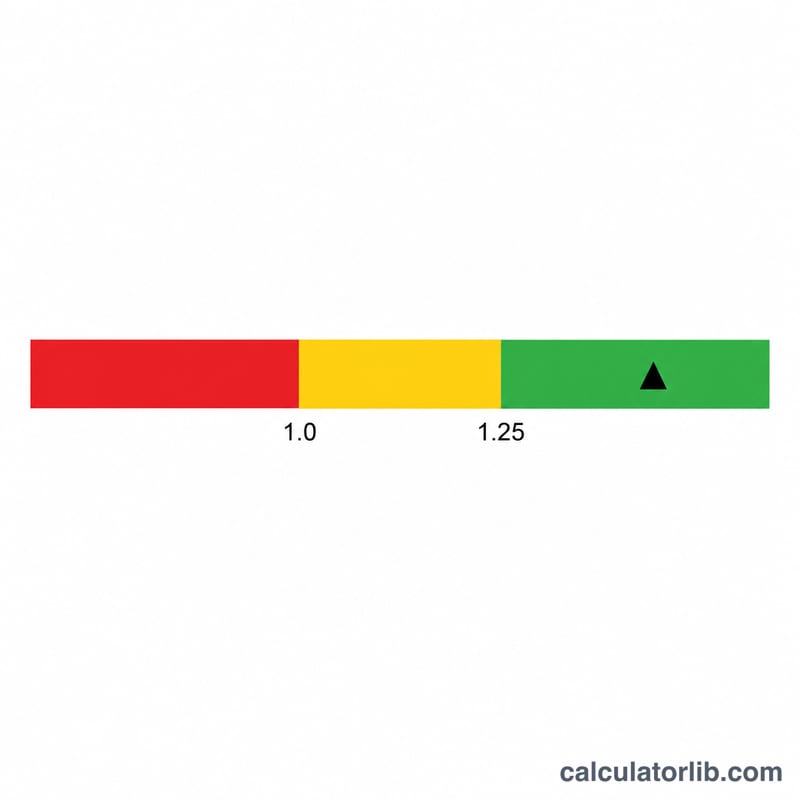

Suppose NOI is $150,000 and annual debt service is $100,000. $$\text{DSCR} = 150{,}000 \div 100{,}000 = 1.50$$ Many lenders require a minimum of 1.20–1.25, so a 1.50 ratio would generally be viewed favorably.

FAQ

What is a good DSCR? Lenders commonly want 1.25 or higher, though requirements vary by loan type and risk appetite.

What does a DSCR below 1.0 mean? The income does not fully cover debt payments, signaling a cash-flow shortfall and higher default risk.

Should NOI include debt payments? No. NOI is calculated before debt service and income taxes, so debt payments stay in the denominator only.