What is the Liquidity Coverage Ratio?

The Liquidity Coverage Ratio (LCR) is a Basel III regulatory metric that ensures banks hold enough unencumbered High Quality Liquid Assets (HQLA) to survive a 30-day period of significant liquidity stress. It is a globally adopted standard, supervised by national regulators (e.g. the Federal Reserve in the US, the PRA in the UK, the EBA in the EU). The minimum requirement is 100%.

How to use this calculator

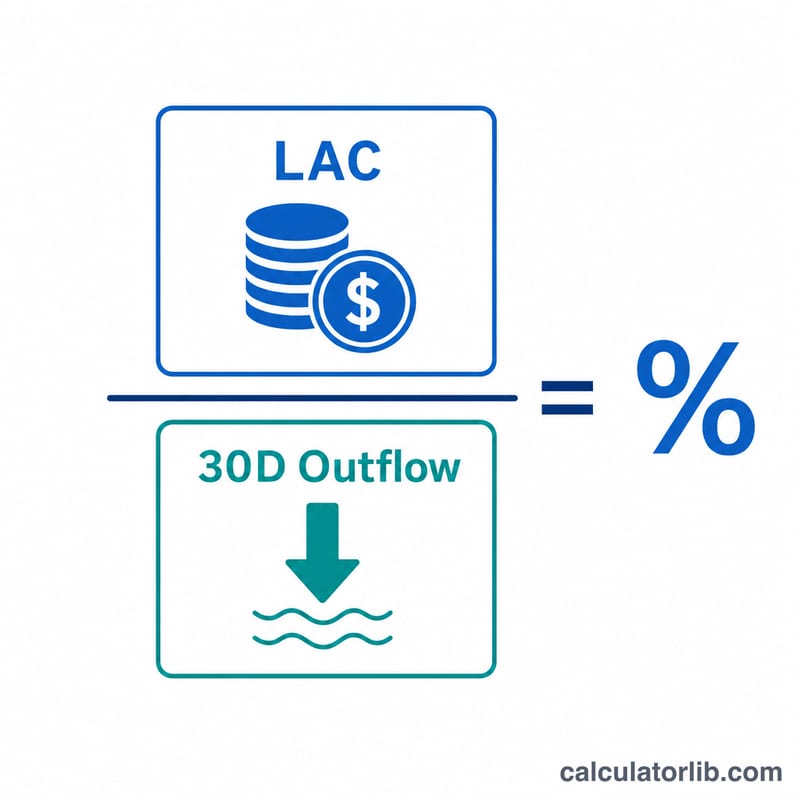

Enter the total value of your High Quality Liquid Assets (such as cash, central bank reserves, and high-grade government bonds) and your projected Total Net Cash Outflows over the next 30 calendar days under a stress scenario. The calculator returns the LCR as a percentage and tells you whether it meets the 100% regulatory minimum.

The formula explained

$$\text{LCR} = \frac{\text{HQLA}}{\text{Total Net Cash Outflows over 30 days}} \times 100$$ HQLA is the numerator; the stock of liquid assets that can be converted to cash quickly with little or no loss of value. The denominator is total expected cash outflows minus total expected cash inflows (capped at 75% of outflows) over the 30-day stress window. A ratio of 100% or higher indicates the bank can fully cover its net outflows.

Worked example

A bank holds $150,000 in HQLA and projects $120,000 in net cash outflows over 30 days. $$\text{LCR} = \frac{150{,}000}{120{,}000} \times 100 = 125\%$$ Because \(125\% \geq 100\%\), the bank is compliant with the minimum requirement and has a comfortable liquidity buffer.

FAQ

What counts as HQLA? Level 1 assets (cash, reserves, qualifying sovereign debt) and Level 2 assets (certain corporate and covered bonds, subject to haircuts and caps).

What is the minimum LCR? 100% under fully phased-in Basel III rules. Regulators may require higher buffers for specific institutions.

Is a higher LCR always better? A high LCR signals strong liquidity, but an excessively high ratio can mean a bank is holding too many low-yielding liquid assets instead of deploying capital profitably.