What Is the Goodwill Calculator?

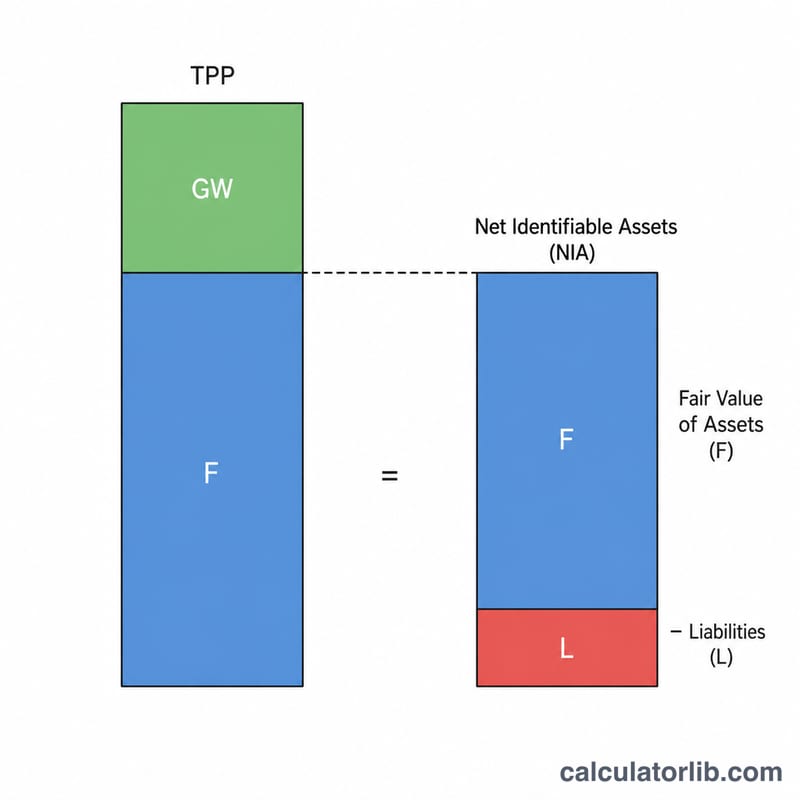

When one company acquires another, it rarely pays exactly the net book value of the target's assets. The premium paid above the fair value of the acquired business's net identifiable assets is recorded as goodwill — an intangible asset representing reputation, customer relationships, brand strength, and expected synergies. This calculator computes goodwill using the standard acquisition-method formula used under both IFRS 3 and US GAAP (ASC 805).

How to Use It

Enter three figures from the acquisition: the purchase price (total consideration transferred), the fair value of identifiable assets acquired, and the liabilities assumed as part of the deal. The calculator first works out net identifiable assets (assets minus liabilities), then subtracts that from the purchase price to reveal goodwill.

The Formula Explained

$$\text{Goodwill} = \text{Purchase Price} - \left(\text{Fair Value of Assets} - \text{Liabilities Assumed}\right)$$ The term in brackets is the net identifiable assets. If the purchase price exceeds this net amount, the difference is positive goodwill. A negative result indicates a "bargain purchase" (negative goodwill), which is typically recognized immediately as a gain.

Worked Example

Suppose Company A buys Company B for \(\$1{,}000{,}000\). B's identifiable assets have a fair value of \(\$900{,}000\) and A assumes \(\$200{,}000\) of liabilities. Net identifiable assets:$$\$900{,}000 - \$200{,}000 = \$700{,}000$$ Goodwill:$$\$1{,}000{,}000 - \$700{,}000 = \mathbf{\$300{,}000}$$

FAQ

What if the result is negative? A negative figure is a bargain purchase. Accounting standards generally require recognizing the gain in profit or loss rather than booking negative goodwill.

Should I use book value or fair value of assets? Always use fair value at the acquisition date, not historical book value, for an accurate goodwill figure.

Is goodwill amortized? Under IFRS and US GAAP for public companies, goodwill is not amortized but tested annually for impairment. Some jurisdictions allow private-company amortization.