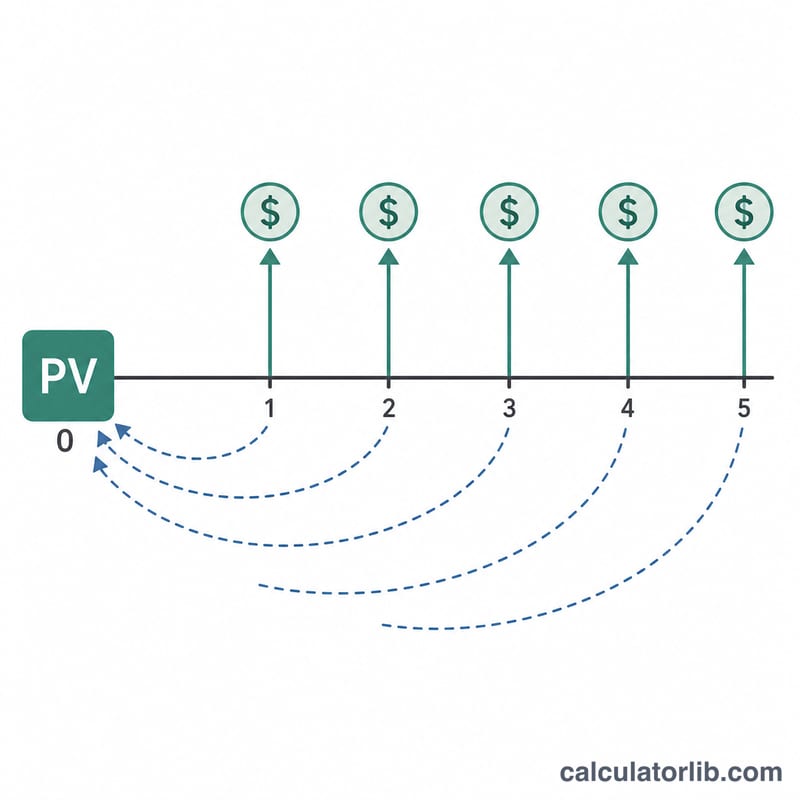

What Is the PVIFA?

The Present Value Interest Factor of an Annuity (PVIFA) is a multiplier that converts a series of equal future payments into a single present value. It answers the question: what is one dollar received every period for n periods worth today, given a discount rate r per period? Multiplying the PVIFA by your periodic payment instantly gives the present value of an ordinary annuity, which is why it appears in loan, lease, and bond calculations.

How to Use This Calculator

Enter the interest (discount) rate per period as a percentage and the total number of periods. The rate must match the payment frequency — use a monthly rate for monthly payments and an annual rate for yearly payments. The calculator returns the PVIFA factor; multiply it by your payment amount to find the present value of the whole stream.

The Formula Explained

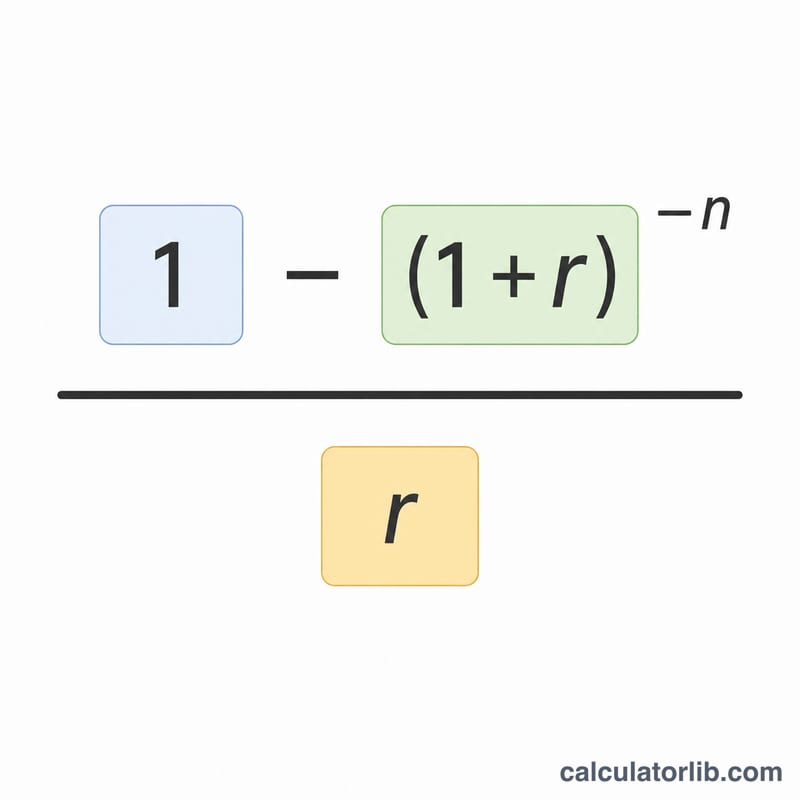

$$\text{PVIFA} = \frac{1 - \left(1 + r\right)^{-n}}{r}$$ Each future payment is discounted by \((1 + r)\) raised to the number of periods until it is received, and the geometric series of those discount factors collapses into this compact closed form. When \(r\) is 0, there is no discounting, so the factor simply equals \(n\).

Worked Example

Suppose \(r = 5\%\) per year and \(n = 10\) years. Then \((1.05)^{-10} \approx 0.613913\), so $$1 - 0.613913 = 0.386087$$ divided by \(0.05\) gives a PVIFA of about \(7.7217\). A $1,000 annual payment is therefore worth roughly $7,721.73 today.

FAQ

Is this for an ordinary annuity or annuity due? This factor assumes an ordinary annuity (payments at the end of each period). For an annuity due, multiply the result by \((1 + r)\).

What rate should I enter? Use the rate per period. For a 6% annual rate paid monthly, enter 0.5 (6 ÷ 12).

What happens at a 0% rate? With no discounting the PVIFA equals the number of periods, \(n\).