What Is the Sortino Ratio?

The Sortino ratio is a measure of risk-adjusted return that improves on the Sharpe ratio by penalizing only harmful volatility. Instead of using total standard deviation, it divides the excess return by the downside deviation — the volatility of returns that fall below a target (usually zero or the risk-free rate). This rewards investments that limit losses rather than punishing them for upside swings.

How to Use This Calculator

Enter three values: your portfolio's return, the risk-free rate (such as a Treasury yield), and the downside deviation of your returns — all as percentages. The calculator subtracts the risk-free rate from the portfolio return to get the excess return, then divides by the downside deviation to produce the Sortino ratio.

The Formula Explained

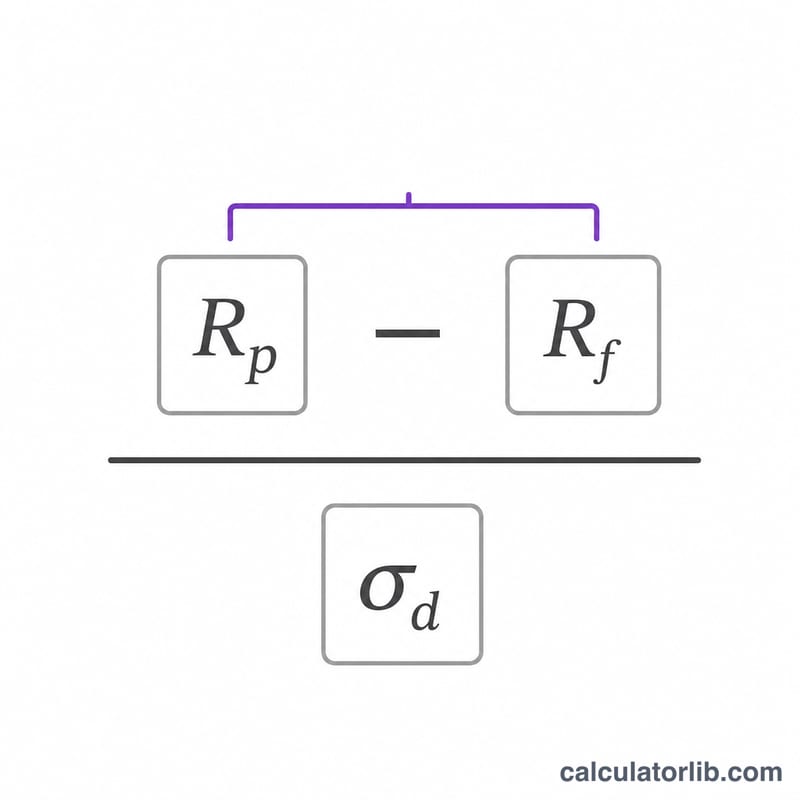

$$\text{Sortino} = \frac{R_p - R_f}{\sigma_d}$$ where \(R_p\) is portfolio return, \(R_f\) is the risk-free rate, and \(\sigma_d\) is the downside deviation. A higher ratio indicates better return per unit of downside risk. Generally a Sortino above 1 is acceptable, above 2 is very good, and above 3 is excellent.

Worked Example

Suppose a portfolio returns 12%, the risk-free rate is 2%, and the downside deviation is 5%. The excess return is \(12\% - 2\% = 10\%\). Dividing by 5% gives a Sortino ratio of $$\frac{10}{5} = 2.0$$ — a strong risk-adjusted result.

FAQ

How is the Sortino ratio different from the Sharpe ratio? The Sharpe ratio uses total standard deviation (both up and down moves), while the Sortino ratio uses only downside deviation, so it ignores beneficial volatility.

What is downside deviation? It is the standard deviation of returns that fall below a minimum acceptable return (MAR), often the risk-free rate or zero. You must compute it from your return series before using this calculator.

What is a good Sortino ratio? Above 1 is considered acceptable, above 2 is good, and above 3 is excellent, though benchmarks vary by asset class and strategy.