What this calculator does

Buying a home is rarely cheaper or pricier than renting on its own — it depends on your time horizon, the mortgage, taxes, upkeep and how the market moves. This Rent or Buy Calculator estimates the net cost of each path over the number of years you plan to stay, so you can compare apples to apples.

How to use it

Enter the home price, down payment, mortgage rate and term, and how many years you expect to live there. Add property tax and maintenance as a percentage of the home price per year, plus your monthly rent and how fast rent rises. The tool returns the net cost of buying, the total cost of renting, your monthly payment, the equity you build, and the gain from appreciation.

The formula explained

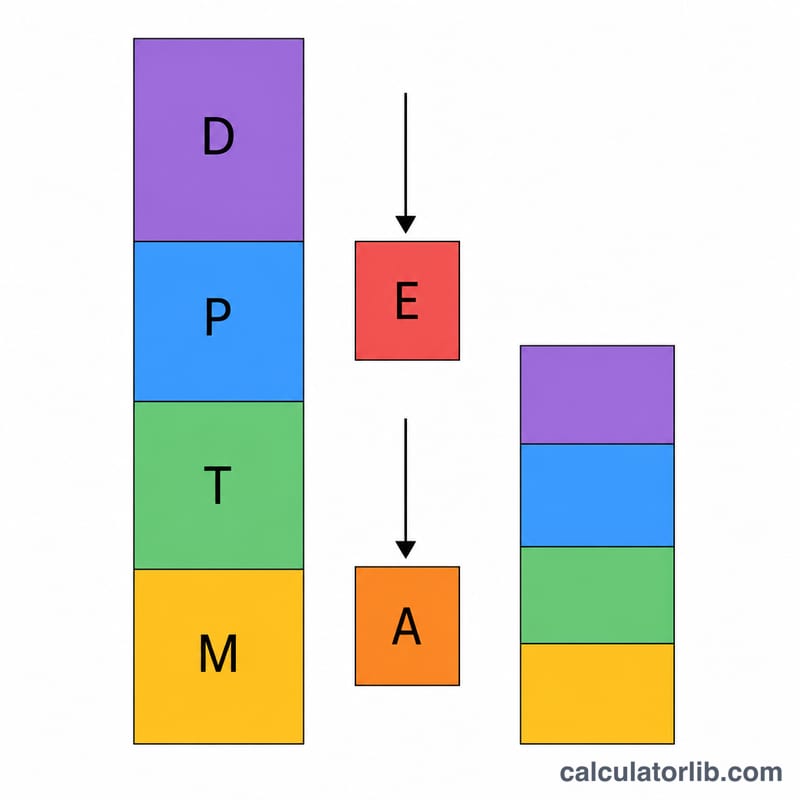

The net cost of buying adds the down payment, the mortgage payments you make while you live there, property taxes and maintenance, then subtracts the equity you accumulate (down payment plus principal paid down) and the home's appreciation gain. Rent cost simply totals twelve months of rent each year, growing rent annually. Appreciation gain here uses a simple linear estimate: price × appreciation rate × years.

$$\text{BuyCost} = D + P\cdot n + T + M - E - A$$

$$\text{Buy} = D + (\text{pmt}\cdot n) + T + M - E - A$$

$$\text{Rent} = \sum_{y=0}^{Y-1} 12\,r\,(1+g)^y$$

Worked example

A $400,000 home with 20% down ($80,000), a 6.5% 30-year mortgage, held 7 years, 3% appreciation, 1.1% tax and 1% maintenance, versus $2,000/mo rent growing 3%. Appreciation gain = $$400{,}000 \times 0.03 \times 7 = 84{,}000$$ $84,000. The calculator nets everything to show which option costs less over those 7 years.

FAQ

Does this include investment of the down payment? No — it focuses on direct housing cash flows and equity, not opportunity cost on invested savings.

Are closing or selling costs included? Not by default; add them mentally to the buy side for a stricter comparison.

Why does a longer stay favor buying? Equity and appreciation accumulate over time, lowering the net cost of owning the longer you stay.