What Is the 28% Rule?

The 28% rule is a widely used guideline for housing affordability. It suggests that your total monthly housing cost — mortgage payment (or rent), property taxes, and insurance — should not exceed 28% of your gross monthly income. Staying within this limit helps keep your budget balanced and leaves room for other expenses, savings, and unexpected costs.

How to Use This Calculator

Enter your annual gross salary (before taxes and deductions) and a housing ratio. The default ratio is 28%, the traditional lender benchmark, but you can lower it for a more conservative budget or raise it if you want to test a stretch scenario. The calculator instantly shows your maximum monthly housing cost, your gross monthly income, and the equivalent annual housing limit.

The Formula Explained

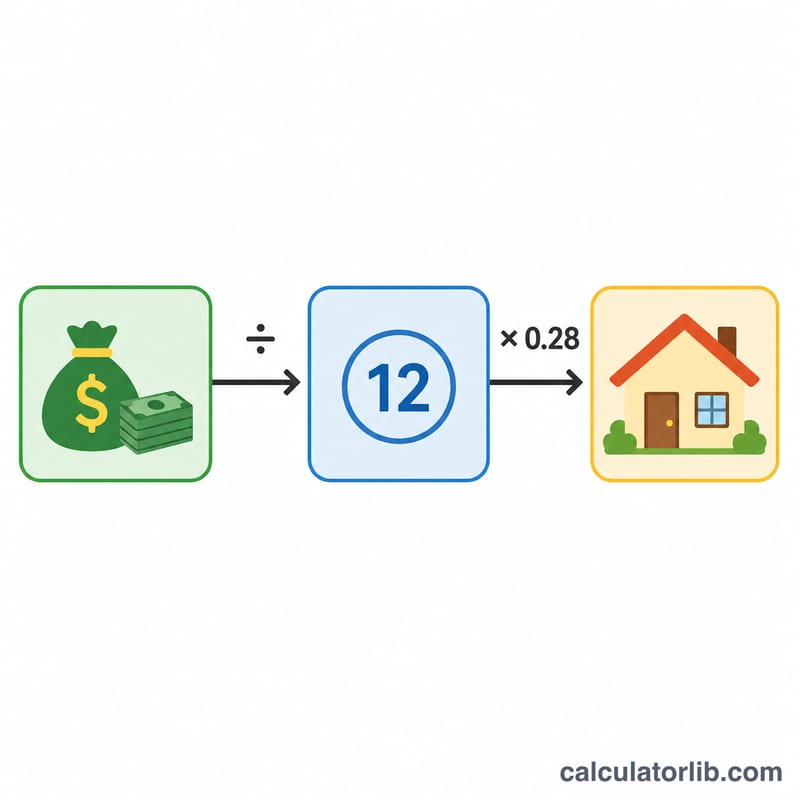

The math is straightforward. First we convert annual salary to monthly income by dividing by 12. Then we multiply by the housing ratio expressed as a decimal:

$$\text{Max Monthly Housing} = \frac{\text{Annual Salary}}{12} \times \frac{\text{Ratio (\%)}}{100}$$

With the standard 28% rule, the ratio decimal is \(0.28\).

Worked Example

Suppose you earn $60,000 per year. Your gross monthly income is $$60{,}000 \div 12 = \$5{,}000.$$ Applying the 28% rule: $$5{,}000 \times 0.28 = \$1{,}400 \text{ per month}.$$ Over a year that totals $16,800 in housing costs. If you preferred a more cautious 25% ratio, your monthly limit would drop to $1,250.

FAQ

Is gross or net salary used? The 28% rule traditionally uses gross (pre-tax) income, which is what lenders evaluate.

What does the housing cost include? Typically the full PITI payment: principal, interest, property taxes, and homeowner's insurance — or your rent if renting.

Is the 28% rule a hard limit? No, it's a guideline. Many lenders also apply a 36% rule for total debt. Your ideal ratio depends on your other obligations and goals.