What this calculator does

Jurisdiction: United States. This tool estimates US federal individual income tax owed on a given amount of taxable income using the IRS progressive marginal rate schedules for the tax year and filing status you choose (2019 through 2026). It reports your estimated tax, your top marginal bracket, your effective tax rate, and your net income after tax. Non-US readers: this models US federal income tax only and has no equivalent elsewhere.

Important: taxable income only

You must enter income after deductions and exemptions. This calculator does NOT apply the standard deduction, itemized deductions, tax credits, the Alternative Minimum Tax (AMT), the Net Investment Income Tax, self-employment tax, FICA (Social Security/Medicare), or any state or local tax. It is a clean estimate of tax on the taxable base only.

How to use it

1) Pick the tax year. 2) Pick your filing status (Single, Married Filing Jointly, Married Filing Separately, or Head of Household). 3) Enter your taxable income in dollars. Press calculate to see the breakdown.

The formula explained

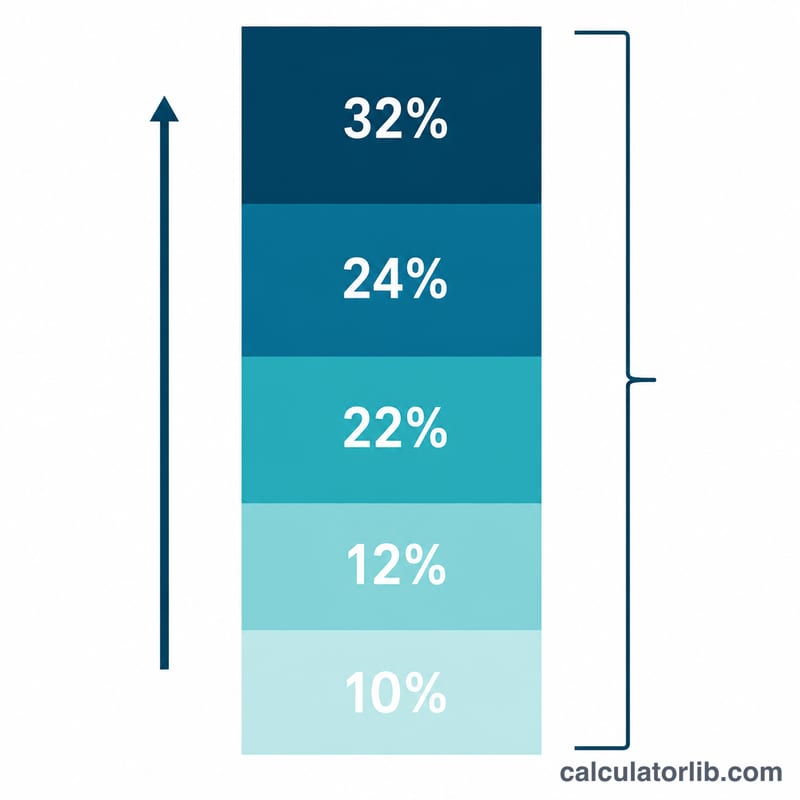

The US uses a progressive system: income is sliced into brackets, and each slice is taxed at that bracket's marginal rate. All four filing statuses share the same seven rates (10%, 12%, 22%, 24%, 32%, 35%, 37%); only the dollar thresholds differ by year and status. Your tax is the sum of (rate x portion of income falling inside each bracket). Bracket boundaries are lower-inclusive and upper-exclusive, so income exactly at a threshold falls into the higher bracket.

$$\text{Tax} = \sum_r \text{rate}_r \times \big(\min(\text{income}, U_r) - L_r\big)$$

Worked example

Tax year 2026, Married Filing Jointly, taxable income $85,000. The 10% bracket covers [0, 24800): \(0.10 \times 24{,}800 = \$2{,}480\). The 12% bracket covers [24800, 100800), and your income stops at 85,000:

$$0.12 \times (85{,}000 - 24{,}800) = 0.12 \times 60{,}200 = \$7{,}224$$Total tax = \(2{,}480 + 7{,}224 = \) $9,704. Marginal bracket = 12.0%. Effective rate = \(9{,}704 / 85{,}000 \times 100 = 11.42\%\). Net income = \(85{,}000 - 9{,}704 = \$75{,}296\).

FAQ

Why is my marginal rate higher than my effective rate? The marginal rate applies only to your last dollar; lower brackets tax earlier dollars at lower rates, so your overall (effective) rate is always lower than your top bracket.

The effective rate is computed as $$\text{Effective Rate} = \frac{\text{Estimated Tax}}{\text{Taxable Income}} \times 100$$

Does this include the standard deduction? No. Enter income already reduced by your deduction. For 2026 the standard deduction is about $16,100 (Single) and $32,200 (Married Filing Jointly), but you subtract that yourself before entering taxable income.

How accurate is the 2026 table? The 2026 thresholds are the IRS inflation-adjusted figures from Revenue Procedure 2025-32; all years estimate federal income tax only.