What Is a 10/1 ARM?

A 10/1 ARM (adjustable-rate mortgage) is a US home loan that carries a fixed interest rate for the first 10 years, then adjusts once per year for the remaining term. This calculator estimates your fixed monthly payment during the introductory decade and the new payment after the first reset, assuming a single adjusted rate for the rest of the loan. Figures are estimates; actual ARMs use index + margin and rate caps that vary by lender.

How to Use It

Enter the loan amount, the initial fixed rate (in effect for the first 10 years), the rate you expect after the adjustment, and the total loan term (usually 30 years). The calculator returns the initial monthly principal-and-interest payment, the remaining balance after 10 years, and the recomputed payment for the rest of the loan.

The Formula Explained

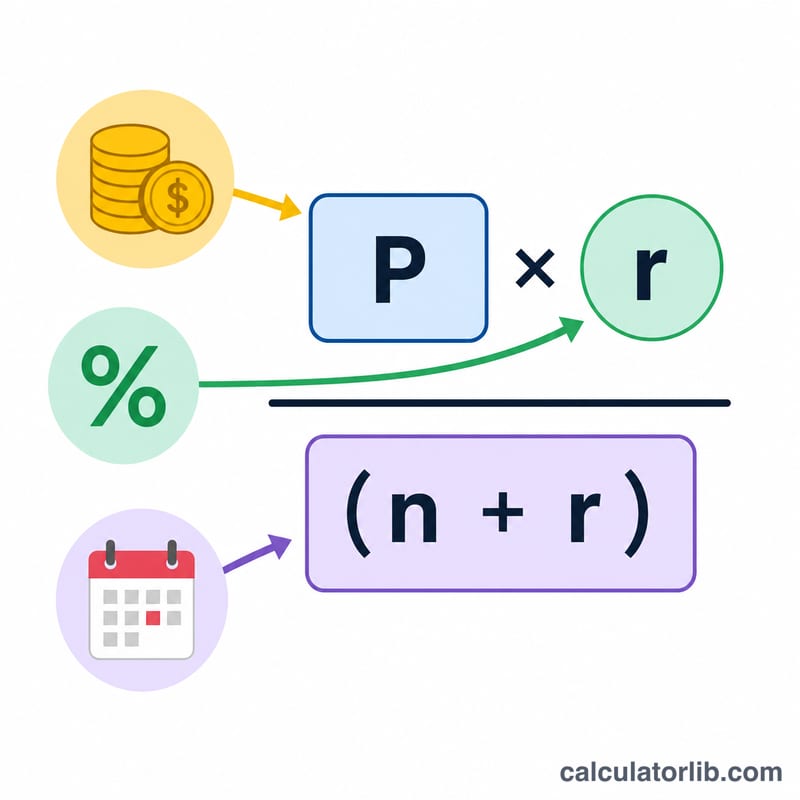

The standard amortization formula is used: $$\text{PMT} = \dfrac{P \cdot r}{1-(1+r)^{-n}}$$ where \(r\) is the monthly rate (annual \(\div\) 12) and \(n\) is the number of months. The initial payment amortizes the full balance over the entire term at the introductory rate. We then march the balance forward month by month for 120 payments, and re-amortize the leftover balance over the remaining months at the adjusted rate.

Worked Example

Loan $300,000, initial rate 5%, adjusted rate 7%, 30-year term. The initial payment is about $1,610.46/month. After 10 years roughly $244,026 remains. Re-amortized at 7% over 240 months, the new payment jumps to about $1,892.06 — an increase of about $281.60.

Definitions & Glossary

A 10/1 adjustable-rate mortgage (ARM) carries a fixed interest rate for the first 10 years, after which the rate can adjust once per year. The terms below describe the mechanics that govern how the rate and payment change.

- Index — A published, market-driven benchmark interest rate (for example SOFR or a Treasury-based rate) that the lender uses as the moving reference for adjustments. The lender cannot control the index.

- Margin — A fixed number of percentage points the lender adds to the index. The margin stays constant for the life of the loan and is set at origination.

- Fully-indexed rate — The sum of the current index value and the margin: \(\text{index} + \text{margin}\). This is the rate the loan moves toward at each adjustment, subject to caps.

- Periodic cap — A limit on how much the interest rate can change at a single adjustment (commonly 1–2 percentage points per year for a 10/1 ARM).

- Lifetime cap — A ceiling on how far the rate can rise above the initial rate over the entire life of the loan (commonly around 5 percentage points).

- Initial rate — The fixed interest rate charged during the first 10 years (the “10” in 10/1). It is often lower than a comparable fixed-rate mortgage.

- Adjusted rate — The interest rate that applies after the fixed period ends and adjustments begin; in real loans it is reset periodically to the fully-indexed rate within the caps.

- Re-amortization — Recalculating the monthly payment so the remaining balance is paid off over the remaining term at the new interest rate. The payment after adjustment is based on the balance left after 10 years, not the original loan amount.

- Principal-and-interest (P&I) payment — The monthly amount that covers both interest charges and repayment of principal. It excludes taxes, insurance and other escrow items.

- Amortization — The process of gradually paying off a loan through scheduled equal payments, where early payments are mostly interest and later payments are mostly principal.

Interpreting Your Result

This calculator reports two figures: the fixed payment for years 1–10 and a recomputed payment for the period after the rate adjusts. The difference between them shows how sensitive your budget is to a rate change at the end of the fixed period.

The adjusted payment is not simply the initial payment scaled by the new rate. After 10 years you have already paid down part of the principal, so the new payment is calculated by re-amortizing the remaining balance over the remaining term at the adjusted rate. A higher remaining balance or a higher rate increases the payment; the shorter remaining term works in the opposite direction.

Real ARMs differ from this model in two important ways:

- Caps limit movement. Actual loans apply a periodic cap (how much the rate can move at one adjustment) and a lifetime cap (the maximum rate over the life of the loan). The fully-indexed rate may be high, but caps can prevent the rate from reaching it immediately.

- The rate is set by index + margin and can change every year. After the fixed period a 10/1 ARM resets annually, so the rate — and the payment — can move up or down each year based on the current index plus the fixed margin.

This tool assumes a single flat adjusted rate held for the entire remaining term, rather than a series of annual resets. Treat the adjusted-payment figure as a what-if estimate for one rate scenario, useful for stress-testing your budget across several possible rates rather than as a forecast of your exact future payment. This is general information, not personalized financial advice; consult your lender's loan documents for your specific caps, index, and margin.

FAQ

Does the payment always go up? No. If the adjusted rate is lower than the initial rate, the payment can fall.

Are rate caps included? No — this is a simplified single-adjusted-rate model. Real ARMs cap how much the rate can move per period and over the life of the loan.

Is this only for the US? The 10/1 ARM structure is primarily a US mortgage product, but the underlying amortization math is universal.