What Is the Advanced Loan Calculator?

This calculator works out the fixed monthly payment for any fully amortizing loan — a mortgage, auto loan, personal loan, or student loan. Enter how much you are borrowing, the annual interest rate, and the repayment term, and it returns the monthly payment, the total amount you will repay, and the total interest cost over the life of the loan.

How to Use It

Type the loan amount (the principal), the annual interest rate as a percentage (e.g. 6 for 6%), and the term in years. The tool converts the term to months and the annual rate to a monthly rate, then applies the standard amortization formula. Results update instantly so you can compare different terms or rates.

The Formula Explained

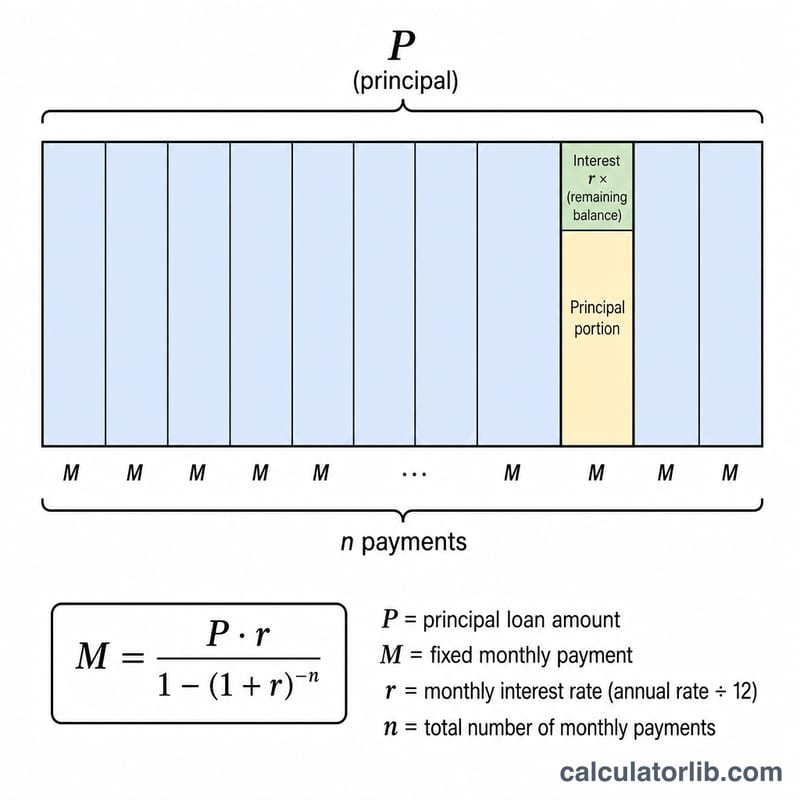

The monthly payment is given by $$M = P \cdot \frac{r(1+r)^n}{(1+r)^n - 1}$$ where \(P\) is the principal, \(r\) is the monthly interest rate (the annual rate divided by 12), and \(n\) is the total number of monthly payments (years × 12). When the interest rate is 0%, the payment is simply the principal divided by the number of months. Total interest equals the monthly payment times the number of payments, minus the principal.

Worked Example

Borrow $200,000 at 6% annual interest over 30 years. The monthly rate is \(0.06 / 12 = 0.005\) and \(n = 360\). Then \((1.005)^{360} \approx 6.02258\), so $$M = 200{,}000 \times \frac{0.005 \times 6.02258}{6.02258 - 1} \approx \$1{,}199.10$$ per month. Over 360 payments you repay about $431,676, of which roughly $231,676 is interest.

Key Loan Terms Defined

- Principal (P)

- The original amount borrowed, before any interest is added. In the formula this is the starting balance the payments must repay.

- Annual interest rate vs. monthly rate (r)

- The annual rate is the yearly cost of borrowing quoted as a percentage (e.g. 6%). The monthly rate used in the payment formula is that figure divided by 12 and converted from percent: \( r = \dfrac{\text{Annual Rate}}{1200} \). For 6% this is \( 6/1200 = 0.005 \) per month.

- Term

- The length of the loan, here entered in years. It determines how long you make payments.

- Number of payments (n)

- The total count of monthly payments over the life of the loan: \( n = 12 \times \text{Term in years} \). A 30-year loan has \( n = 360 \) payments.

- Amortization

- The process of paying off a loan in equal periodic payments, where each payment covers the interest due that period plus a portion of the principal, gradually reducing the balance to zero.

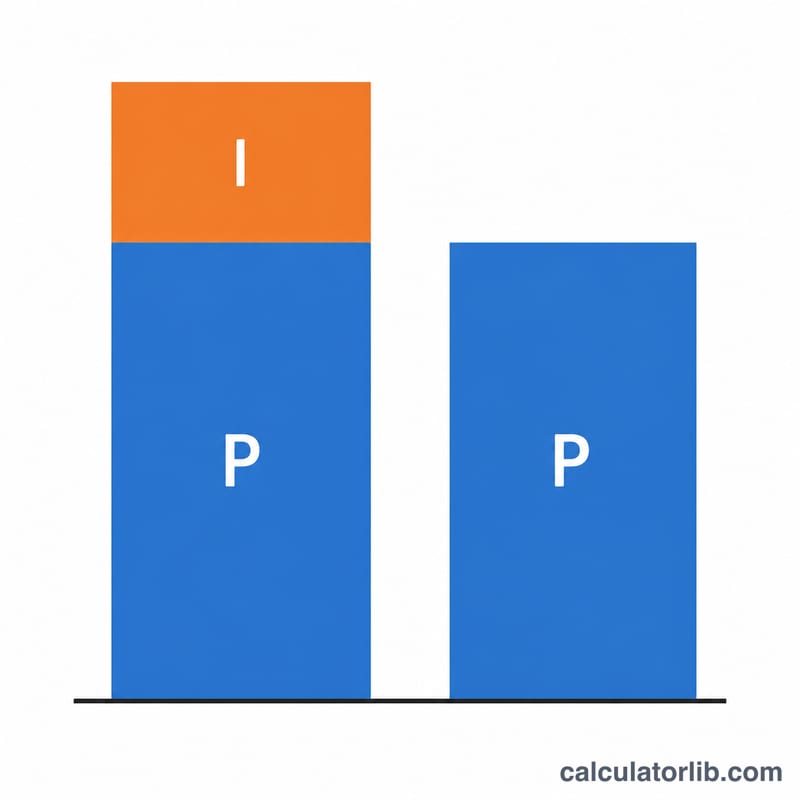

- Total interest

- The sum of all interest charges over the life of the loan, equal to total payments minus the original principal: \( (M \times n) - P \).

- Total cost

- Everything you pay back over the full term: \( M \times n \), i.e. principal plus total interest.

Understanding Your Results

The monthly payment (M) is the fixed amount you owe each month for a fully amortizing loan. It is sized so that, after the final payment, the balance reaches exactly zero. Because it is fixed, it lets you budget predictably regardless of how the split between interest and principal changes over time.

The total interest is the extra you pay above the amount borrowed — the lender's compensation for the loan. The total cost is the sum of principal and total interest, representing the complete out-of-pocket amount over the term.

Within an amortizing loan, interest dominates the early payments. Interest each month is charged on the outstanding balance, which is largest at the start, so a big share of your early payments goes to interest and only a small share reduces principal. As the balance falls, the interest portion shrinks and more of each payment chips away at principal — the split tilts steadily toward principal as the loan matures.

Choosing a longer term lowers the monthly payment because the principal is spread over more payments, but it raises the total interest because you carry a balance longer and accrue interest for more months. A shorter term does the opposite: a higher monthly payment but far less interest overall. Comparing the total-cost figures across terms makes this trade-off concrete.

This is general educational information about how loan math works, not personalized financial advice. Actual loan offers may include fees, compounding conventions, or insurance that change the numbers; consult the lender's disclosures and a qualified professional for decisions specific to your situation.

FAQ

Does this include taxes or insurance? No. It shows only principal and interest. For a mortgage, add escrow amounts separately.

What if my rate is 0%? The calculator handles a 0% rate by dividing the principal evenly across the months.

Can I use it for any currency? Yes — the math is currency-agnostic; just enter your amounts in whatever currency you use.