What Is Days Sales Outstanding (DSO)?

Days Sales Outstanding (DSO) measures the average number of days a company takes to collect cash after making a credit sale. It is a key liquidity and accounts-receivable efficiency metric used by finance teams worldwide. A lower DSO means customers pay quickly and cash flow is healthy; a higher DSO can signal collection problems or overly generous credit terms.

How to Use This Calculator

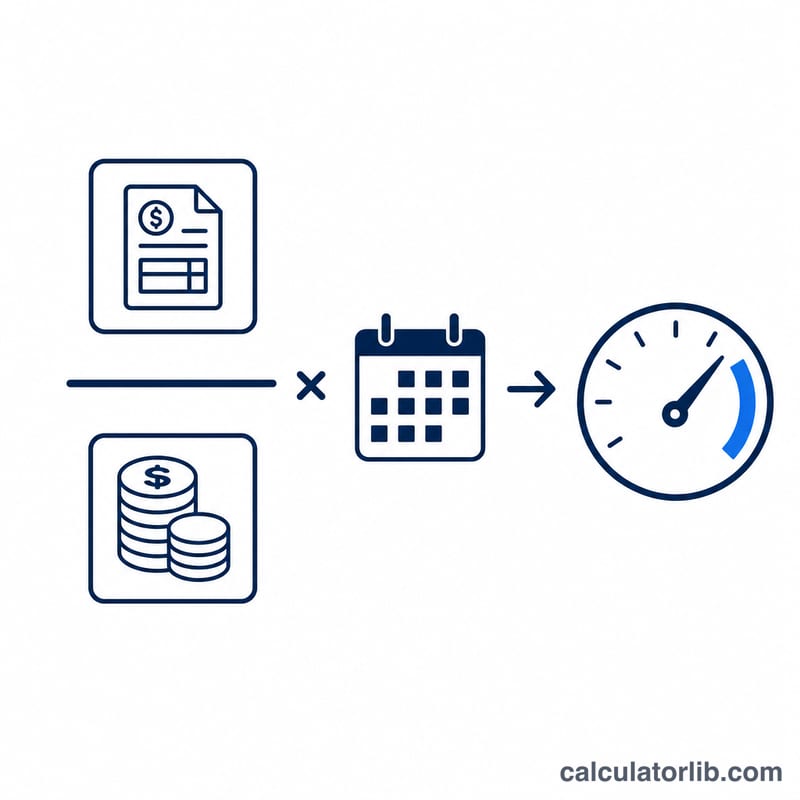

Enter your Accounts Receivable (the outstanding amount customers owe), your Total Revenue for the period (ideally net credit sales), and the number of days in that period. Use 365 for a full year, 90 for a quarter, or 30 for a month. The calculator returns your DSO in days plus the receivables turnover ratio.

The Formula Explained

The standard formula is $$\text{DSO} = \frac{\text{Accounts Receivable}}{\text{Net Credit Sales}} \times \text{Days in Period}$$ The ratio of receivables to revenue represents the fraction of sales still uncollected; multiplying by the number of days in the period scales it into a day count. Receivables turnover is calculated as Days ÷ DSO.

Worked Example

Suppose a company has $50,000 in accounts receivable and $500,000 in annual revenue. $$\text{DSO} = \left( \frac{50{,}000}{500{,}000} \right) \times 365 = 0.10 \times 365 = \textbf{36.5 days}$$ This means it takes roughly 37 days on average to collect payment. The receivables turnover is \(365 \div 36.5 = 10\) times per year.

FAQ

What is a good DSO? It varies by industry, but a DSO under 45 days is generally considered healthy. Compare against your payment terms — if you offer net-30, a DSO near 30 is ideal.

Should I use total revenue or credit sales? Strictly, DSO should use net credit sales, since cash sales are collected immediately. If credit-only figures aren't available, total revenue is a common approximation.

Why does the period length matter? DSO is always tied to a time window. Using 365 gives an annualized figure; using 90 measures a single quarter, which can reveal seasonal collection patterns.