What Is Portfolio Expected Return?

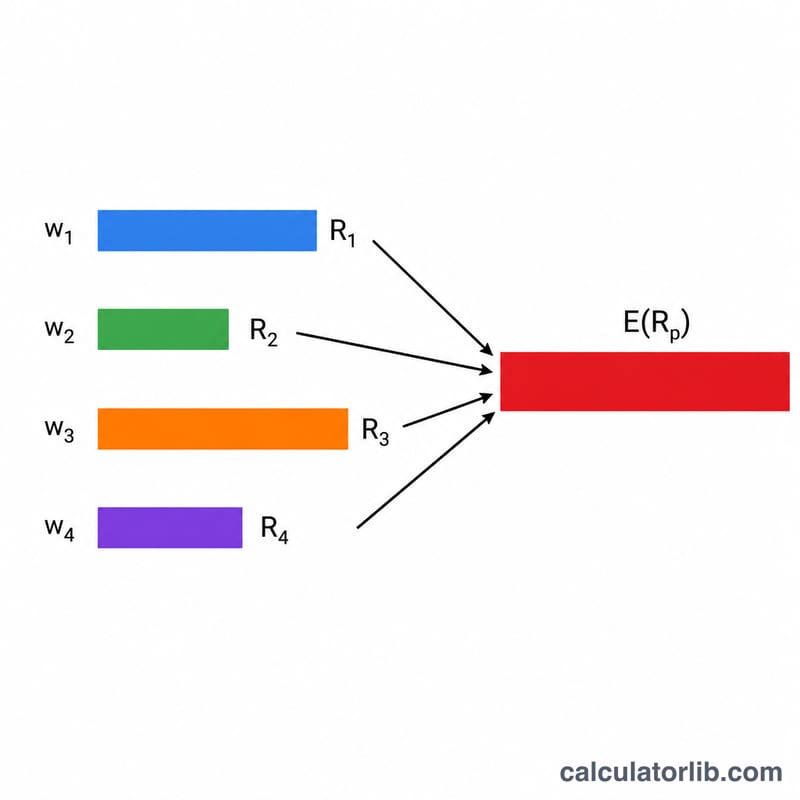

The expected return of a portfolio, written \(E(R_p)\), is the anticipated weighted-average return of all the assets it holds. Each asset contributes in proportion to how much of the portfolio it represents. It is one of the most fundamental concepts in modern portfolio theory and is used by investors to forecast performance and compare allocation choices before committing capital.

How to Use This Calculator

Enter the portfolio weight (as a percentage) and the expected return (as a percentage) for each asset you hold — up to four. Weights should ideally sum to 100%, but if they do not, the calculator automatically normalizes by dividing the weighted total by the sum of your weights, so you always get a meaningful weighted average. Leave unused asset rows at 0.

The Formula Explained

The core equation is

$$E(R_p) = \sum w_i \times E(R_i)$$where \(w_i\) is the weight of asset i and \(E(R_i)\) is its expected return. You multiply each asset's weight by its expected return, then add all the products together. If weights are expressed as percentages that sum to 100, the result is read directly as a percent return.

Worked Example

Suppose you hold 60% in stocks expected to return 8% and 40% in bonds expected to return 4%. The calculation is

$$(0.60 \times 8) + (0.40 \times 4) = 4.8 + 1.6 = 6.4\%$$The portfolio is expected to return 6.4% per period — higher than bonds alone but lower than stocks, reflecting the blend.

FAQ

Do my weights have to add up to 100%? Ideally yes, but this tool normalizes automatically so even if they sum to, say, 90%, it still returns a correct weighted average.

Does this account for risk? No — expected return ignores volatility and correlation. For risk you would also compute portfolio standard deviation.

Is expected return guaranteed? No. It is a probability-weighted estimate; actual returns will vary around it.