What Is Portfolio Beta?

Beta measures how sensitive an investment is to movements in the overall market. A beta of 1.0 means the asset tends to move in line with the market; a beta above 1.0 means it is more volatile, while a beta below 1.0 means it is less volatile. Portfolio beta aggregates the betas of all your holdings into a single number that describes the systematic risk of your entire portfolio.

How to Use This Calculator

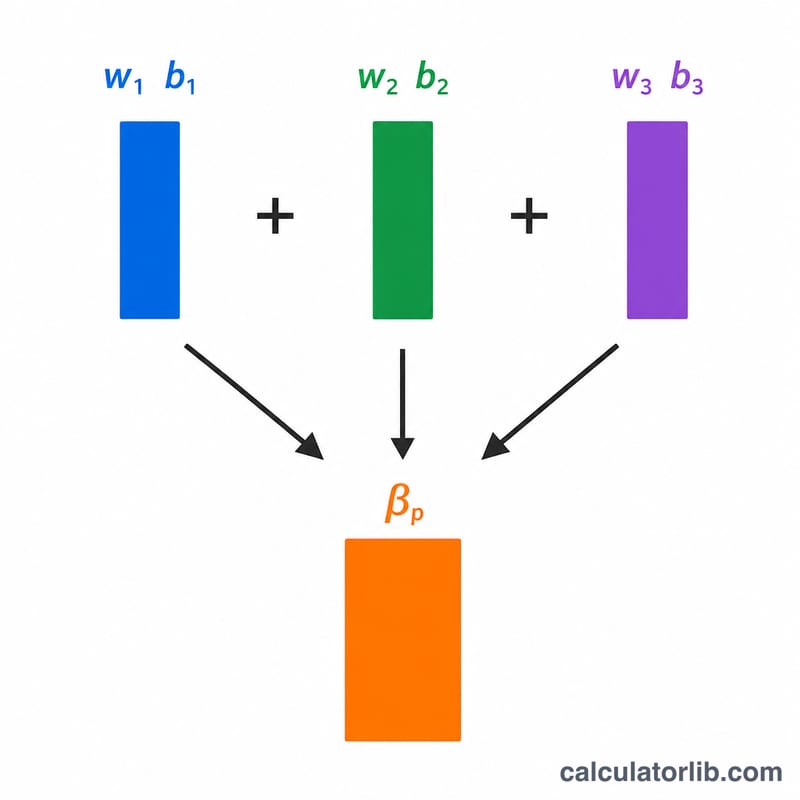

Enter the current dollar value and the beta of each holding (up to four). Leave any rows you do not need blank. The calculator computes each holding's weight as its value divided by the total portfolio value, multiplies each weight by its beta, and sums the results to produce the portfolio beta.

The Formula Explained

Portfolio beta is a value-weighted average:

$$\beta_p = \sum (w_i \times \beta_i)$$ where \(w_i = V_i / \sum V\).

Because the weights add up to 1, the portfolio beta is simply the weighted mean of the individual betas. Bigger positions influence the result more than smaller ones.

Worked Example

Suppose you hold $10,000 of a stock with beta 1.2 and $15,000 of a stock with beta 0.8. Total value is $25,000. Weighted beta = $$(10{,}000 \times 1.2) + (15{,}000 \times 0.8) = 12{,}000 + 12{,}000 = 24{,}000.$$ Divide by 25,000 to get a portfolio beta of 0.96 — slightly less volatile than the market.

FAQ

What does a beta of 1.5 mean? The portfolio is expected to move about 1.5% for every 1% move in the market, making it 50% more volatile.

Can portfolio beta be negative? Yes, if you hold assets that move opposite to the market (such as some inverse funds or certain commodities).

Does beta capture all risk? No. Beta only measures systematic (market) risk, not company-specific or idiosyncratic risk that can be reduced through diversification.