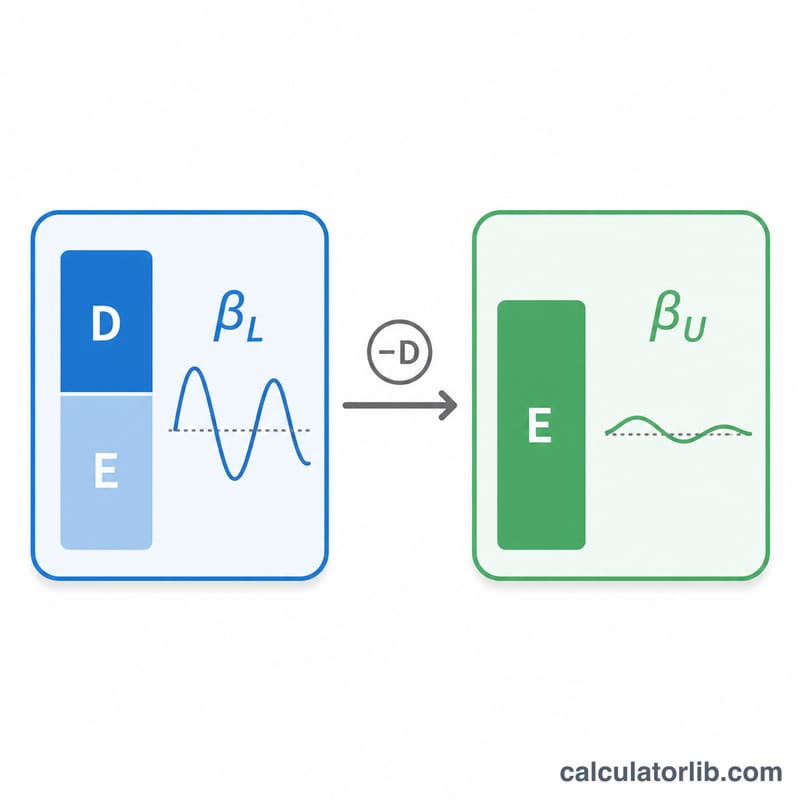

What Is Unlevered Beta?

Unlevered beta (also called asset beta) measures the systematic risk of a company's assets without the influence of debt. While a stock's observed levered beta reflects both business risk and financial risk from borrowing, unlevered beta strips out the leverage effect so you can compare the underlying risk of firms with different capital structures. It is a core input when estimating the cost of equity using the CAPM, especially in the "pure-play" method of valuing private companies or new business segments.

How to Use This Calculator

Enter the company's levered (equity) beta, its marginal tax rate as a percentage, and its total debt and total equity (usually market values). The calculator computes the debt-to-equity ratio, applies the Hamada equation, and returns the unlevered beta along with the levering factor used in the denominator.

The Formula Explained

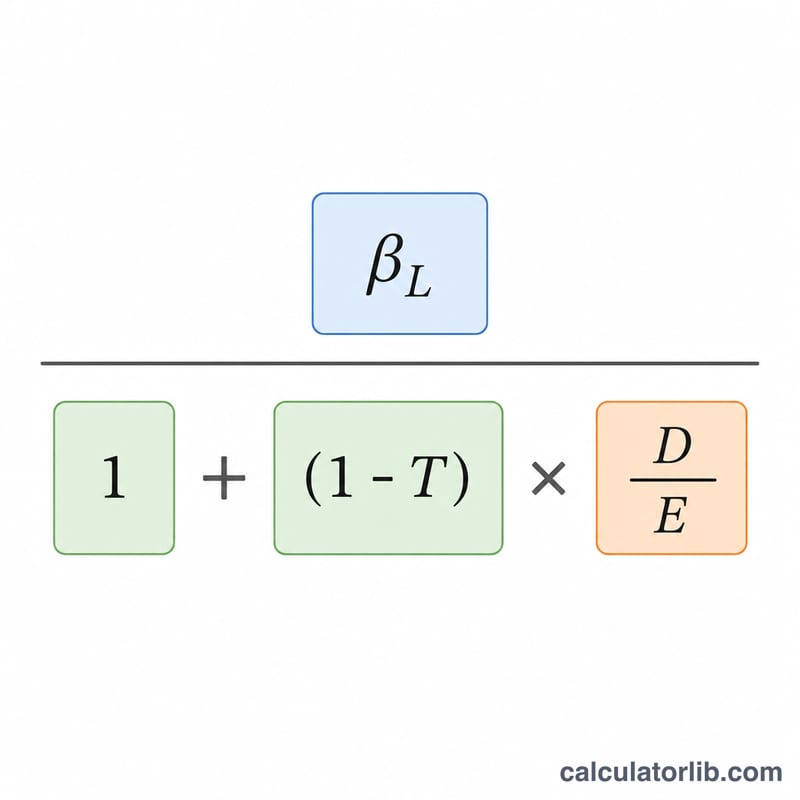

The relationship is given by the Hamada equation:

$$\beta_U = \frac{\text{Levered Beta}}{1 + \left(1 - \dfrac{\text{Tax Rate (\%)}}{100}\right)\dfrac{\text{Debt}}{\text{Equity}}}$$

Because interest on debt is tax-deductible, the term (1 − Tax Rate) reduces the impact of leverage. A higher debt-to-equity ratio increases the denominator, which lowers the unlevered beta relative to the levered beta — confirming that observed equity risk is partly driven by borrowing.

Worked Example

Suppose a firm has a levered beta of 1.2, a tax rate of 21%, debt of 400,000 and equity of 600,000. The debt-to-equity ratio is \(400{,}000 / 600{,}000 = 0.6667\). The denominator is $$1 + (1 - 0.21) \times 0.6667 = 1 + 0.79 \times 0.6667 = 1.5267.$$ The unlevered beta is \(1.2 / 1.5267 \approx 0.7860\).

FAQ

Why unlever a beta? To compare companies with different debt levels or to re-lever a comparable company's beta to your target's capital structure.

Should I use market or book values? Market values of debt and equity are preferred in valuation; book values are sometimes used when market data is unavailable.

Is unlevered beta always lower than levered beta? Yes, whenever the company carries debt the unlevered beta is lower, because removing leverage removes financial risk.