What This Calculator Does

This tool shows how much a loan will grow when interest compounds and no payments are made. Unlike an amortizing loan, where regular payments steadily reduce the balance, a no-payment loan lets interest pile on top of interest. This applies to scenarios like deferred student loans, certain bridge financing, or savings/investment growth viewed in reverse. The result is the total amount owed at the end of the term plus the interest portion.

How to Use It

Enter the original loan amount (principal), the annual interest rate as a percentage, the number of years the loan runs, and how often interest compounds (daily, monthly, quarterly, semi-annually, or annually). The calculator returns the total balance owed and the total compound interest accrued over the term.

The Formula Explained

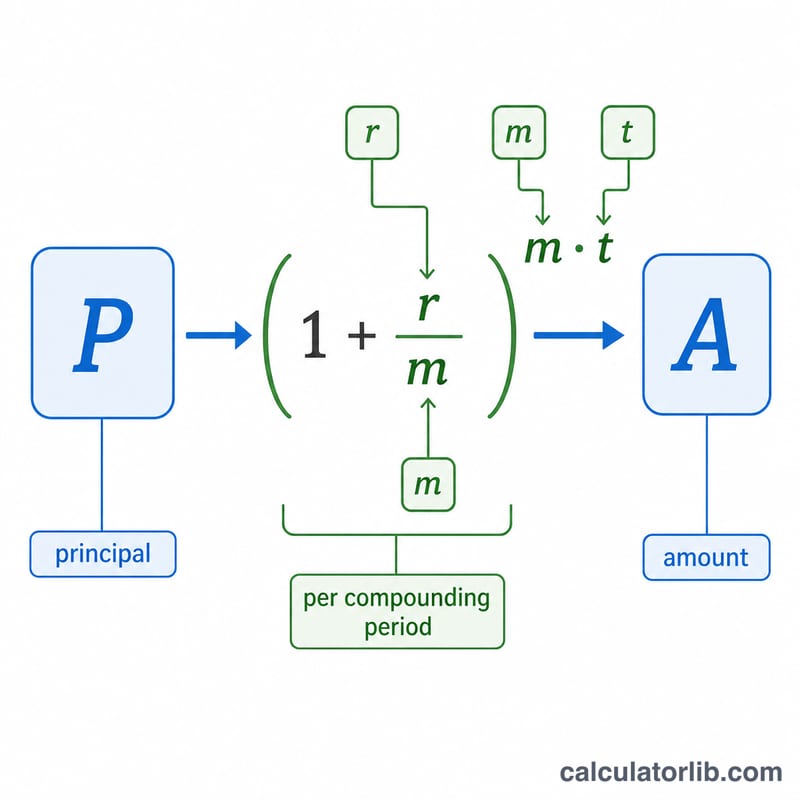

The future balance is given by $$A = P\left(1 + \frac{r}{m}\right)^{m\,t}$$ where P is the principal, r is the annual rate as a decimal, m is the number of compounding periods per year, and t is the time in years. Each period, interest of \(r/m\) is applied to the current balance, so the balance grows geometrically. More frequent compounding (larger \(m\)) produces a slightly higher final balance for the same nominal rate.

Worked Example

Suppose you borrow $10,000 at 5% annual interest, compounded monthly, for 10 years with no payments. Here \(r = 0.05\), \(m = 12\), \(t = 10\). So $$A = 10{,}000 \times \left(1 + \frac{0.05}{12}\right)^{120} \approx 10{,}000 \times 1.647009 \approx \mathbf{\$16{,}470.09}$$ The total interest accrued is about $6,470.09.

FAQ

Does this assume any payments? No. This calculator assumes zero payments are made during the term, so all interest compounds onto the balance.

Why does compounding frequency matter? The more often interest is added, the sooner it starts earning interest itself, which slightly increases the final balance for the same stated rate.

Can I use it for savings? Yes — the same formula gives the future value of a one-time deposit with compound interest.