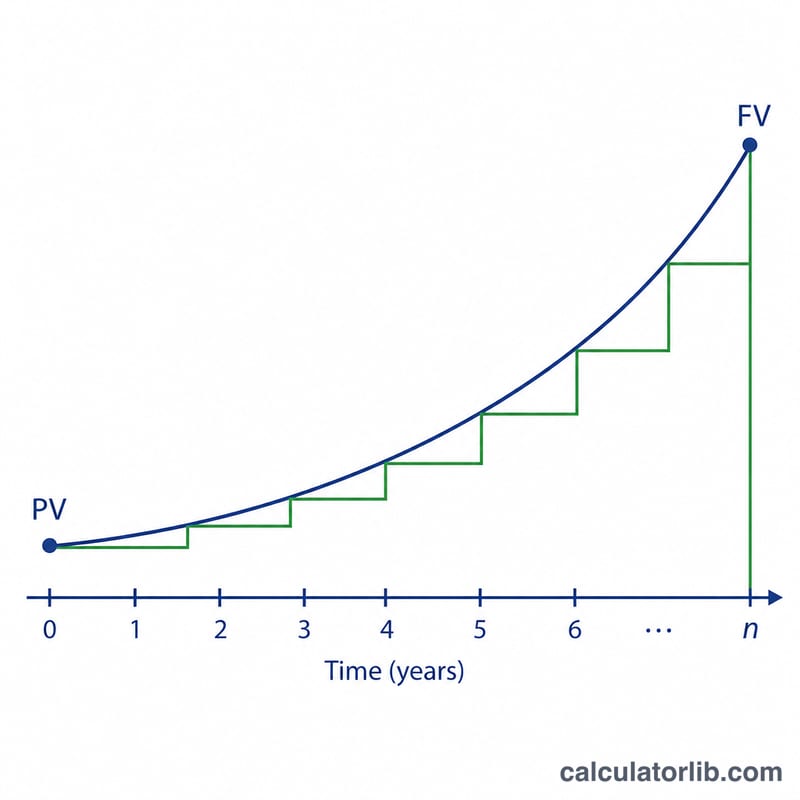

What this calculator does

This tool works backward from a known result: you supply how much you started with (the principal, PV), how much you ended with (the final amount including interest, FV), how many years it took (n), and how often interest was compounded each year (k). It then solves for the annual interest rate two ways — the nominal annual rate (the quoted APR that compounds k times a year) and the effective annual rate (the true annualized yield). It is pure finance math and applies in any currency or country.

How to use it

Enter the principal and final amount in the same currency. Enter the number of elapsed years (decimals allowed). Choose the compounding period — annually, semiannually, quarterly, monthly, or daily. The calculator returns both rates as percentages. If the final amount is below the principal, both rates are negative (a loss), which is still valid.

The formula explained

Let \(g = \text{FV} / \text{PV}\) be the growth ratio. Over the term there are \(n \times k\) compounding periods, so the per-period rate is \(g^{1/(nk)} - 1\). Multiplying by \(k\) annualizes it into the nominal rate \(r\). The effective rate \(R = g^{1/n} - 1\) is the single yearly multiplier that produces the same growth. They satisfy \((1 + r/k)^{k} - 1 = R\), so \(R \ge r\) whenever \(k > 1\), and they are equal when \(k = 1\).

$$r_{\text{nom}} = \text{k} \left[\left(\frac{\text{FV}}{\text{PV}}\right)^{\frac{1}{\text{n}\cdot\text{k}}} - 1\right] \times 100\%$$ $$r_{\text{eff}} = \left[\left(\frac{\text{FV}}{\text{PV}}\right)^{\frac{1}{\text{n}}} - 1\right] \times 100\%$$

Worked example

PV = 100,000, FV = 150,000, n = 8 years, monthly compounding (k = 12). \(g = 1.5\), \(n \times k = 96\). The per-period rate is \(1.5^{1/96} - 1 = 0.0042325\), so $$r = 12 \times 0.0042325 = 5.079\%$$ The effective rate is $$1.5^{1/8} - 1 = 5.199\%$$

FAQ

Nominal vs effective — which should I quote? The effective annual rate lets you compare products with different compounding fairly; the nominal rate is the stated APR.

Can I use months instead of years? Convert to years first (e.g. 18 months = 1.5 years).

Why are both rates the same sometimes? With annual compounding (k = 1) nominal and effective rates are identical. Results are informational; banks may round differently.