What Is Ending Inventory?

Ending inventory is the total value of goods a business still has on hand at the close of an accounting period. It appears as a current asset on the balance sheet and directly affects reported profit. This calculator finds ending inventory using the standard accounting identity: beginning inventory plus purchases minus the cost of goods sold (COGS).

How to Use the Calculator

Enter three figures: your beginning inventory (the value carried over from the prior period), your net purchases made during the period, and your cost of goods sold. The tool instantly returns your ending inventory along with the goods available for sale. All values should be entered in the same currency and cost basis.

The Formula Explained

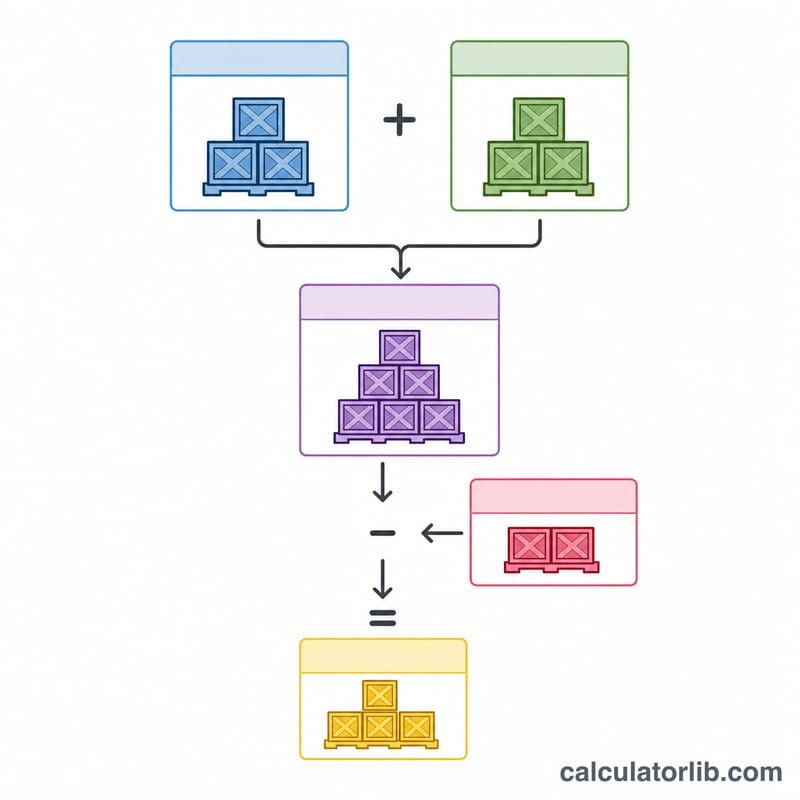

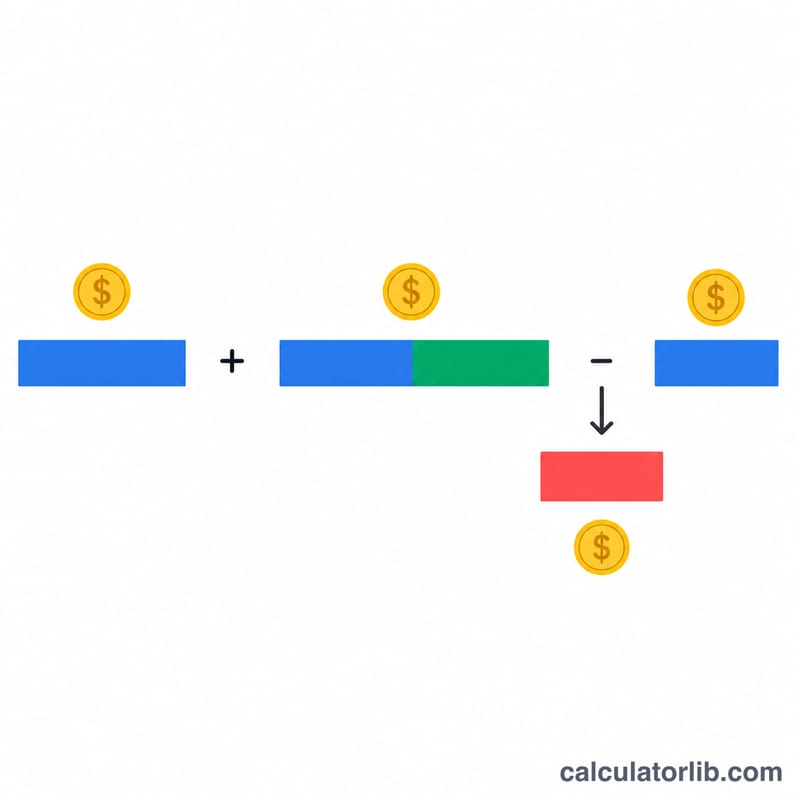

The relationship is straightforward: Ending Inventory = Beginning Inventory + Purchases − COGS.

$$\text{Ending Inventory} = \text{Beginning Inventory} + \text{Net Purchases} - \text{COGS}$$Beginning inventory and purchases together form the goods available for sale. Whatever you did not sell (i.e., goods available minus COGS) remains as ending inventory. This identity underlies periodic inventory systems and the calculation of COGS itself.

Worked Example

Suppose a retailer starts the quarter with $10,000 of inventory, buys $5,000 more, and records $8,000 in cost of goods sold. Goods available for sale = \(\$10{,}000 + \$5{,}000 = \$15{,}000\). Ending inventory:

$$\$15{,}000 - \$8{,}000 = \mathbf{\$7{,}000}$$That $7,000 carries forward as next period's beginning inventory.

FAQ

Can ending inventory be negative? Mathematically yes if COGS exceeds goods available, but in practice a negative result signals a data or counting error.

What counts as net purchases? Gross purchases minus purchase returns, allowances, and discounts, plus freight-in.

How does this relate to COGS? The same equation rearranges to \(\text{COGS} = \text{Beginning Inventory} + \text{Purchases} - \text{Ending Inventory}\), so a physical count of ending inventory lets you derive COGS.