What Is a PMI Calculator?

This calculator applies to US conventional mortgages. Private Mortgage Insurance (PMI) is a premium lenders require when your down payment is less than 20% of the home's value (a loan-to-value ratio above 80%). PMI protects the lender — not you — if you default, and it is usually added to your monthly mortgage payment. This tool estimates your monthly and annual PMI cost from your loan balance and the annual PMI rate quoted by your lender.

How to Use It

Enter your loan amount (the amount you are borrowing, not the home price) and your annual PMI rate as a percentage. Typical PMI rates range from about 0.3% to 1.5% per year depending on your credit score and down payment. The calculator returns the monthly premium and the total yearly cost.

The Formula Explained

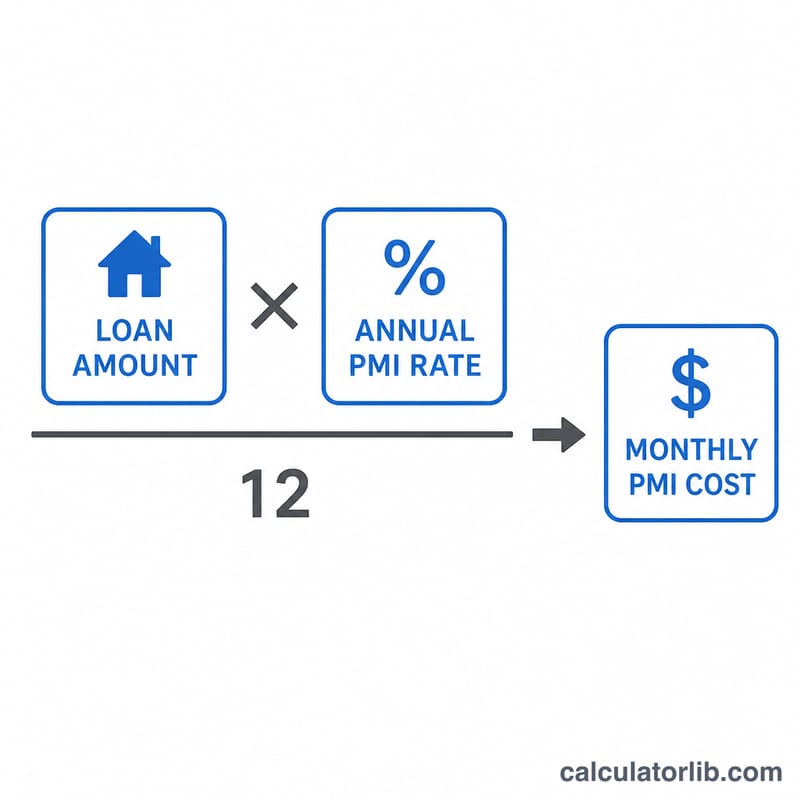

The yearly PMI cost equals the loan amount multiplied by the annual rate. Divide by 12 to get the monthly premium:

$$\text{Monthly PMI} = \frac{\text{Loan Amount} \times \frac{\text{PMI Rate (\%)}}{100}}{12}$$

For example, with a $250,000 loan and a 0.5% annual rate: annual PMI = \(250{,}000 \times 0.005 = \$1{,}250\), and monthly PMI = \(1{,}250 \div 12 \approx\) $104.17.

FAQ

When does PMI go away? On conventional loans, you can request PMI cancellation once your loan-to-value reaches 80%, and lenders must automatically terminate it at 78% LTV based on the original amortization schedule.

Is PMI the same as the rate? No. PMI is separate insurance. The rate here is a flat annual percentage of the loan balance, while some lenders may recalculate it as the balance declines.

Can I avoid PMI? Yes — putting down 20% or more, using a piggyback loan, or choosing lender-paid PMI (built into a higher interest rate) can avoid a separate PMI line item.