What Is Sum of Years Digits Depreciation?

The Sum of Years Digits (SYD) method is an accelerated depreciation technique that charges a larger expense in the early years of an asset's life and smaller amounts later. It is useful for assets that lose value quickly or are most productive when new, such as vehicles and technology equipment. This calculator works for any currency — just treat the dollar sign as your local unit.

How to Use the Calculator

Enter the asset's original cost, its estimated salvage (residual) value at the end of its useful life, the total useful life in years, and the specific year for which you want the depreciation expense. The tool returns that year's depreciation, the sum-of-years-digits denominator, the accumulated depreciation up to and including the chosen year, and the remaining book value.

The Formula Explained

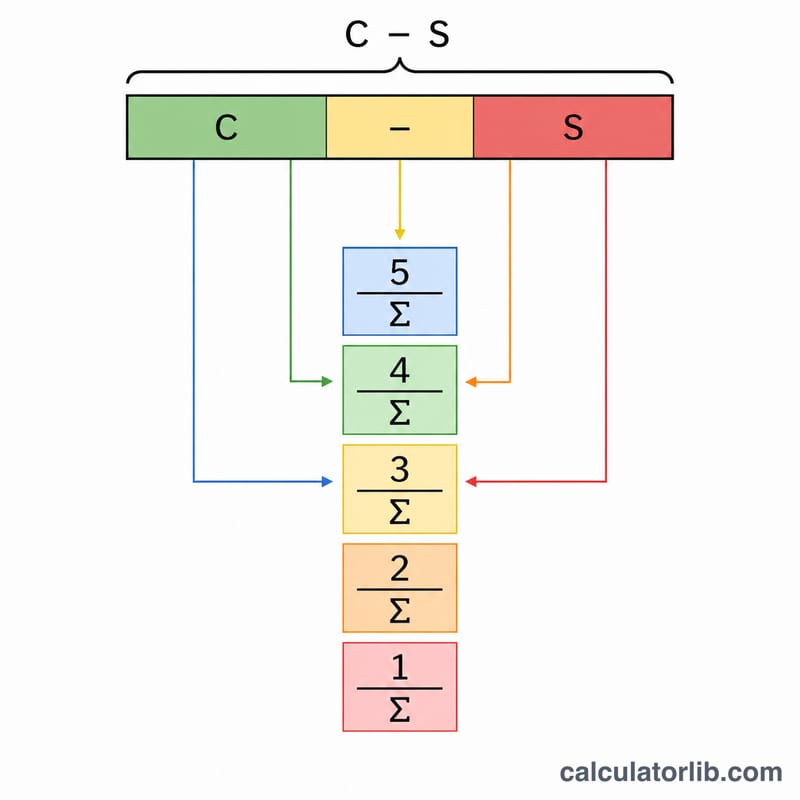

First find the depreciable base: cost minus salvage value. Then compute the sum of the digits of the useful life: \(\text{SYD} = \dfrac{n(n+1)}{2}\). For year \(t\), the remaining life is \(n - t + 1\). The depreciation for that year is the depreciable base multiplied by the fraction (remaining life ÷ SYD). Each year the fraction shrinks, so the expense declines over time.

$$\text{Depreciation} = (\text{Cost} - \text{Salvage}) \times \dfrac{\text{Remaining Life}}{\frac{n(n+1)}{2}}$$

$$D_t = (C - S)\times\dfrac{n - t + 1}{\frac{n(n+1)}{2}}$$

Worked Example

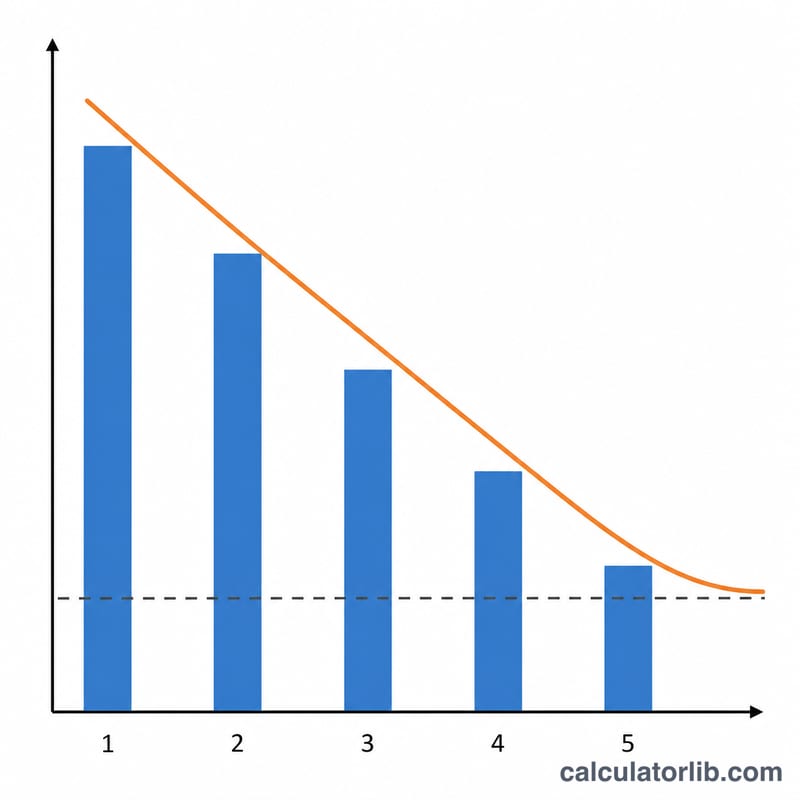

Suppose an asset costs $10,000, has a $1,000 salvage value and a 5-year life. The depreciable base is $9,000 and \(\text{SYD} = \dfrac{5\times 6}{2} = 15\). In year 1 the remaining life is 5, so depreciation $$= 9{,}000 \times \dfrac{5}{15} = \$3{,}000.$$ In year 2 it falls to \(9{,}000 \times \dfrac{4}{15} = \$2{,}400\), and so on until year 5 (\(9{,}000 \times \dfrac{1}{15} = \$600\)). After year 1 the book value is \(\$10{,}000 - \$3{,}000 = \$7{,}000\).

FAQ

Why use SYD over straight-line? SYD front-loads depreciation, better matching expense to assets that are most valuable when new and offering earlier tax deductions.

Can total depreciation exceed the cost? No. Over the full life, total SYD depreciation equals exactly cost minus salvage, so book value never drops below salvage.

What if salvage value is zero? Then the full cost is depreciated; simply enter 0 for salvage value.