What Is Units of Production Depreciation?

The units of production (or units of activity) method spreads an asset's cost across its productive output rather than over time. Instead of an equal charge each year like straight-line depreciation, expense rises and falls with actual usage — making it ideal for machinery, vehicles, or equipment whose wear depends on how much they are used.

How to Use This Calculator

Enter four values: the original asset cost, the estimated salvage value at the end of its life, the total estimated units the asset is expected to produce over its entire life, and the units produced this period. The calculator returns the depreciation expense for the period, the per-unit rate, and the remaining book value.

The Formula Explained

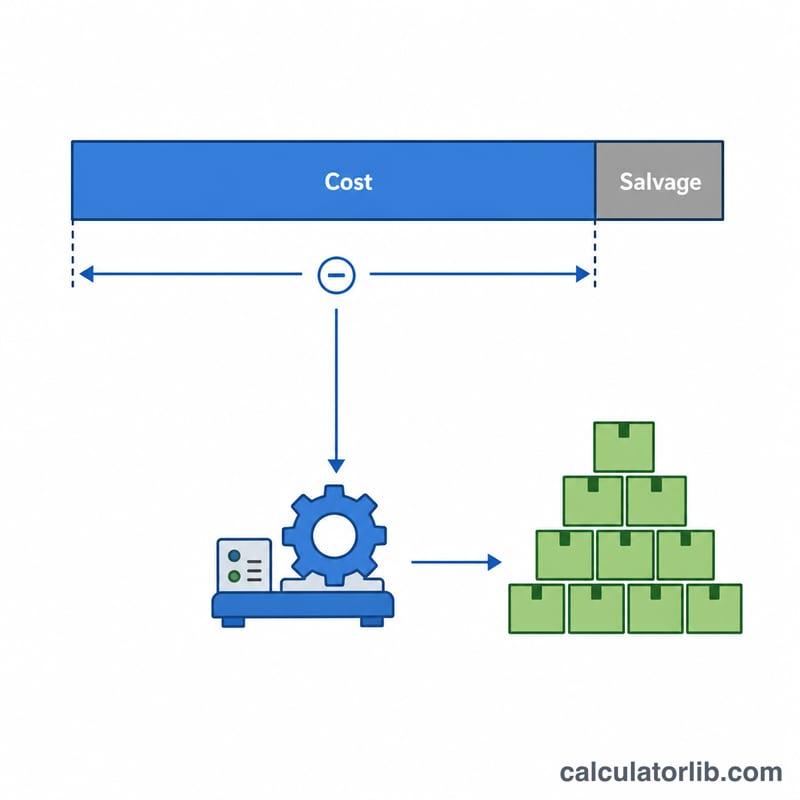

First find the depreciable base by subtracting salvage value from cost. Divide that by total estimated units to get the depreciation rate per unit. Multiply the rate by the units produced in the period:

$$\text{Depreciation} = \dfrac{\text{Cost} - \text{Salvage}}{\text{Total Units}} \times \text{Units Produced}$$

This guarantees the asset is never depreciated below its salvage value once all estimated units are produced.

Worked Example

A machine costs $50,000 with a $5,000 salvage value and is expected to produce 100,000 units. The depreciable base is $45,000, giving a rate of $0.45 per unit. If it produces 12,000 units this year, depreciation is $$0.45 \times 12{,}000 = \$5{,}400$$ leaving a book value of $44,600.

FAQ

When should I use this method? Use it when an asset's value loss tracks usage rather than the passage of time, such as production equipment or fleet vehicles measured in units, hours, or miles.

What if I overestimate total units? If actual output exceeds the estimate, you stop depreciating once accumulated depreciation reaches the depreciable base — you cannot depreciate past salvage value.

Does the per-unit rate change? The rate stays fixed unless you revise the cost, salvage, or total-units estimate, in which case you recalculate going forward.