这个计算器能做什么

"月供预算反推可贷款额度计算器"是从你每月愿意承担的还款金额出发,倒推出最适合这个预算的最高贷款本金。它解决的不是"我每月要还多少钱?",而是"我到底能贷多少?"——非常适合在固定开支上限内挑选房贷、车贷或个人消费贷款。

如何使用

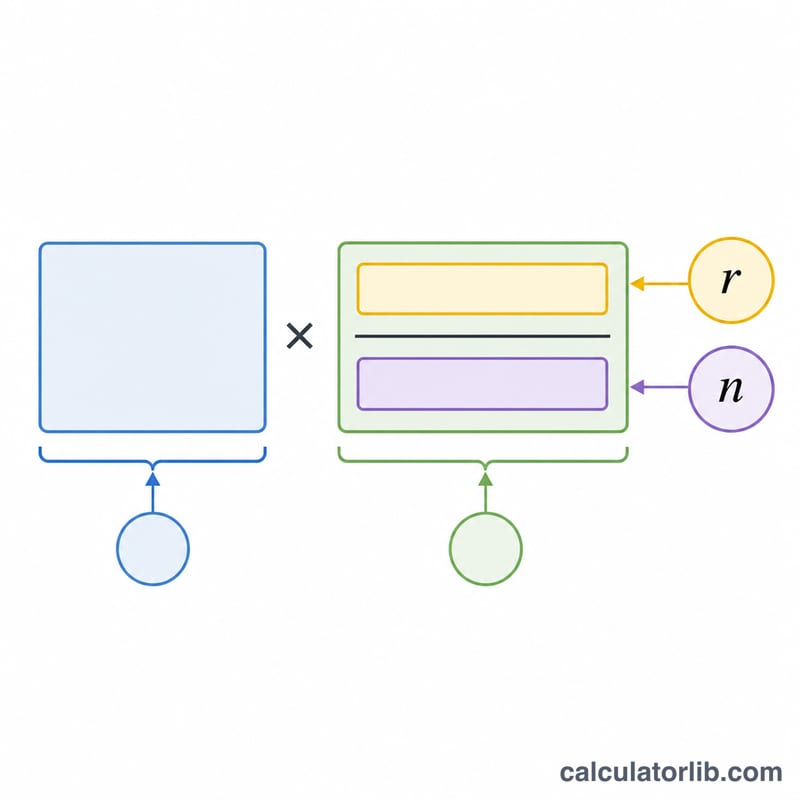

填入你每月能承受的还款金额、贷款机构给出的年利率,以及以年为单位的贷款期限。计算器会把年利率换算成月利率,算出总还款期数,并给出最高可贷本金,同时显示整个贷款周期内的还款总额和累计利息。

公式解析

这里用到的是年金现值公式:$$L = M \cdot \frac{1 - (1+r)^{-n}}{r}$$其中 \(r\) 是月利率(年利率 ÷ 100 ÷ 12),\(n\) 是还款总期数(年数 × 12)。当利率为零时,可贷额度就等于 \(M \times n\)。

Advertisement

实例演算

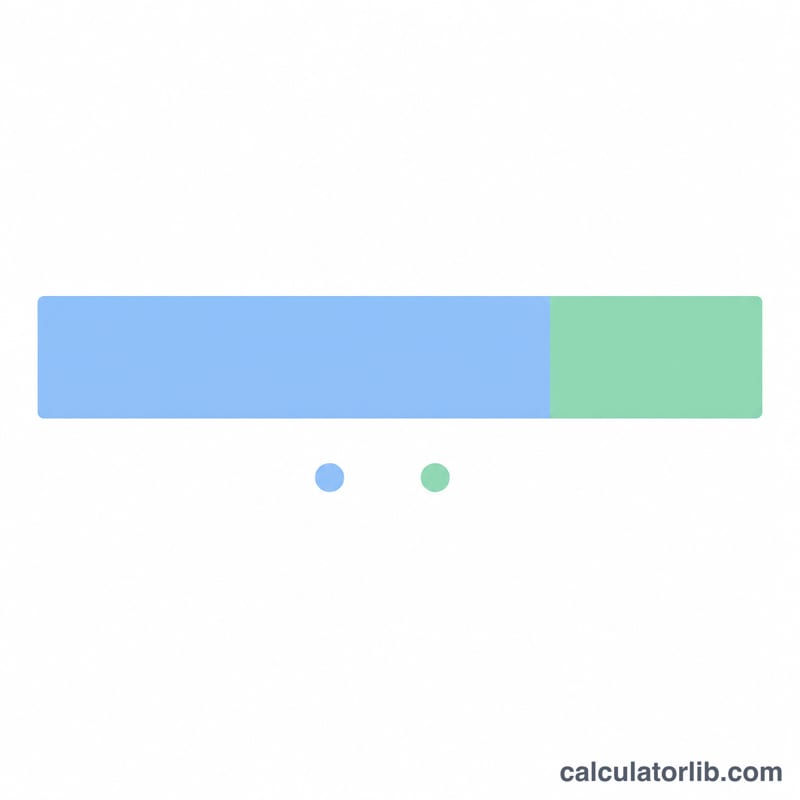

假设你每月可还 $1,500,年利率为 6%,期限 30 年。那么月利率为 \(0.06 \div 12 = 0.005\),\(n = 360\)。可贷额度 $$L = 1500 \times \frac{1 - 1.005^{-360}}{0.005} \approx \$250{,}187$$30 年间你总共支付 \(1500 \times 360 = \$540{,}000\),其中约 $289,813 是利息。

Advertisement

常见问题

结果包含房产税或保险吗?不包含。本计算器只算贷款本金和利息。如果是房贷,请另外为税费、保险和各项手续费留出预算。(注:本工具以美元和通用摊还公式为例,中国国内的房贷可参考等额本息利率与 LPR 政策,具体规则略有不同。)

该填哪个利率?请填写贷款机构给出的年(名义)利率,工具会自动除以 12 按月计息。

任何贷款都能用吗?可以——房贷、车贷和个人消费贷款都遵循相同的等额摊还计算逻辑。