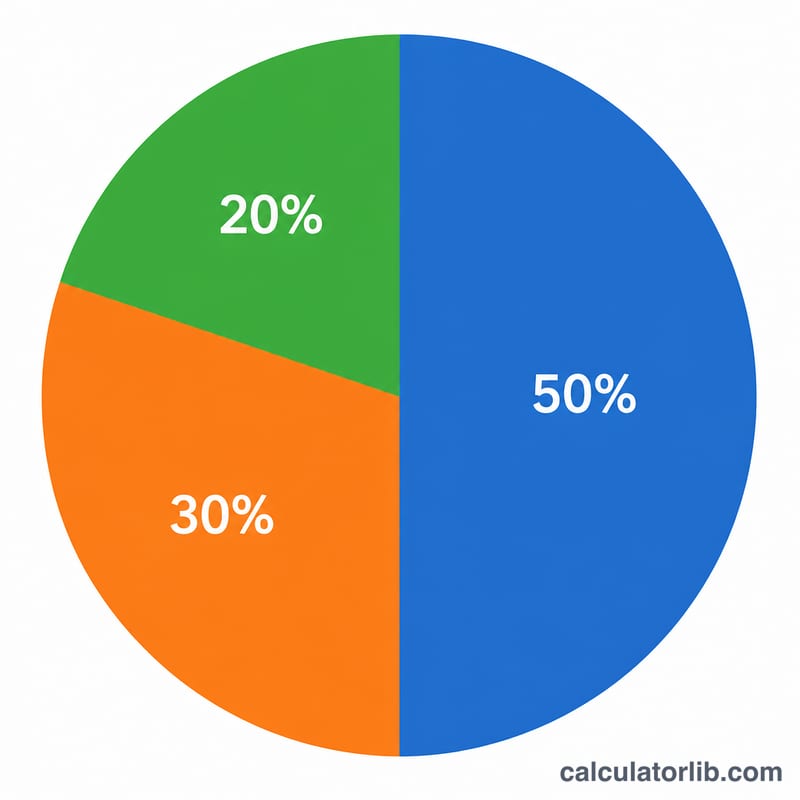

What is the 50/30/20 budget rule?

The 50/30/20 rule is a simple budgeting framework popularized by Senator Elizabeth Warren. It divides your monthly take-home (after-tax) income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It is intentionally easy to remember and works in any currency, making it a great starting point for people who want structure without tracking dozens of line items.

How to use this calculator

Enter your monthly after-tax income — the amount that actually lands in your bank account after taxes and payroll deductions. The calculator instantly shows how much should go to each bucket. Needs are essentials you cannot skip: rent or mortgage, groceries, utilities, insurance, and minimum debt payments. Wants are lifestyle choices: dining out, subscriptions, hobbies, and travel. Savings covers emergency funds, investing, and extra debt payments beyond the minimum.

The formula explained

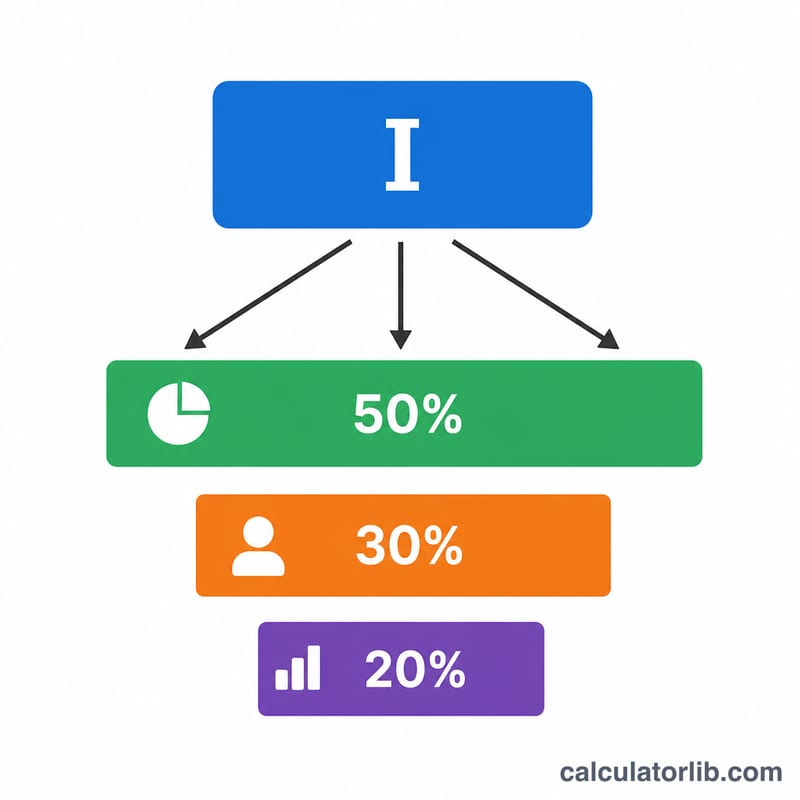

The math is straightforward percentage allocation of your income \(I\):

$$\text{Needs}=0.50\times I,\quad \text{Wants}=0.30\times I,\quad \text{Savings}=0.20\times I$$Because the three percentages add up to 100%, every dollar of income is assigned a job.

Worked example

Suppose your monthly after-tax income is 4,000. Then $$\text{Needs}=0.50\times 4{,}000=2{,}000,\quad \text{Wants}=0.30\times 4{,}000=1{,}200,\quad \text{Savings}=0.20\times 4{,}000=800.$$ You would aim to keep essential bills at or under 2,000, cap discretionary spending around 1,200, and direct at least 800 toward savings and debt.

50/30/20 Split at Different Income Levels

The 50/30/20 rule divides your monthly after-tax (take-home) income into three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. The table below shows how each category scales across several common monthly net income levels.

| Monthly After-Tax Income | Needs (50%) | Wants (30%) | Savings (20%) |

|---|---|---|---|

| $2,000 | $1,000 | $600 | $400 |

| $3,000 | $1,500 | $900 | $600 |

| $4,000 | $2,000 | $1,200 | $800 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $7,000 | $3,500 | $2,100 | $1,400 |

Each amount is simply the income multiplied by the category percentage. For example, at $4,000 per month: \(\text{Needs} = 0.50 \times 4000 = 2000\), \(\text{Wants} = 0.30 \times 4000 = 1200\), and \(\text{Savings} = 0.20 \times 4000 = 800\). The 20% savings slice can also fund extra debt payments — at $800 a month it could, for instance, accelerate paying down a credit card balance.

Key Budgeting Terms Explained

- After-tax (net) income

- The money that actually lands in your account after income taxes, payroll taxes, and other mandatory withholdings are removed. The 50/30/20 rule is always applied to this take-home figure, not your gross salary.

- Needs (50%)

- Essential expenses you cannot reasonably avoid: rent or mortgage, utilities, groceries, insurance, transportation to work, and minimum debt payments. If you stopped paying these, you would face serious consequences such as eviction, default, or loss of essential services.

- Wants (30%)

- Lifestyle spending that is nice to have but not essential: dining out, streaming subscriptions, hobbies, travel, upgraded phone plans, and entertainment. These are choices that improve quality of life rather than survival.

- Savings (20%)

- Money directed toward your financial future — emergency fund contributions, retirement accounts, investments, and extra (above-minimum) debt repayment. This bucket builds long-term security and net worth.

- Minimum debt payment

- The smallest amount a lender requires you to pay each month to keep a loan or credit card in good standing. In the 50/30/20 framework, minimum payments count as a need, while any additional payoff above the minimum counts toward the 20% savings/debt category.

- Discretionary spending

- Spending you have full control over from month to month — essentially the same idea as "wants." Trimming discretionary spending is the fastest way to free up money for savings or debt without affecting your essential needs.

FAQ

Should I use gross or net income? Use net (after-tax) income, since that is what you can actually spend. If your employer already deducts retirement contributions, you may count those toward the 20% savings bucket.

What if my needs exceed 50%? In high-cost areas this is common. Treat the 50/30/20 split as a target — trim wants first, and look for ways to lower fixed costs over time.

Is the 20% savings before or after debt? The 20% bucket combines savings and any debt payments beyond the required minimums. Minimum required payments count as needs.