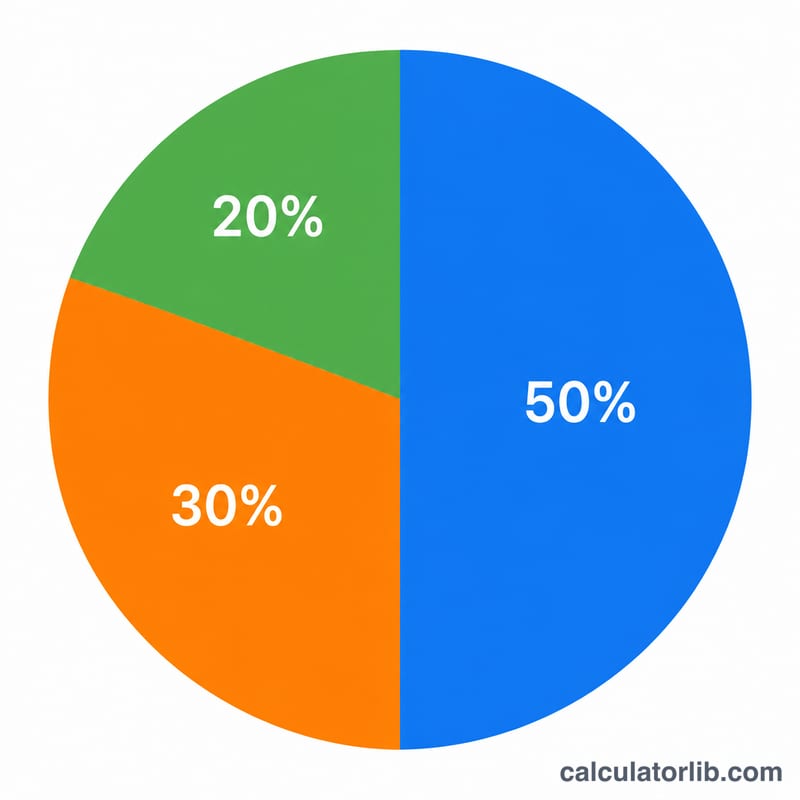

What Is the 50/30/20 Budget?

The 50/30/20 rule is a simple, popular framework for managing personal finances. It divides your monthly take-home (net) income into three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Because it works with percentages rather than fixed dollar amounts, it adapts to any income level and any currency, making it a universal starting point for building a budget.

How to Use This Calculator

Enter your monthly net income — the amount that actually lands in your bank account after taxes and deductions. The calculator instantly shows how much to allocate to each category. If you are paid weekly or annually, convert to a monthly figure first (multiply weekly pay by about 4.33, or divide annual net pay by 12).

The Formula Explained

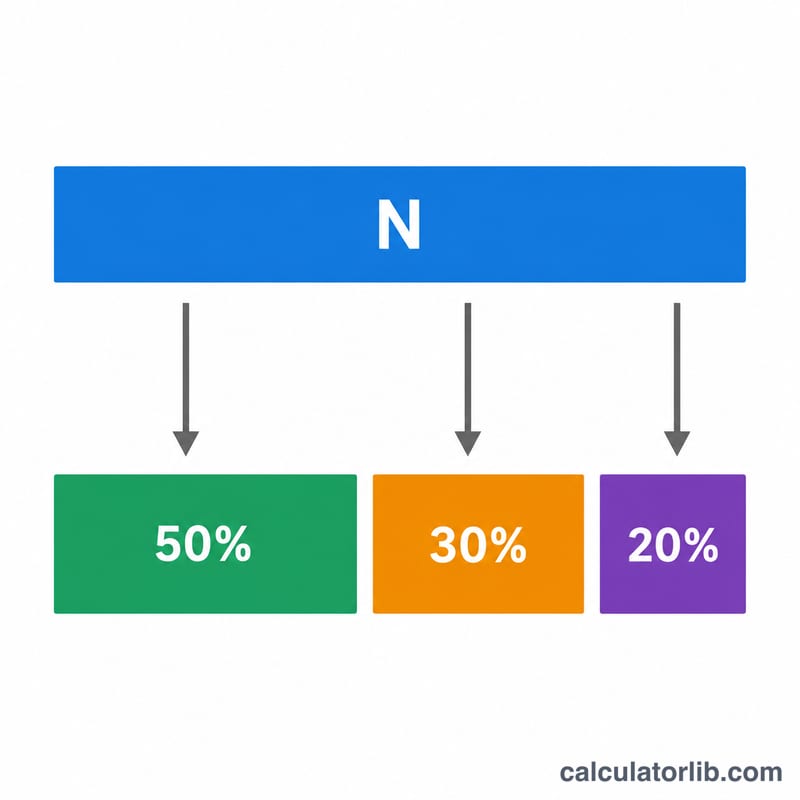

The math is straightforward. Given net income \(N\): Needs = \(N \times 0.50\), Wants = \(N \times 0.30\), and Savings = \(N \times 0.20\). The three categories always add up to 100% of your net income.

$$\begin{gathered} \text{Needs} = 0.50 \times \text{Net Income} \\[0.6em] \text{Wants} = 0.30 \times \text{Net Income} \\[0.6em] \text{Savings} = 0.20 \times \text{Net Income} \end{gathered}$$

Needs are essentials you can't skip: rent or mortgage, groceries, utilities, insurance, and minimum loan payments. Wants are lifestyle choices: dining out, subscriptions, hobbies, and travel. Savings covers your emergency fund, retirement contributions, and extra debt payoff.

Worked Example

Suppose your monthly net income is $4,000.

$$\text{Needs} = 4{,}000 \times 0.50 = \$2{,}000$$$$\text{Wants} = 4{,}000 \times 0.30 = \$1{,}200$$$$\text{Savings} = 4{,}000 \times 0.20 = \$800$$So you'd aim to keep essential spending under $2,000, discretionary spending under $1,200, and stash $800 every month.

FAQ

Should I use gross or net income? Use net (after-tax) income, since that is the money you can actually budget.

What if my needs are more than 50%? In high-cost areas this is common. Try trimming wants first, or treat 50/30/20 as a target to work toward over time.

Is the 20% savings before or after debt? The savings bucket includes extra debt repayment beyond minimums, plus building savings and investing — prioritize high-interest debt first.