What This Calculator Does

This tool estimates how much interest you can save by repaying your loan early instead of continuing to pay it off through scheduled monthly installments (EMIs). Because each EMI contains both principal and interest, settling the loan today means you only pay the remaining principal — and avoid all the future interest baked into the upcoming payments. The calculation is based on standard amortization mathematics and works for any equated installment loan such as a personal, auto, or home loan.

How to Use It

Enter three values: your fixed monthly payment (EMI), the loan's annual interest rate, and the number of payments still remaining. The calculator converts the annual rate to a monthly rate, discounts the remaining payments back to today's value to find the payoff amount (outstanding principal), and subtracts it from the total of all remaining payments to reveal your interest savings.

The Formula Explained

The monthly rate is \(i = \text{annual rate} \div 12 \div 100\). The outstanding principal is the present value of an annuity: $$\text{Outstanding} = \text{EMI}\times\dfrac{1-(1+i)^{-n}}{i}$$ The total you would otherwise pay is simply \(\text{EMI} \times n\). The difference, $$\text{InterestSaved} = (\text{EMI} \times n) - \text{Outstanding}$$ is the future interest you eliminate by prepaying now.

Worked Example

Suppose your EMI is 15,000, the annual rate is 10% (so \(i = 0.0083333\)), and you have 60 payments left. The total remaining is $$15{,}000 \times 60 = 900{,}000$$ The outstanding principal is $$15{,}000 \times \dfrac{1 - (1.0083333)^{-60}}{0.0083333} \approx 705{,}968$$ Interest saved $$\approx 900{,}000 - 705{,}968 = 194{,}032$$ By settling the loan today you avoid roughly 194,032 in interest.

Key Terms Explained

- EMI (Equated Monthly Instalment)

- The fixed amount you pay each month, covering both interest and principal repayment. In this calculator it is entered as a single recurring payment that stays constant over the remaining term.

- Annual vs. monthly interest rate

- The rate is usually quoted as an annual percentage. For monthly EMI math it is converted to a monthly rate by dividing by 12 (and by 100 to convert from a percentage), so \(i = \text{rate} / 1200\). For example, a 10% annual rate gives a monthly rate of \(10/1200 \approx 0.008333\).

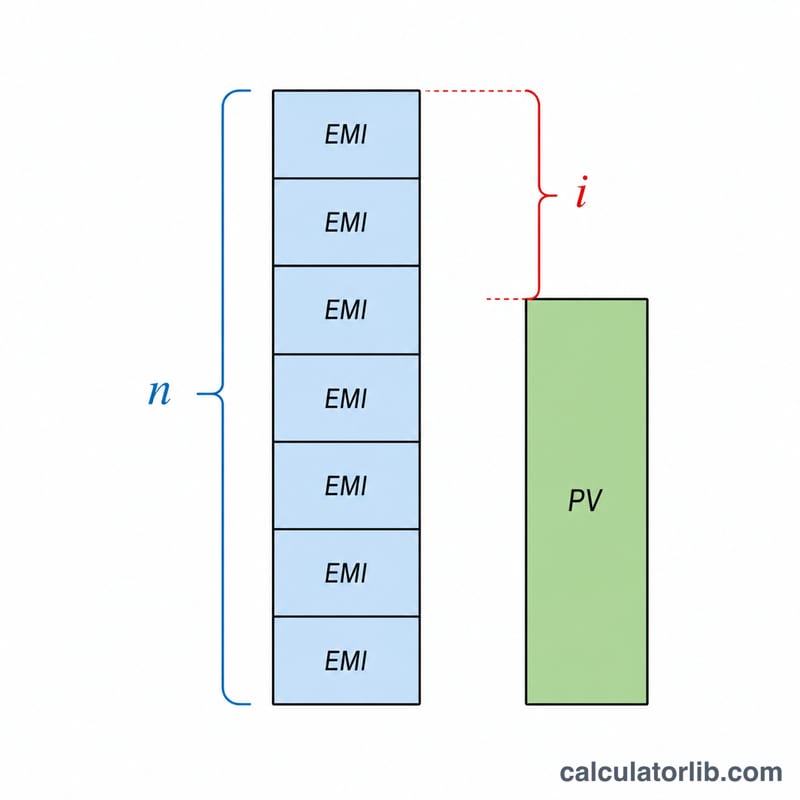

- Outstanding / principal balance

- The amount of loan principal still owed. As you pay EMIs, the principal balance falls; the outstanding balance equals the present value of all your remaining scheduled payments at the loan's rate.

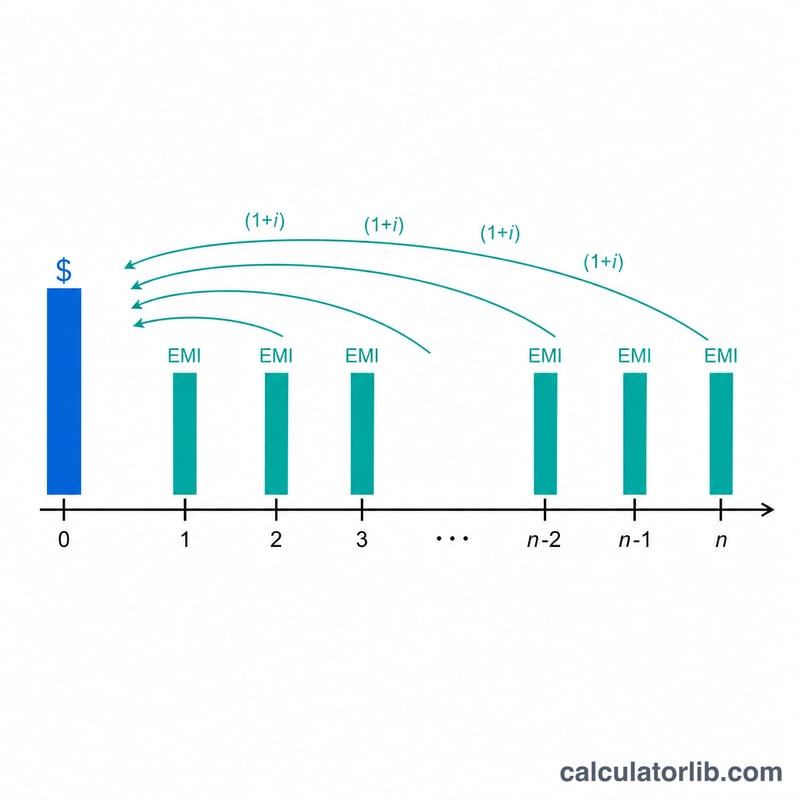

- Present value of an annuity

- The lump sum today that is financially equivalent to a stream of equal future payments, discounted at the loan rate: \(\text{PV} = \text{EMI} \cdot \frac{1-(1+i)^{-n}}{i}\). It is the basis for the payoff amount.

- Payoff / foreclosure amount

- The single lump sum needed to clear the loan today. It equals the present value of the remaining payments — less than the simple total of remaining EMIs because future interest no longer accrues once the loan is settled.

- Prepayment penalty

- A fee some lenders charge for paying off a loan early, often a percentage of the outstanding balance. It reduces the net benefit of prepaying and is not included in this calculator's interest-saved figure.

- Interest saved

- The future interest you avoid by closing the loan now: the sum of all remaining EMIs minus the payoff amount, \(\text{EMI} \times n - \text{PV}\).

Interpreting Your Result

The calculator returns two main figures, and it helps to read them together:

- Payoff amount — the lump sum required to clear the loan today. It is the present value of your remaining EMIs, discounted at the loan's monthly rate. It is always less than EMI × remaining months, because settling now stops future interest from accruing.

- Interest saved — the gross future interest you avoid: the total of all remaining scheduled payments minus the payoff amount. This is the headline benefit of prepaying.

To estimate the real economic benefit, subtract any costs of prepaying:

$$\text{Net benefit} = \text{Interest saved} - \text{Prepayment penalty/fees}$$

If your loan carries a foreclosure charge (for example, a percentage of the outstanding balance), deduct it from the interest saved to see whether prepaying still leaves you ahead. Some loans also have lock-in periods during which prepayment is restricted or more heavily penalized.

Savings are largest earlier in the loan term. In a standard EMI schedule, early payments are weighted toward interest, so a larger share of future interest remains unpaid the further you are from the final instalment. Prepaying when many months remain therefore avoids more interest than prepaying near the end. Likewise, higher interest rates make prepayment more valuable, because each future payment contains more interest to be saved.

This calculator assumes a fixed EMI and a constant interest rate over the remaining term, and it does not account for lender-specific fees, taxes, or rounding in your actual amortization schedule. The figures are estimates for comparison and planning. This is general information, not professional financial advice; confirm exact payoff figures and any penalties with your lender before acting.

FAQ

Does this account for prepayment penalties? No. Many lenders charge a foreclosure or prepayment fee; subtract any such charge from the interest saved shown here to find your net benefit.

Why is the payoff amount less than the remaining payments? Because future payments include interest that has not yet accrued. Paying today removes that interest, so the lump-sum payoff is smaller than the sum of future EMIs.

Is this currency-specific? No — the math is universal. Enter all amounts in the same currency you use for your loan.