What Is Accrued Interest?

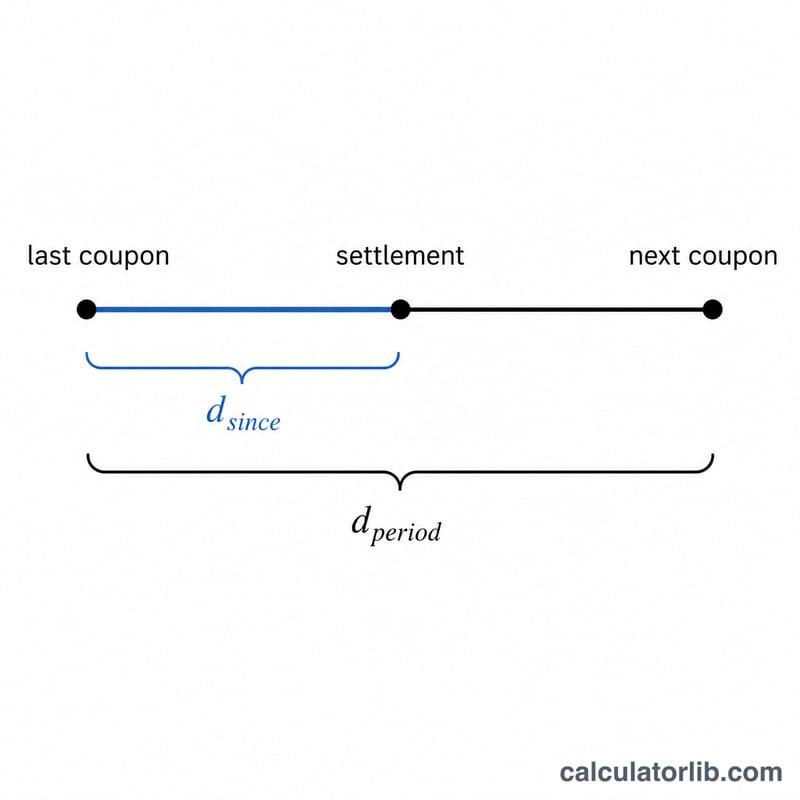

When a bond is sold between two coupon payment dates, the seller has earned interest for the portion of the coupon period they held the bond but has not yet received that cash. To compensate them, the buyer pays this earned amount — called accrued interest — on top of the bond's quoted (clean) price. The total amount exchanged, clean price plus accrued interest, is the dirty price.

How to Use This Calculator

Enter the bond's face value (par, e.g. 1,000), the annual coupon rate as a percentage, the number of days since the last coupon was paid, the total days in the current coupon period, and the coupon frequency (how many coupons are paid per year). The calculator returns the accrued interest, the full periodic coupon payment, and the fraction of the period that has elapsed.

The Formula Explained

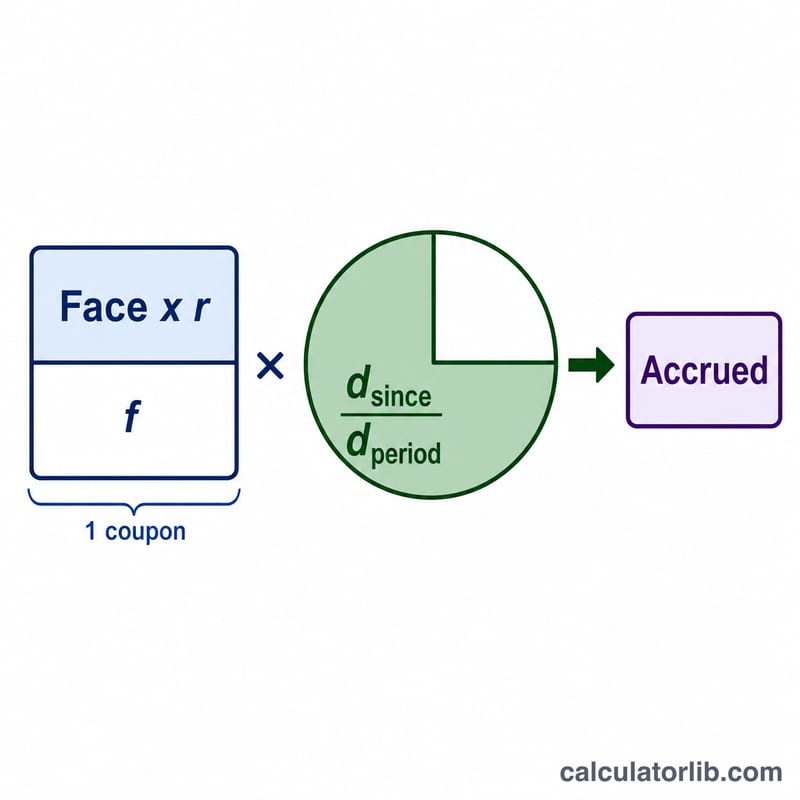

Each coupon payment equals Face × rate ÷ frequency. Accrued interest is simply that payment multiplied by the fraction of the period that has passed: days since coupon ÷ days in period. The day-count basis you pick (actual/actual, 30/360, etc.) determines the day numbers you enter — the math here works with whatever counts you supply.

$$\text{Accrued} = \frac{\text{Face} \times r}{f} \times \frac{d_{\text{since}}}{d_{\text{period}}}$$

$$C = \frac{\text{Face} \times r}{f}$$

Worked Example

A $1,000 bond pays a 5% annual coupon semi-annually (frequency 2). The full coupon payment is $$1{,}000 \times 0.05 \div 2 = \$25.$$ If 90 days have passed in a 182-day period, the fraction is $$90 \div 182 = 0.4945.$$ Accrued interest = $$25 \times 0.4945 = \$12.36.$$ $12.36.

Day-Count Conventions Reference

The accrued interest formula multiplies the per-period coupon by the fraction \(\frac{\text{Days Since}}{\text{Days in Period}}\). What goes into that numerator and denominator depends on the bond's day-count convention — the market rule that defines how calendar time is counted. Using the wrong convention shifts the accrued amount, so always match the convention to the instrument before entering daysSince and daysInPeriod.

| Convention | Days Since Last Coupon (numerator) | Days in Period (denominator) | Typically Used By |

|---|---|---|---|

| Actual/Actual (ICMA / Actual-Actual) | Actual calendar days from the last coupon to settlement | Actual calendar days in the current coupon period (e.g. 181, 182, 184) | US Treasury notes & bonds; most government bonds |

| 30/360 (Bond Basis) | Days counted assuming every month has 30 days (e.g. day = 360 × Δyear + 30 × Δmonth + Δday) | 180 days for a semiannual period (360 ÷ 2) | US corporate bonds, municipal bonds, many agency bonds |

| Actual/360 | Actual calendar days from the last coupon to settlement | 360 days (treated as a fixed-length year; period = 360 ÷ frequency) | Money-market instruments: commercial paper, CDs, USD/EUR floating-rate notes, repo |

| Actual/365 (Fixed) | Actual calendar days from the last coupon to settlement | 365 days (period = 365 ÷ frequency) | GBP money markets, some sterling and Commonwealth bonds, certain loans |

How to read this for the calculator. For an Actual/Actual Treasury, count the literal calendar days for both fields. For a 30/360 corporate bond on a semiannual schedule, set daysInPeriod to 180 and compute daysSince with the 30-day-month rule. For money-market Actual/360, the "period" denominator is 360 divided by the number of payments per year. The coupon frequency (1, 2, 4 or 12) should match the bond's payment schedule so the per-period coupon is correct.

Note that 30/360 and Actual/Actual usually give slightly different accrued figures for the same dates, because actual calendar months are rarely exactly 30 days. The difference is largest near month-ends (28-, 29- and 31-day months) and shrinks to zero at the coupon dates themselves, where accrued interest resets to a full period.

FAQ

Why does the buyer pay accrued interest? Because the next full coupon goes entirely to whoever owns the bond on the payment date — the buyer. Paying accrued interest reimburses the seller for the interest they earned but won't collect.

What is clean vs dirty price? The clean (quoted) price excludes accrued interest; the dirty price is what actually changes hands and equals clean price plus accrued interest.

Which day-count should I use? US Treasuries use actual/actual, many corporate bonds use 30/360. Use the convention specified in the bond's terms to determine the days values you enter.