What Is the Average Daily Balance Method?

The average daily balance (ADB) method is the most common way credit card issuers calculate the interest you owe. Instead of charging interest on your balance at a single point in time, the issuer tracks your balance for every day of the billing cycle, adds those daily balances together, and divides by the number of days. Interest is then applied to that average. This calculator estimates your ADB and the resulting finance charge.

How to Use This Calculator

Enter your beginning balance for the cycle, the number of days in the billing cycle (usually 28–31), and your card's APR. If you made new charges or payments during the cycle, enter the amount and the day it posted so the daily balances adjust accurately. The calculator builds a day-by-day balance, averages it, and multiplies by the daily periodic rate to show your estimated interest.

The Formula Explained

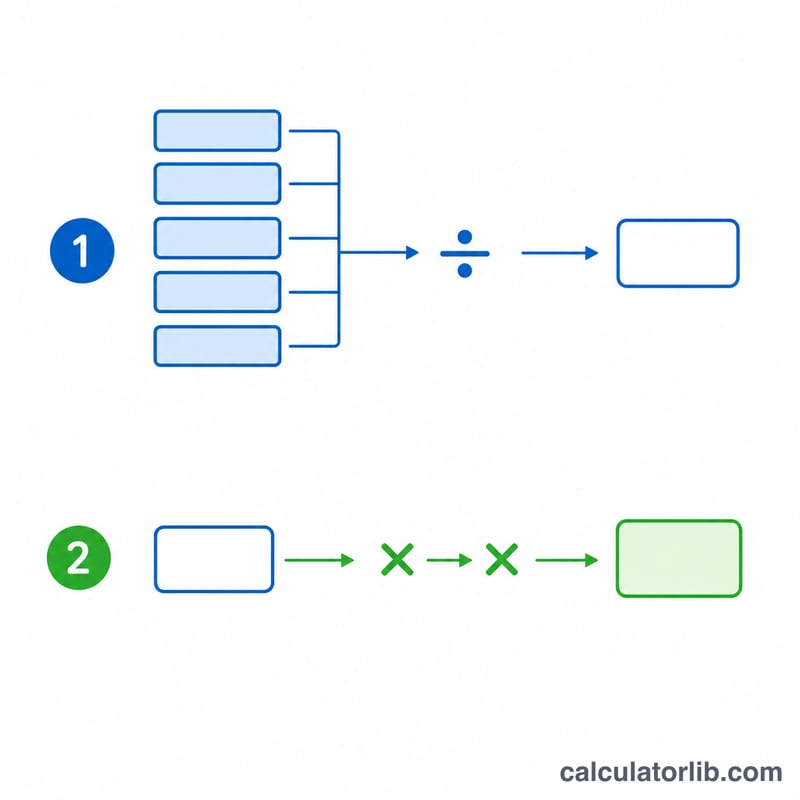

First, the daily periodic rate (DPR) is the APR divided by 365. The average daily balance is the sum of every day's ending balance divided by the number of days. The finance charge equals ADB × DPR × number of days.

$$\text{Finance Charge} = \text{ADB} \times \frac{\text{APR}/100}{365} \times \text{Days}$$$$\text{where}\quad \text{ADB} = \frac{1}{\text{Days}} \sum_{d=1}^{\text{Days}} B_d$$For example, with a steady $1,000 balance over 30 days at 18% APR: \(\text{DPR} = 0.18 \div 365 = 0.000493\), \(\text{ADB} = \$1{,}000\), and the finance charge =

$$1{,}000 \times 0.000493 \times 30 \approx \$14.79$$

Key Terms Defined

Understanding how credit card interest is calculated starts with a handful of core terms. Most U.S. card issuers use the average daily balance method, so these definitions describe that approach.

- Average Daily Balance (ADB): The sum of the account balance at the end of each day in the billing cycle, divided by the number of days in the cycle. It weights each balance by how long it stayed on the account, so a payment made early in the cycle lowers the ADB more than the same payment made late.

- Daily Periodic Rate (DPR): The interest rate applied to the balance each day. It equals the APR divided by the number of days in the year, normally \(\text{DPR} = \text{APR} / 365\). For example, an 18% APR gives a DPR of about \(0.18/365 = 0.0004932\), or roughly 0.0493% per day.

- APR (Annual Percentage Rate): The yearly cost of borrowing expressed as a percentage. For purchases, it is a nominal rate that is divided down to a daily rate; it does not include the compounding effect that the effective annual rate (APY) reflects.

- Billing cycle: The recurring period — typically 28 to 31 days — over which transactions are recorded before a statement is issued. The number of days in the cycle is the divisor in the ADB calculation and the multiplier in the finance charge.

- Finance charge: The dollar amount of interest assessed for the cycle. With the average daily balance method it equals \(\text{ADB} \times \text{DPR} \times \text{Days}\).

- Grace period: The interest-free window — usually at least 21 days — between the statement closing date and the payment due date. If you pay the full statement balance by the due date, no finance charge is assessed on new purchases; carrying a balance typically forfeits the grace period until the account is paid in full.

- Posting date: The date a transaction (charge or payment) is actually recorded to your account. The posting date — not the transaction date — determines which daily balances change, so a payment that posts a day later affects the ADB accordingly.

FAQ

Does paying mid-cycle reduce interest? Yes. Posting a payment earlier in the cycle lowers more daily balances, reducing your average and your interest.

Why divide APR by 365? The daily periodic rate spreads the annual rate across each day. Some issuers use 360 days; this tool uses 365.

Is this exact? It is a close estimate. Actual charges depend on your issuer's exact method, grace periods, and compounding rules.