What Is the Kelly Criterion?

The Kelly Criterion is a money-management formula that calculates the optimal fraction of your bankroll to wager on a bet or investment with a known edge. Developed by John L. Kelly Jr. in 1956, it maximizes the long-run growth rate of your capital while avoiding the risk of ruin that comes from over-betting. It is widely used by professional gamblers, sports bettors, and investors.

How to Use This Calculator

Enter three values: your win probability as a percentage, the net odds (b) you receive on a win, and your current bankroll. Net odds are expressed fractionally — if a winning bet pays 2 units of profit per 1 unit staked, enter 2. The calculator returns the Kelly fraction, the corresponding stake in your currency, and the more conservative half-Kelly figures.

The Formula Explained

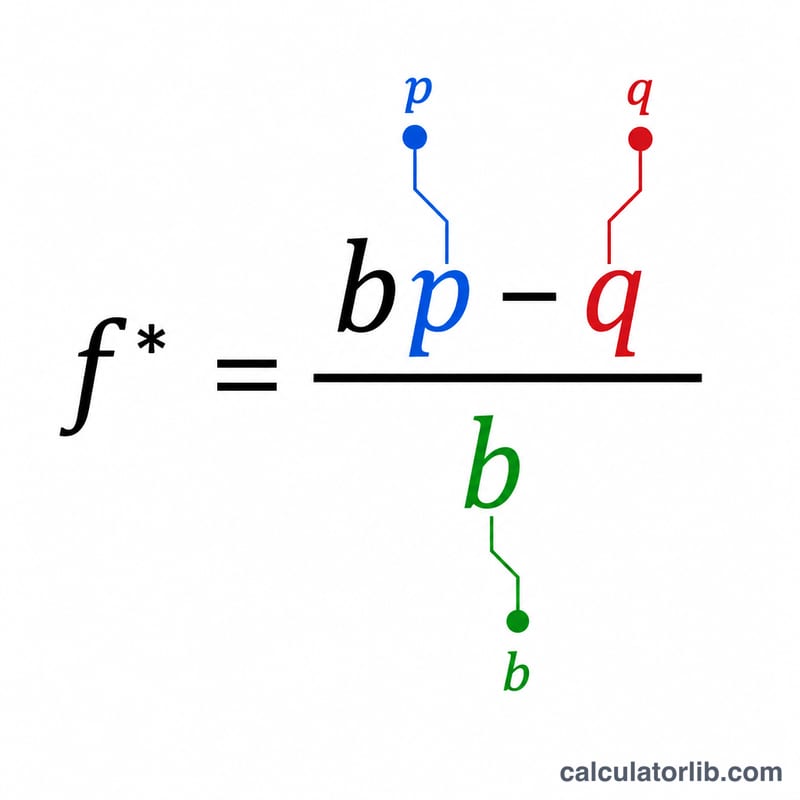

The Kelly formula is $$f^{*} = \frac{bp - q}{b}$$ where b is the net decimal odds, p is the probability of winning, and \(q = 1 - p\) is the probability of losing. A positive result means the bet has positive expected value and you should risk that fraction of your bankroll. A zero or negative result means you have no edge and should not bet.

Worked Example

Suppose you have a 60% chance of winning (\(p = 0.6\), \(q = 0.4\)) on a bet that pays 1-to-1 (\(b = 1\)). Then $$f^{*} = \frac{1 \times 0.6 - 0.4}{1} = 0.2$$ or 20% of your bankroll. With a $1,000 bankroll, the full-Kelly stake is $200, and a more cautious half-Kelly bet is $100.

FAQ

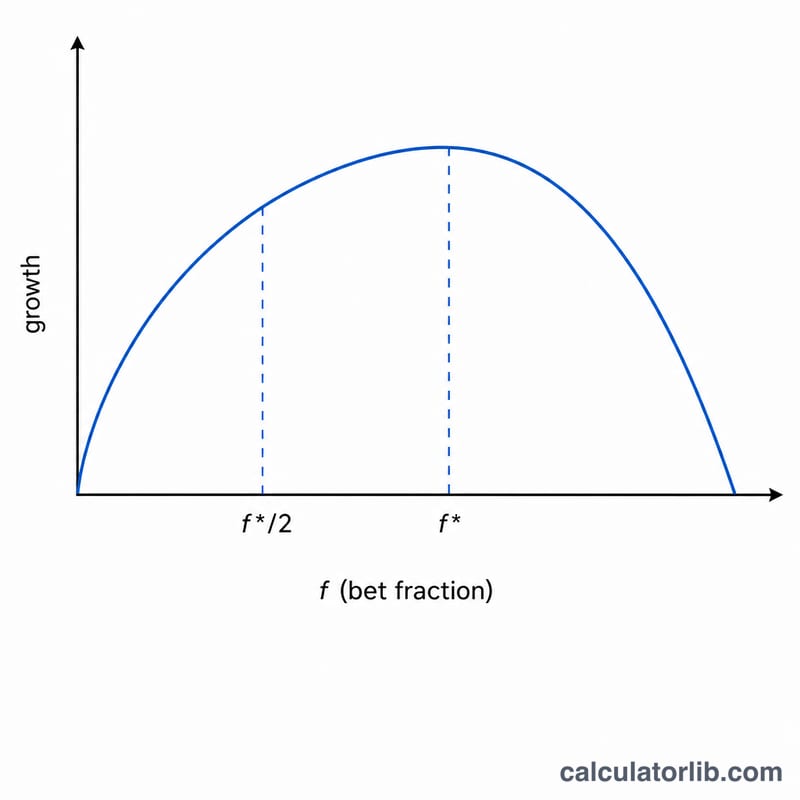

What is half Kelly? Betting half the Kelly fraction sacrifices a little growth for much lower volatility, which many practitioners prefer.

What if the result is negative? A negative fraction means the wager has no edge — the Kelly answer is to bet nothing.

Does Kelly guarantee profit? No. It maximizes long-term growth only when your probability and odds estimates are accurate; inflated estimates lead to over-betting and losses.