What Is the Income Multiple Net Worth Target?

This calculator estimates how much you should have saved by a given age, expressed as a multiple of your annual salary. It is based on popular age-based savings benchmarks (similar to those published by Fidelity), which translate a complex retirement-planning question into one simple, memorable rule of thumb: by certain ages, your invested savings should equal a growing multiple of what you earn.

How to Use It

Enter your gross annual salary, your current age, and optionally your current savings or investable net worth. The calculator picks the appropriate age-based multiple, multiplies it by your salary to produce a target, and shows how far you are from that goal.

The Formula Explained

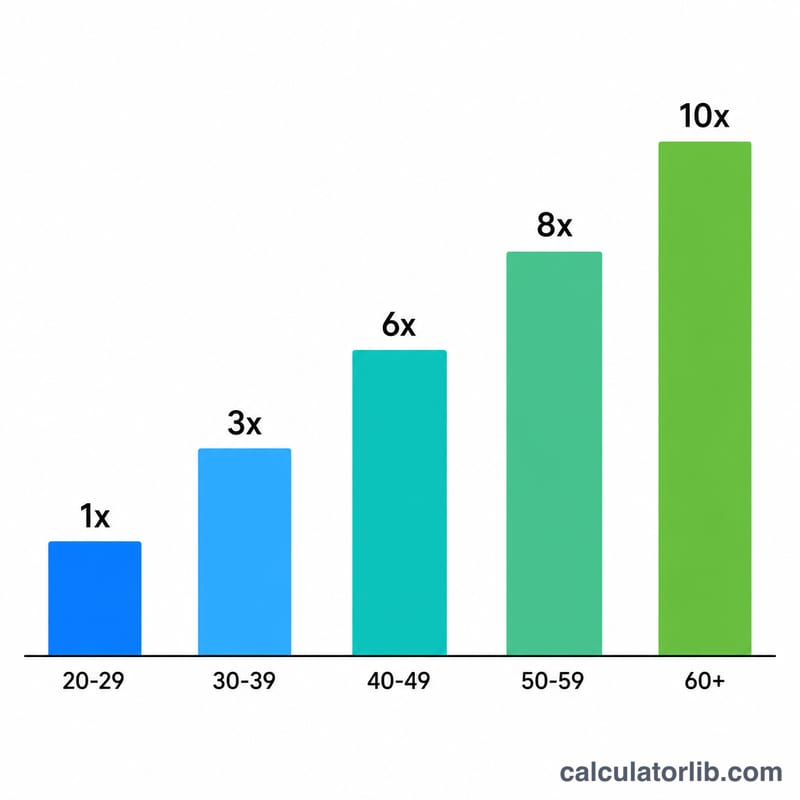

The core equation is $$\text{Target} = \text{Annual Salary} \times \text{Age Multiple Factor}$$ The factor grows with age to reflect the time you have left to compound your money. Common benchmarks are: \(1\times\) salary by 30–34, \(2\times\) by 35–39, \(3\times\) by 40–44, \(4\times\) by 45–49, \(6\times\) by 50–54, \(7\times\) by 55–59, \(8\times\) by 60–66, and roughly \(10\times\) by retirement at 67.

Worked Example

Suppose you earn $80,000 and you are 45 years old. The factor for ages 45–49 is \(4\times\), so your target net worth is $$80{,}000 \times 4 = \$320{,}000$$ If you currently have $200,000 saved, your gap to target is $120,000 and your progress is 62.5%.

FAQ

Are these targets exact? No. They are general guidelines. Your real number depends on lifestyle, retirement age, pension or social-security income, and investment returns.

Should I include home equity? Most benchmarks count investable/retirement savings rather than your primary residence, but you can include whatever net worth figure you wish.

I'm under 30 and the target is zero — why? Early benchmarks set the first milestone (\(1\times\) salary) at around age 30, so before then the rule simply encourages building the habit rather than hitting a specific multiple.