What is effective duration?

Effective duration measures how much a bond's price is expected to change when interest rates move, expressed in years. Unlike modified duration, it works for bonds with embedded options (callable, putable, or mortgage-backed securities) because it is derived directly from observed or modeled prices after small yield shifts rather than from a fixed cash-flow schedule. A duration of 6 means a 1% rise in yields would push the price down roughly 6%.

How to use this calculator

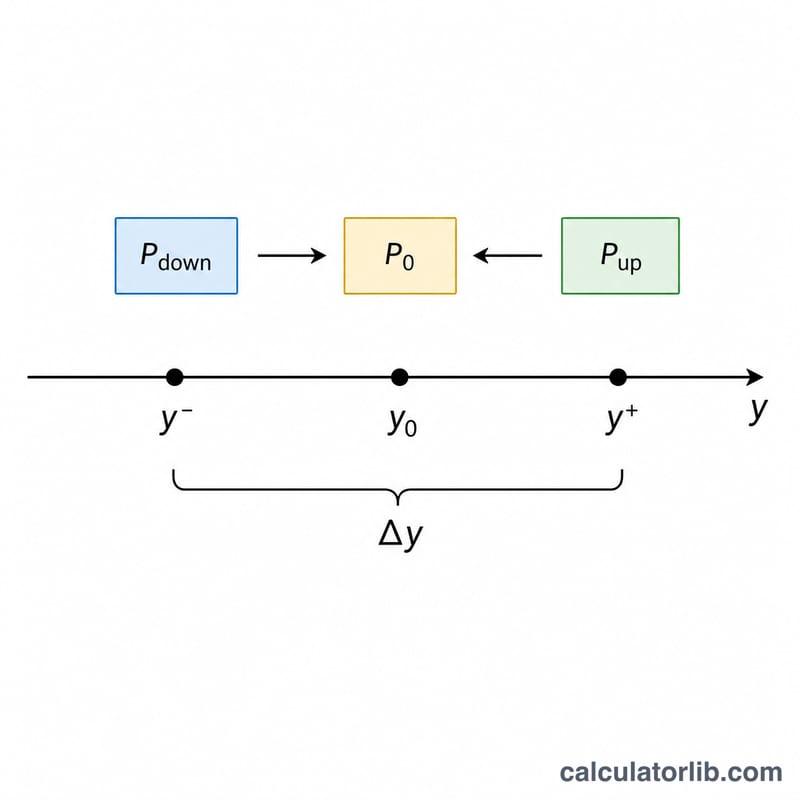

Enter four values: the bond's price if yields rise by Δy (P_up), its price if yields fall by Δy (P_down), its current price (P0), and the size of the yield shift Δy expressed as a decimal (for example, 0.005 for 50 basis points). The calculator returns the effective duration and an estimate of the percentage price change for a 1% move in yields.

The formula explained

The equation is:

$$D_{\text{eff}} = \frac{\text{P}_{\text{down}} - \text{P}_{\text{up}}}{2 \times \text{P}_0 \times \Delta y}$$

The numerator captures the total price swing between the down-yield and up-yield scenarios. Dividing by \(2 \times \text{P}_0 \times \Delta y\) normalizes that swing per unit of yield change and scales it to the original price, producing a value in years.

Worked example

Suppose a bond trades at P0 = 100. If yields rise 50 bps the price falls to P_up = 98.50; if yields fall 50 bps the price rises to P_down = 101.60. With Δy = 0.005:

$$\text{Effective Duration} = \frac{101.60 - 98.50}{2 \times 100 \times 0.005} = \frac{3.10}{1.00} = \textbf{3.10 years}$$

A 1% rise in yields would therefore move the price by roughly −3.1%.

FAQ

What yield change should I use? A small, symmetric shift such as 25–50 bps (0.0025–0.005) is standard. Too large a shift reduces accuracy because convexity becomes significant.

Why is effective duration better than modified duration? It accounts for the way cash flows can change when rates move — essential for callable and mortgage bonds whose prices behave non-linearly.

Is duration negative for some bonds? Rarely; certain structured products (like some interest-only strips) can show negative effective duration, meaning their price rises with yields.