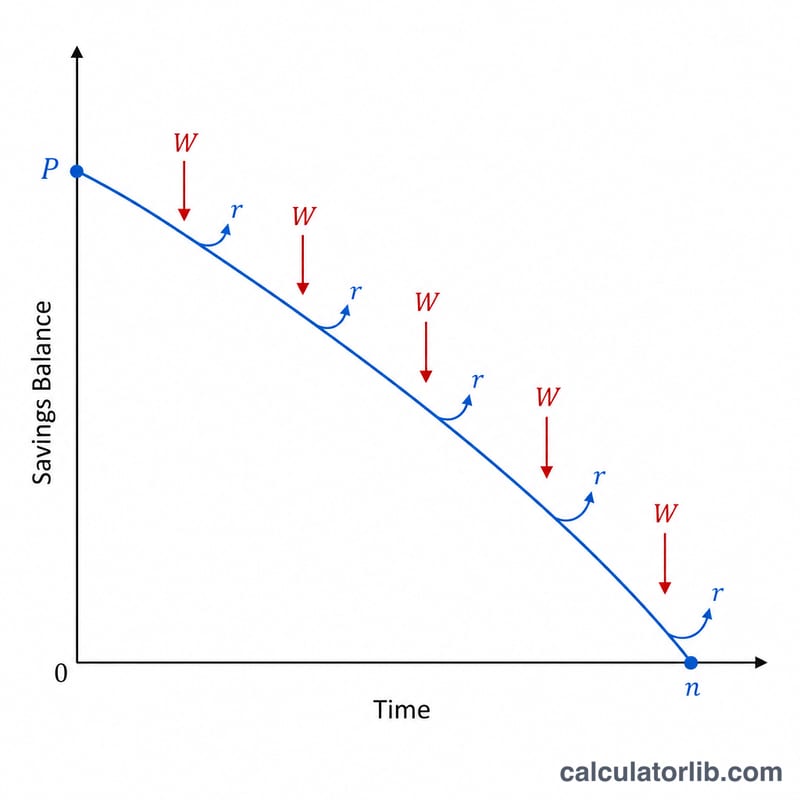

What This Calculator Does

The Savings Drawdown Duration Calculator tells you how long a lump sum of savings will last when you take regular withdrawals while the remaining balance keeps earning compound interest. This is the classic "annuity exhaustion" problem retirees face: you have a nest egg, you withdraw a fixed amount each period, and interest partially offsets your spending. The tool returns the number of periods, the equivalent number of years, and the total you will withdraw before the balance hits zero.

How to Use It

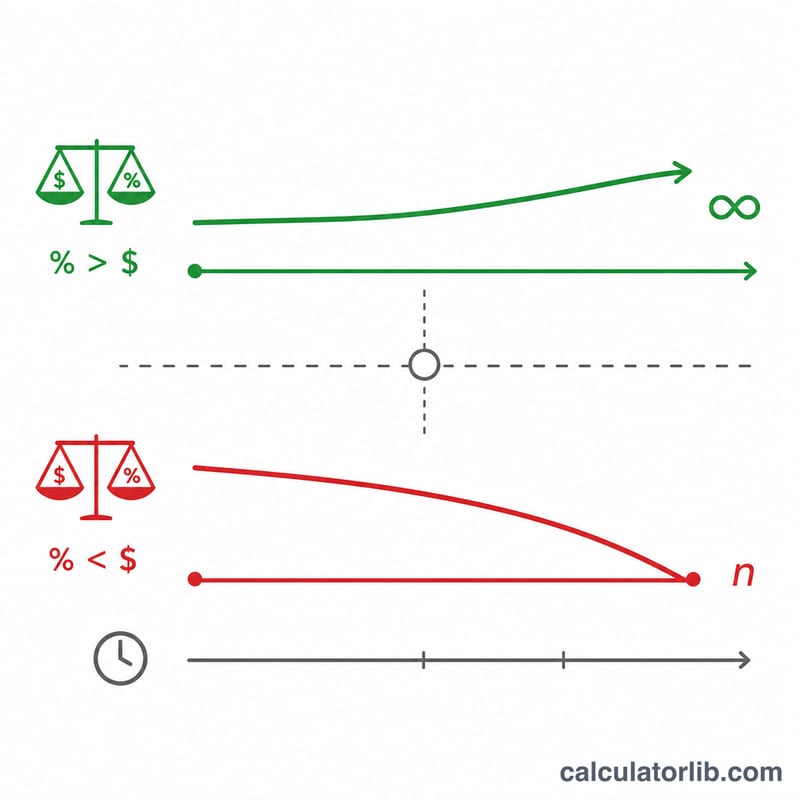

Enter your starting balance, the fixed amount you plan to withdraw each period, the annual interest rate your savings earn, and how often you withdraw (monthly, quarterly, semi-annual, or annual). The calculator converts the annual rate into a periodic rate and applies the drawdown formula. If your withdrawal is smaller than the interest the balance earns each period, the money never runs out and the result shows "Indefinitely".

The Formula Explained

The number of withdrawal periods is $$n = \dfrac{\ln\!\left(\dfrac{W}{W - P\,r}\right)}{\ln(1 + r)}$$, where \(W\) is the withdrawal per period, \(P\) is the starting principal, and \(r\) is the periodic interest rate. The denominator \(\ln(1+r)\) reflects compounding growth, while the numerator measures how fast withdrawals erode the balance relative to interest earned. When \(W \le P\cdot r\) the term inside the logarithm is non-positive, meaning withdrawals never exceed interest — the fund lasts forever.

Worked Example

Suppose you start with $100,000, withdraw $1,000 monthly, and earn 6% annually. The monthly rate \(r = 0.06 / 12 = 0.005\). Interest the first month is \(100{,}000 \times 0.005 = \$500\), which is less than $1,000, so the balance declines. Then $$n = \frac{\ln\!\left(\dfrac{1000}{1000 - 500}\right)}{\ln(1.005)} = \frac{\ln(2)}{\ln(1.005)} \approx \frac{0.6931}{0.004988} \approx 138.98 \text{ months},$$ or about 11.6 years.

FAQ

What if my withdrawal is less than the interest? The balance grows or stays level forever, so the calculator reports "Indefinitely".

Does this account for inflation? No — it assumes fixed withdrawals and a fixed nominal rate. To approximate real spending power, use an inflation-adjusted (real) interest rate.

Is this country-specific? No. The math applies to any currency and any savings or investment account that compounds at a steady rate.