What Is the Forward Premium?

The forward premium (or discount) measures how much a currency's forward exchange rate differs from its current spot rate, expressed as an annualized percentage. A positive value means the currency trades at a premium in the forward market; a negative value means it trades at a discount. This is a core concept in foreign-exchange markets and is closely tied to interest-rate parity.

How to Use This Calculator

Enter three values: the forward rate (the agreed exchange rate for a future date), the spot rate (today's exchange rate), and the number of days to maturity of the forward contract. The tool annualizes the result using the 360-day money-market convention and returns the premium as a percentage.

The Formula Explained

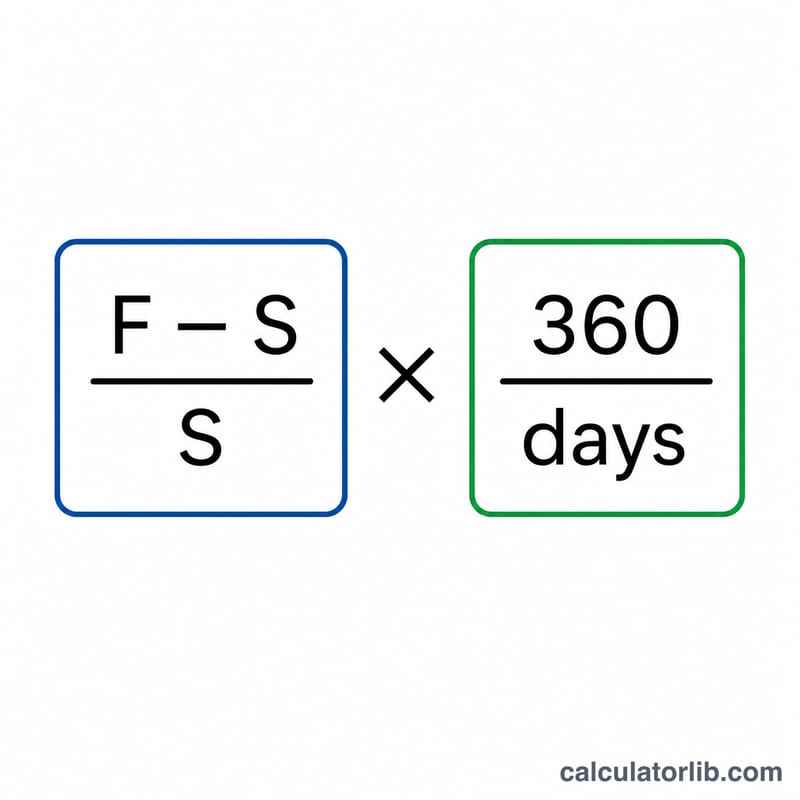

The calculation is:

$$\text{Forward Premium} = \frac{\text{Forward} - \text{Spot}}{\text{Spot}} \times \frac{360}{\text{days}} \times 100\%$$

The term \(\frac{\text{Forward} - \text{Spot}}{\text{Spot}}\) gives the raw period return. Multiplying by \(\frac{360}{\text{days}}\) scales that period return up to an annual figure, making forwards of different tenors directly comparable.

Worked Example

Suppose the spot rate is 1.2000, the 90-day forward rate is 1.2150. Then the raw difference is 0.0150, and \(\frac{0.0150}{1.2000} = 0.0125\), or 1.25% over 90 days. Annualized:

$$0.0125 \times \frac{360}{90} = 0.05 = 5\%$$

The currency trades at a 5% annualized forward premium.

FAQ

Premium vs discount? A premium (positive) means the forward rate is higher than spot; a discount (negative) means it is lower.

Why 360 days? The 360-day basis is the standard money-market convention for FX. Use 365 for an actual/365 basis if your contract specifies it.

What does the premium relate to? Under covered interest-rate parity, the forward premium roughly equals the interest-rate differential between the two currencies.