What Is a Currency Forward Rate?

A currency forward rate is the exchange rate agreed today for the delivery of one currency for another at a future date. It is the cornerstone of FX forward contracts, which let businesses and investors lock in a rate to hedge against future currency movements. The forward rate is not a forecast of where the spot rate will go — it is derived purely from today's spot rate and the interest rate differential between the two currencies, a relationship known as covered interest rate parity.

How to Use This Calculator

Enter the current spot exchange rate (domestic currency per unit of foreign currency), the domestic interest rate, and the foreign interest rate. Each interest rate should already match the contract horizon — for example, use the annual rate for a one-year forward, or pro-rate it for shorter periods. The calculator returns the forward rate, the forward points (premium or discount), and the premium expressed as a percentage of spot.

The Formula Explained

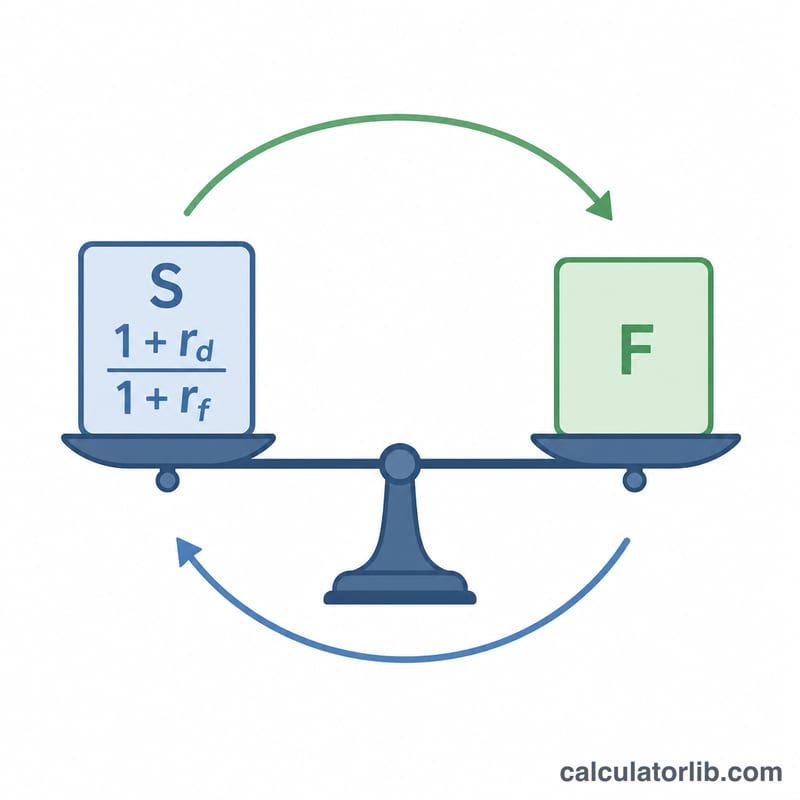

The forward rate is calculated as:

$$F = \text{Spot} \cdot \frac{1 + \dfrac{\text{Domestic Rate (\%)}}{100}}{1 + \dfrac{\text{Foreign Rate (\%)}}{100}}$$

If the domestic interest rate is higher than the foreign rate, the forward rate trades at a premium (above spot). If it is lower, the forward trades at a discount. This keeps an arbitrage-free relationship: an investor cannot profit by borrowing in the low-rate currency and investing in the high-rate currency once the forward hedge is applied.

Worked Example

Suppose the spot rate is 1.10, the domestic rate is 5%, and the foreign rate is 2%. The forward rate is $$1.10 \times \frac{1 + 0.05}{1 + 0.02} = 1.10 \times \frac{1.05}{1.02} = 1.132353.$$ The currency trades at a forward premium of about \(0.032353\), or roughly 2.94% over spot.

FAQ

Is the forward rate a prediction? No. It reflects today's interest rate differential, not an expectation of future spot levels.

What rates should I enter? Use risk-free or interbank rates that match your forward's maturity. For a six-month forward, use the six-month rate or half the annual rate.

Why is my forward below the spot rate? When the foreign interest rate exceeds the domestic rate, the forward trades at a discount and the result falls below spot.